By Chris Becker

The Euro tumbled last night as USD regained prominence, capped by a rally in oil prices, dragging up equity prices on both sides of the Atlantic. The usual safe havens were sold off slightly, namely gold and Yen as markets postiion before the Bank of Englands meeting tonight and the ever-important US NFP print tomorrow night. Services PMI prints from the UK showed a steep decline in growth while the non-manufacturing ISM in the ‘States was solid, if a little weaker from the stellar results shown earlier in the year. Treasuries are still bouncing around the 1.5% yield mark for 10 years, while other government bonds, particularly in Europe are looking shaky after a well overbought rally.

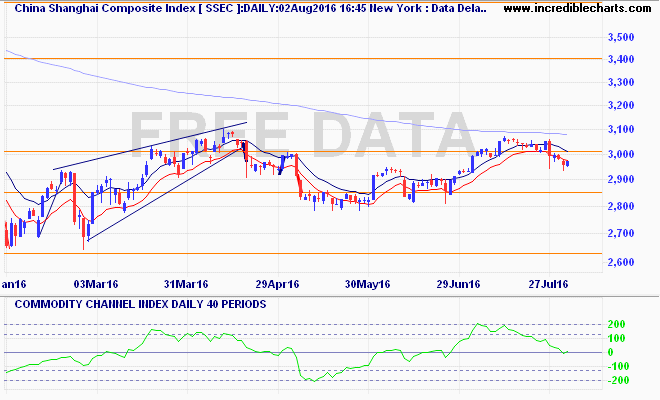

Recapping Asia’s session yesterday where the Shanghai Composite put a few runs on the board to finish up 0.2% to just above 2978 points. Again, it’s still below the critical support level of 3000 points with no real buying support as it chugs along under the 200 day moving average as its bear market continues to splutter: