by Chris Becker

Asia’s session was characterised by the release of CPI/PPI inflation figures from China and a slightly weaker Yen that kept both Chinese and Japanese stocks up respectively. The Shanghai Composite is currently up half a percent, building on the slight breach above key support at 3000 points yesterday, while in Hong Kong, the Hang Seng is off slightly. The Nikkei is up 0.7% with futures gaining further going into the London session, where Eurostoxx futures are mixed, with the DAX down slightly.

The ASX200 was all over the place today, initially reacting to some local releases and indeed earnings season as that picks up pace today. What sent it up finally at the close – although mildly, only 0.3% – was the NAB’s call for two more rate cuts to take the OCR to 1% by the end of 3Q in 2017.

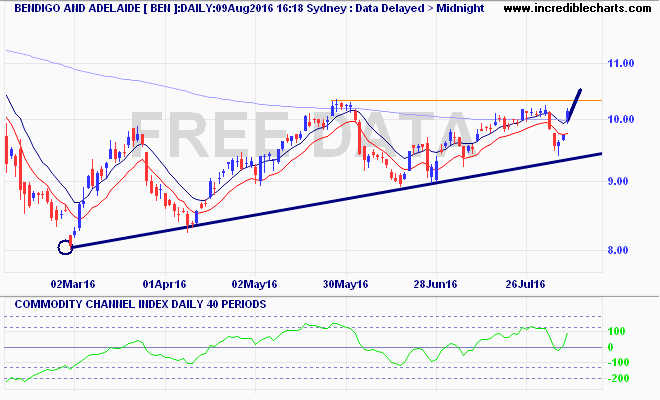

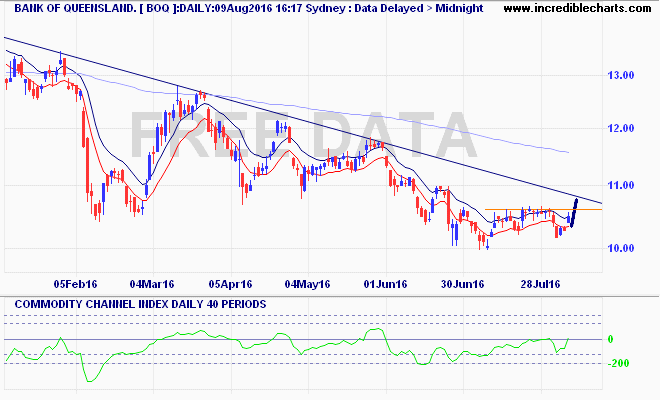

It was the banks that soared today, with ANZ up nearly 3%, CBA up 1.5%, NAB up 2.3% and WBC up 1.8% with regional banks also lifting, Bendigo (BEN) up nearly 4% and BOQ up nearly 3%

That’s a significant breakout for the regionals, although BOQ is just below its bear market downtrend line, I prefer BEN here:

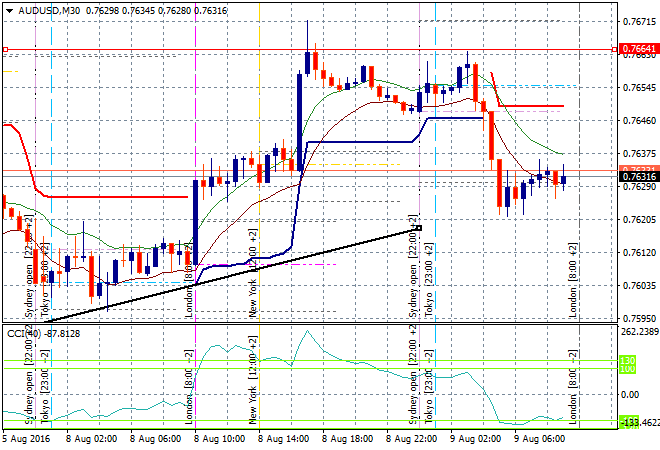

In currencies, the Aussie dollar cracked on NABs call and the CPI release from China, retracing the gains made overnight, but still on trend and above 76 cents against the USD as more calls are made for it to get to 80c or even higher:

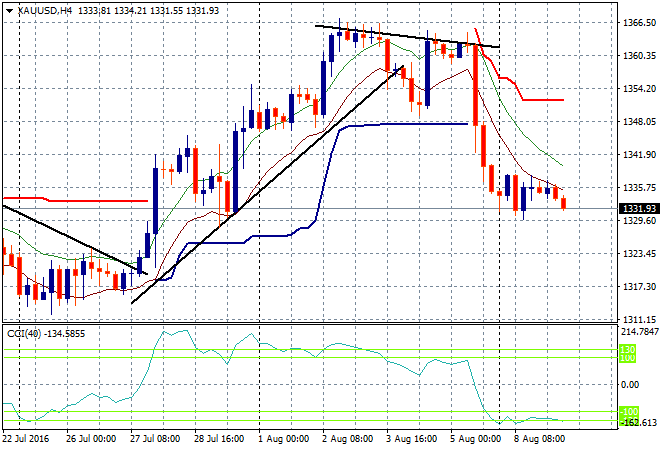

I’m watching gold again which is showing signs of cracking coming into the London fix. There’s not much support in the Asian session so a follow through $1330USD per ounce is possible tonight:

The data calendar tonight continues with the Euro/German trade balance, but the main one to watch in Europe (or out of Europe?) is UK manufacturing production.