With weak US growth baked-in and a Fed that is “one and done” in its tightening cycle, it’s time we ask what impact that this will have on the outlook for the Australian dollar. I do not expect the US dollar to fall very far given the US rates and economic outlook remains more robust than all other major economies but neither can we rely upon a Fed tightening cycle to lift the USD further and by extension to drop the Australian dollar.

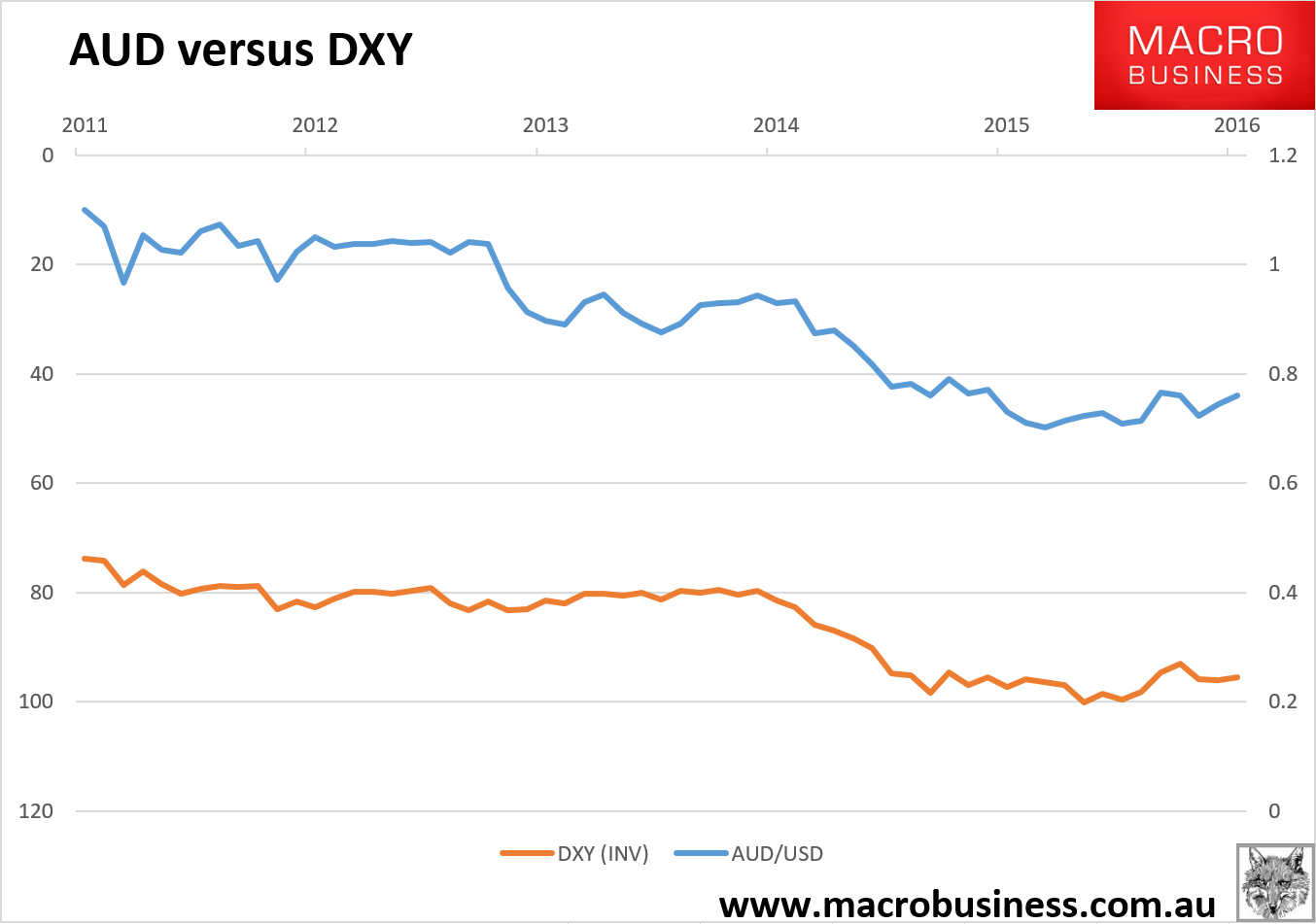

There are two easy ways to judge the relative value of the USD. The first is simply that it is the flip side of the Australian dollar cross. The second is to use the US dollar index, which is an amalgam of the value of the reserve versus all other currencies. If we compare these two values then it gives us a rough idea of much the AUD/USD is impact by the intrinsic value of the USD. Here’s the first chart:

As you can see, there is a strong correlation between a rising DXY and a falling AUD/USD. That is, weakness on the US side of the currency-cross contributes a lot to the value of Australian dollar in US dollar terms, as you’d expect. Maybe more than anyone would care to admit!

Advertisement

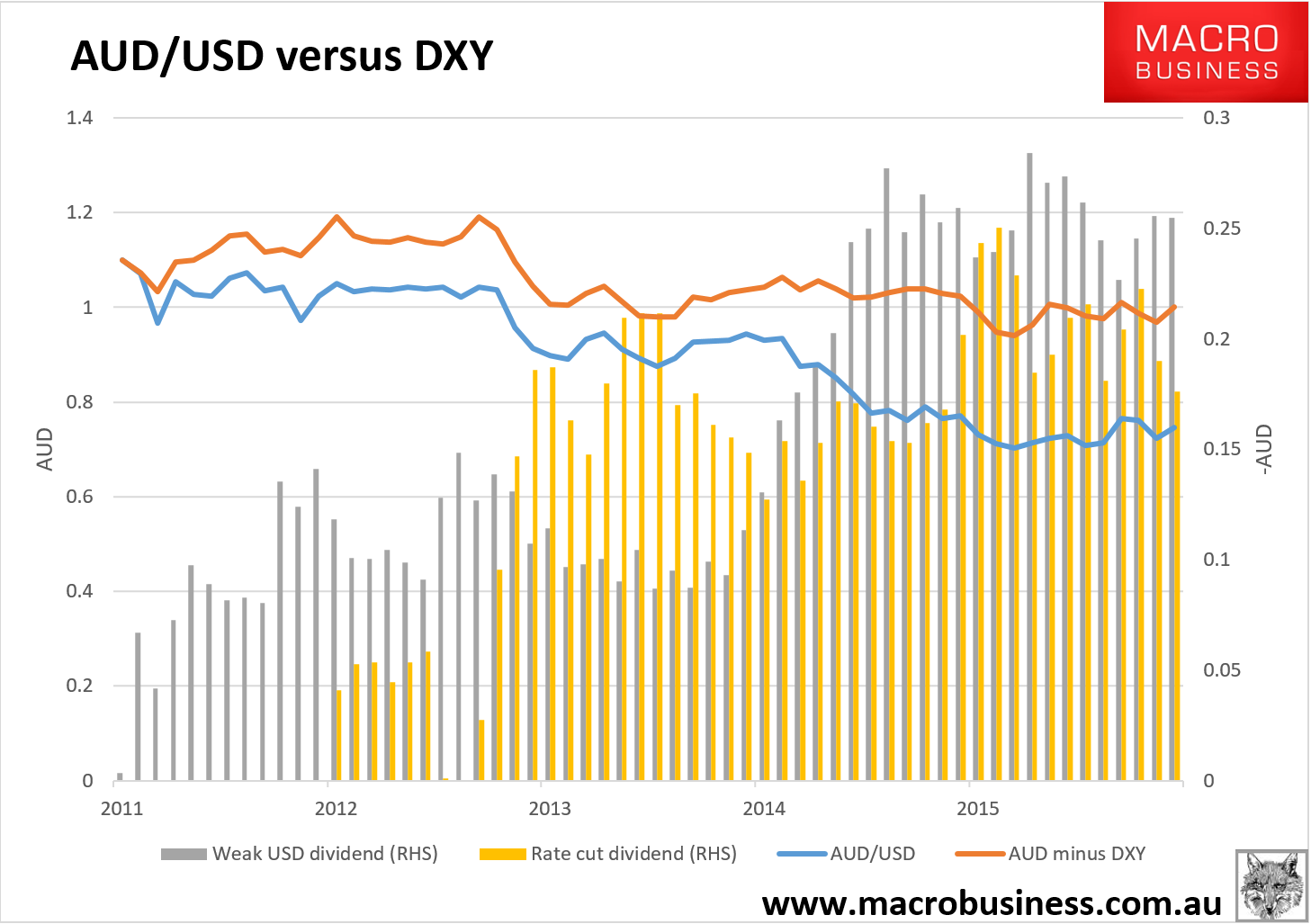

Here is the money chart in which I have compared the value of the AUD/USD today versus what it would look like if there had been no strength on the USD side (by subtracting the influence of the DXY) in recent years:

The difference is rather scary with AUD at $1.01 today if there were no USD strength instead of 76 cents. The strong USD (grey bars) has driven the majority of AUD/USD falls indeed, without it, the cross would not have peaked until early 2013 at $1.19 (all things being equal, though the RBA would have been forced to cut earlier and harder so probably not).

Advertisement

There are many other factors driving currencies – terms of trade, sentiment, technicals, growth etc – but all of these are more or less captured in the setting of monetary policy so I’ve extrapolated the remaining AUD/USD devaluation to the efforts of the RBA (yellow bars). It has contributed 18 cents of devaluation.

So, what does this tell us about the outlook for the Aussie?

First, rate cuts have very likely prevented an Australian recession in the past two years given the AUD would still be above parity without them, preventing any kind of rebalancing and causing enormous pain to mining.

Advertisement

Second, if the US economy were to weaken enough to push its labour market into weakness, triggering a Fed loosening, then the lift under the Aussie is going to be powerful. This would be very difficult for Australia.

Third, that will only be the case if US economic weakness does not threaten outright recession. In that event then the USD would rise as global share markets plunged into an end of cycle shock.

Fourth, it is highly probable that there is more to be gained from further rate cuts vis the currency. The AUD is 18 cents lower than it otherwise would be today owing the rate cuts. The spread between US and Australian interest rates has fallen roughly 2.75% to deliver this outcome so with half that compression available ahead we might expect another 10 cent fall. I suspect it would be a little larger simply because the carry trade argument will cease to exist completely.

Advertisement

So that gets us to the low-60 cents range. From there it is all about either rising US rates or crisis to push the AUD lower.

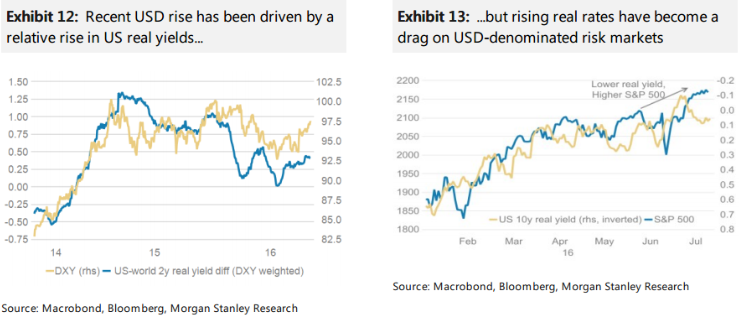

But! That assumes no USD weakness and that’s what Morgan Stanley sees coming:

USD looking south: The Fed has little to gain by hiking rates early. Hence, we regard the recent rise in real US yields that has supported the 4% USD rally seen since May as unsustainable. Our long-held framework suggesting a combination of high global debt, capacity overhangs and resulting low returns on investment should keep deflationary pressures intact. The impact that this environment will have on financial markets via a flattened yield curve and subdued inflation expectations should further support our weaker USD view, even though there have been recent upside surprises in US economic data.

Lower US real yields: Over recent weeks markets have re-priced the front end of the US yield curve. For now, the Fed has no incentive to disagree with the market probability of a 50% chance of a 25bp rate hike by the end of this year. However, US economic surprises have probably peaked and falling oil prices may no longer be a net support for the US as it has become the globe’s biggest oil reserve holder. When oil prices declined in 2014/15, the consumer’s oil dividend ended up going into higher savings while oil sector investment fell. Our in-house indicators predict US domestic demand weakening from here. Starting with momentum:

Accordingly, USD should trade lower from here, and with markets positioned long in USD we expect that, initially, relative positioning and not relative fundamentals will drive markets.

The FX trade: This leaves the question of which currencies to trade long when a decline in risk appetite is the most likely outcome. JPY, EUR and CHF are best positioned to rally. Unfortunately, it would be a pain trade for many.

Some investors thought JPY would weaken with the help of coordinated expansionary fiscal and monetary policies of Japan’s authorities. This trade has been called into question this week.

Some investors though the EUR would weaken,assuming that Brexit would weaken EMU economies by fuelling populism and increasing political uncertainties. However, EUR has remained stable. Domestic real money accounts have not developed an appetite for additional FX risk.

Consequently, EURUSD stayed above 1.09, with EUR-bearish positioning creating an ideal springboard for EUR to move significantly higher.

The stable EURCHF despite improved risk appetite suggests more CHF stability going forward, with Switzerland’s 10% current account surplus generating commercial CHF buying needs.

Advertisement

As I say, any USD weakness is temporary in my view, especially so vis the zombieuro as its existential political challenges continue to flow, however there is clearly scope for a tactical weakening which will again slow any Australian dollar falls, as well as accelerate rate cuts.

I raised my Aussie dollar target earlier this year to 66 cents in the event that the Fed did not hike again. Since then, bulk commodity prices have proven more sticky than I expected, in part owing to the financialisation of iron ore ore which is impacted by the USD, and the rebound in coal which is temporary but material, also supporting the AUD.

Iron ore should still fall heavily by year end, and we’ll get at least one more rate cut with a growing consensus around another, so that will still weigh on the AUD.

Advertisement

Even so, it looks like even my 66 cent target was too bearish now. I’ll raise it to 70 cents.

Beyond that I still expect the grind lower to continue as falling rates and commodity prices steadily take there toll. The deep plunge to 50 cents and below comes with the next crisis.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.