From the ABC:

The key ingredient in essential everyday items – from milk bottles and waste bins to eskies and pipelines – is made in a factory just outside Melbourne.

The polymer is made by a company called Qenos from Australian gas extracted from the huge fields of the Cooper and Surat Basins in the arid lands out near the Queensland, New South Wales and South Australian borders.

It’s not just used for plastics. Foundries, food processors, wool scourers and all sorts of other businesses rely on that gas as a cheap, clean and reliable source of heat and power.

At least, they used to. Many of those businesses now find themselves under threat as a result of soaring gas prices that have rendered them uncompetitive on the global stage.

Adding insult to injury, it is Australian gas flooding into Asia that has caused a regional glut. Prices have collapsed and Asian manufacturers can now buy Australian gas at half the price local manufacturers are paying.

“Companies will shut, jobs will go,” warns Dow Chemical Australia chief executive Tony Frencham.

It’s a sentiment echoed by Qenos managing director Jonathan Clancy.

According to the Australian Industry Group’s Tennant Reed, the long run wholesale average price has soared from $3 to $4 a gigajoule on average to around $6 or $7 a gigajoule, occasionally peaking at far higher prices.

“At times they have been $12, $15 or $20 a gigajoule,” he said.

According to Mr Clancy, the situation is likely to deteriorate further.

“The situation for us is that we can see those prices escalating in the vicinity of 50 per cent,” he says.

It is not just the price. Major manufacturers such as Qenos and Dow Chemical are also worried about supply.

It’s a paradox. Australia is home to some of the largest gas deposits in the world. But a $200 billion investment in liquefaction and shipping facilities has transformed it into the world’s biggest gas exporter.

Three massive new plants at Curtis Island, just off Gladstone on the Queensland coast, are contracted to supply Asia with gas. An unintended consequence of this gas bonanza, however, has been to create shortages at home.

“We’ve got the perfect storm just now,” says Qenos’s Jonathan Clancy.

“We’ve had the Gladstone LNG projects come online, we’ve got a collapse in the oil price which means exploration isn’t taking place and then we’ve got these moratoriums on onshore gas development preventing us from getting access to conventional onshore gas.”

The exporters, struggling to fulfil contracted orders written years ago when the plants were in planning stage, have begun raiding gas from the domestic market to meet their contracts.

Mr Frencham says the contracted price Dow has been forced to pay will increase 50 per cent this year.

Apart from that being outrageous, that is going to put us well above international gas pricing in any of the free markets in the world

Japan is our biggest buyer. Businesses there have been reportedly able to buy Australian gas at around half the price to that available to Australian manufacturers.

By several estimates, Asia will be awash with cheap Australian gas until at least 2022.

According to Mr Reed, spot gas prices in east Asia are as low as they have been in living memory.

“So we have not just a loss of a source of advantage but gas prices have become a source of competitive disadvantage,” he says.

Global chemical maker Incitec Pivot was planning to expand in Australia but instead diverted its cash to Louisiana in the US.

“It simply couldn’t get long term credible gas prices it could depend upon,” said Mr Frencham.

“I know of another company here I can’t name who has closed a plant … wanted to in fact expand the plant but could not get long term gas pricing at an affordable level and is now looking offshore.”

A 2012 report from NIEMIR claimed that for each dollar gained from gas exports $21 in economic activity was lost.

Even more concerning, a Deloitte report predicted that high gas prices could result in the loss of up to 15,000 manufacturing jobs as industries shut down.

“It doesn’t allow us to plan any expansion,” says Dow’s Mr Frencham.

“I can’t go to my international leadership and propose anything to them because I don’t know what the price of gas is going to be.”

Jonathan Clancy has a similar lament.

“The thing that we had to our advantage was energy and we must find a way to quickly get that opportunity back,” he says.

Newly appointed Energy Minister Josh Frydenberg has put reform of the national electricity market and gas at the top of his agenda.

“We need more gas supply and more gas supplies in Australia, and gas is an important part of the energy mix,” he said in a recent interview on ABC’s Lateline.

That’s music to the industry’s ears.

“The gas producers need all the help and assistance that they can so they can bring supply to market, because that’s what we need; more supply.”

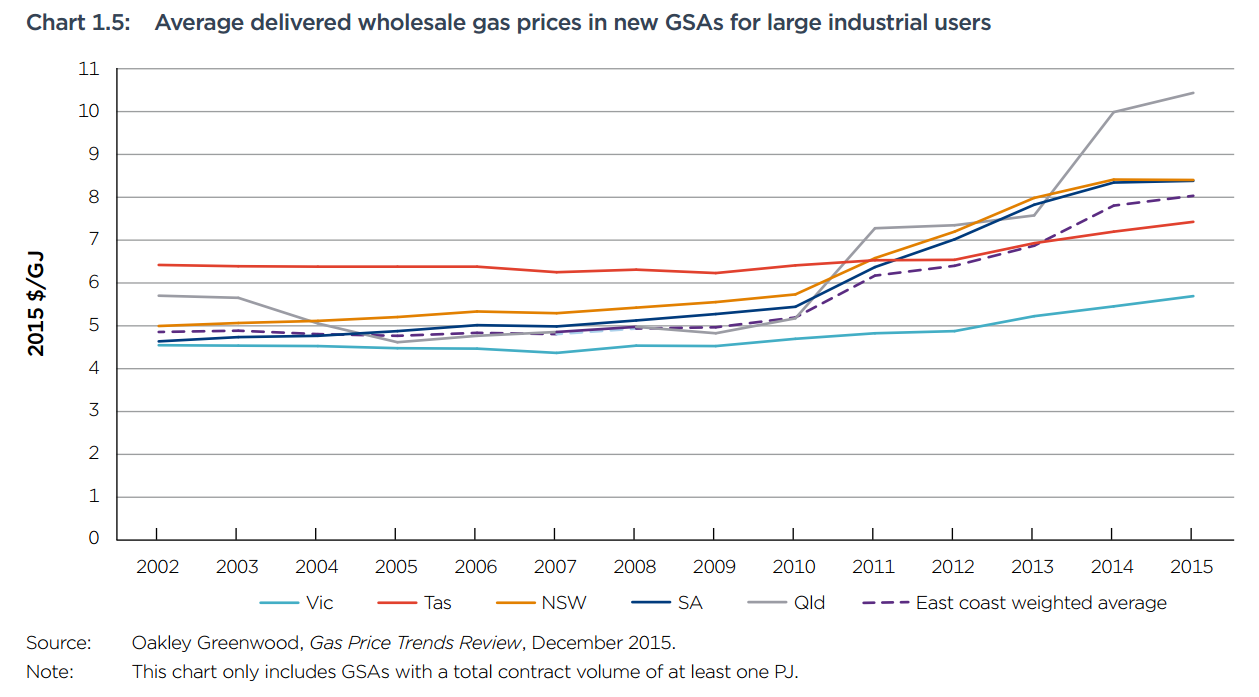

All true, here’s the chart:

It’s worse for industrial users, from the ACCC:

The ABC missed the crucial point that gas sets the marginal cost of electricity on the east coast so it’s a lot worse for your electricity bill:

So, what’s the answer? Here’s some:

- install domestic gas reservation onto the east coast cartel;

- force more east coast fraccing. I suggest a government corporation to reassure communities of high safety standards vis water tables and to ensure mandated pricing to force the cartel to heal. Otherwise you may still need domestic gas reservation;

- government buys one of the gas carteliers and uses it to force efficient market pricing;

- install LNG regasification terminals in eastern cities and buy US gas, or, buy our own gas back from Asia. After all, they have a glut of it. When Japan breaks the destination clauses in supply contracts later this year it will be very easy to divert a cargo from Gladstone to Sydney. Floating LNG regasification terminals are only $200-300 million each versus $1 billion for onshore. I’d suggest the former because once installed they won’t be used anyway. By rendering the local gas market contestable, the cartel will drop its prices to compete and undercut the imports.

There is no wondrous solution here without the heavy hand of regulation.