More headwinds for bank earnings, from Morgan Stanley:

Higher than forecast loan losses in the June quarter: We believe reporting season has highlighted the downside risk to major banks’earnings from a deterioration in credit quality. Loan losses in the June quarter were ~7% higher than our forecast and did not fall relative to the 1H16 quarterly average, despite the non-recurrence of “single name” loan losses. We note that: ANZ’s charges rose due to specific provision top-ups; stressed exposures increased in 9 of 12 industry segments at WBC;new impaired assets increased ~20% h-o-h and troublesome exposures rose ~10% at CBA;and NAB boosted its mining and agriculture overlay.

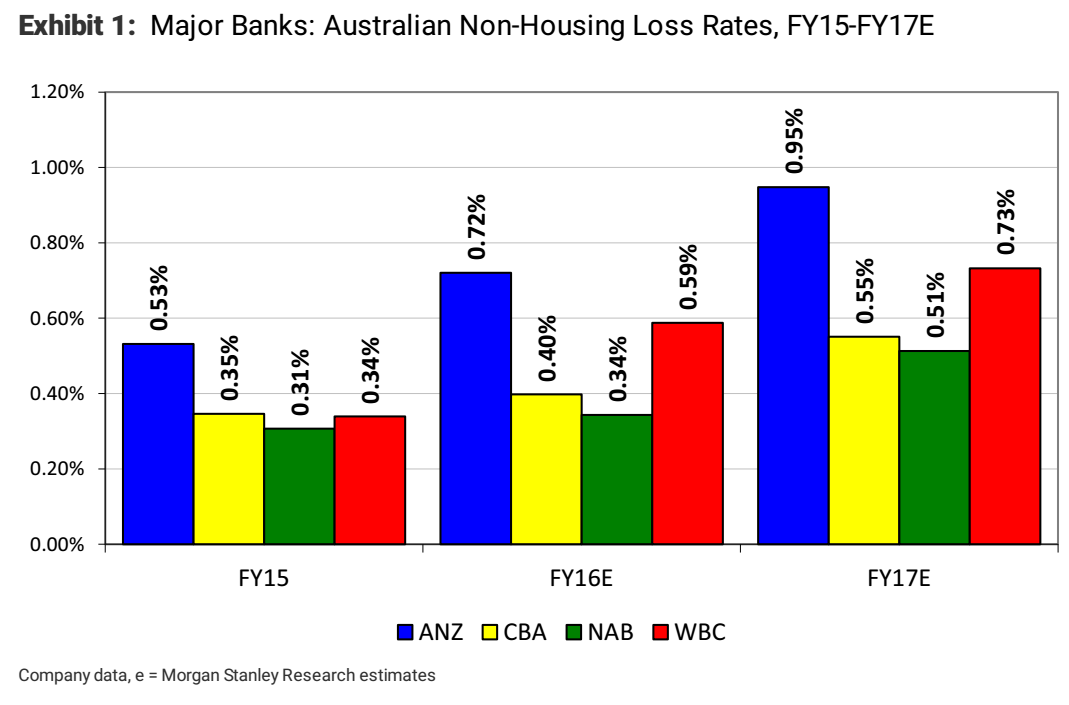

Comparing the banks’ Australian non-housing loss rates: Our Chart of the Week shows our forecasts for the majors’ Australian non-housing loss rates. We expect them to rise from ~37bp in FY15 and ~49bp in 1H16 to an estimated ~66bp in FY17E. We highlight: (1) the last reported loss rates were ANZ 1H16: ~73bp, CBA 2H16: ~43bp, NAB 1H16: ~28bp,and WBC 1H16: ~66bp; (2) ANZ’s loss rate has been >50% higher than the peer average over the past 18 months,and our forecasts assume this remains the case; (3) NAB’s Australian loss rates fell from ~57bp in FY13(above CBA: ~54bp and WBC: ~42bp) to 31bp in FY15 as a result of de-risking,and our forecasts imply that it will be the “lowest risk” bank in FY17E with a loss rate of ~51bp vs the peer average of ~66bp; (4) WBC has suffered more than CBA and NAB from single name exposures in FY16E,and we conservatively assume that its loss rates will remain higher in FY17E. Overall, we see a higher probability of loan loss driven FY17E earnings downgrades at NAB than we do at ANZ or WBC.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.