Our report on the Brexit vote emphasised one key point over all others: that the way forward for the global economy is fraught with risk and uncertainty, and only time will tell the inevitable scale of the vote’s impact.

For the US, the immediate response from market participants was to remove any and all likelihood of a rate hike out to the end of 2018. Indeed, in the first few days after the decision, participants went as far as to price in a circa 20% chance of a Fed Funds Rate cut by November 2016.

As the week has progressed, fears have been quelled and the chance of a rate cut priced out. However, it is still not until the end of 2018 that the next rate hike from the FOMC is fully priced. Said profile raises doubts over whether the US rate cycle has been indefinitely delayed.

From Chair Yellen’s recent appearances following the June FOMC meeting, we know that the (then) impending Brexit decision was a factor in the Committee holding fire in June. The ongoing uncertainty regarding what the people’s decision means for the UK; European Union; and the global economy will likewise almost surely keep the FOMC on the sidelines again in July.

Yet, looking past the next meeting, evident from the volatility in pricing noted above (not to mention the sharp reversal in equity markets and the VIX this week) is that perceptions of the future can shift rapidly.

Simply, just because the Brexit vote occurred does not mean that the US rate hike cycle has automatically come to an end. Throughout the past year, the FOMC has remained watchful of global developments; yet their primary focus has always been the domestic economy, specifically the strength of demand and the consequences for inflation. For the domestic demand outlook, there are two primary factors: the consumer and the USD.

First, Chair Yellen and the Committee have long emphasised that their optimistic outlook depends on the consumer’s willingness to spend on marginal consumption. That itself is a function of the labour market (which, despite recent weak results, still remains robust) and the confidence consumers have in the economy and their own financial position.

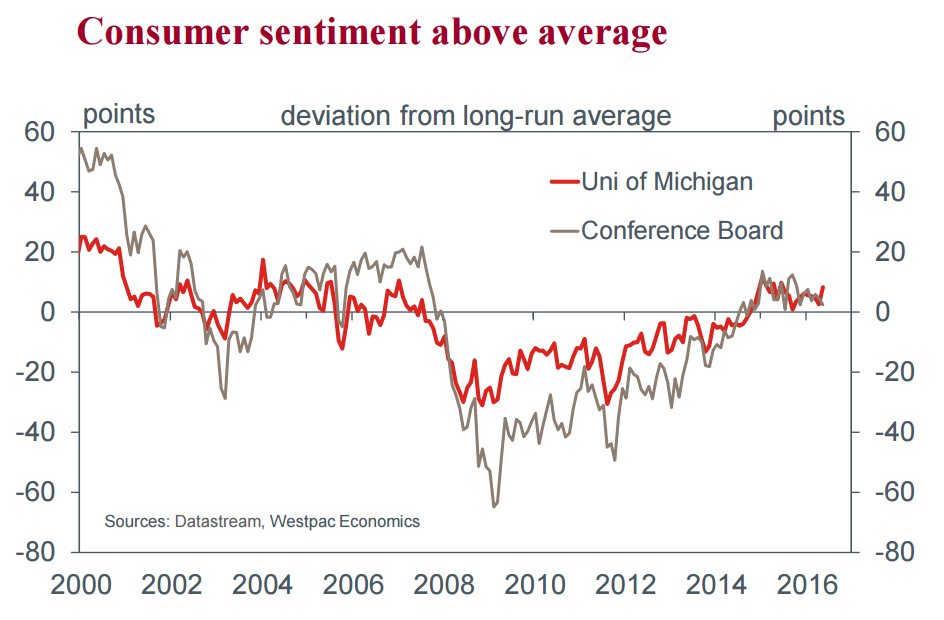

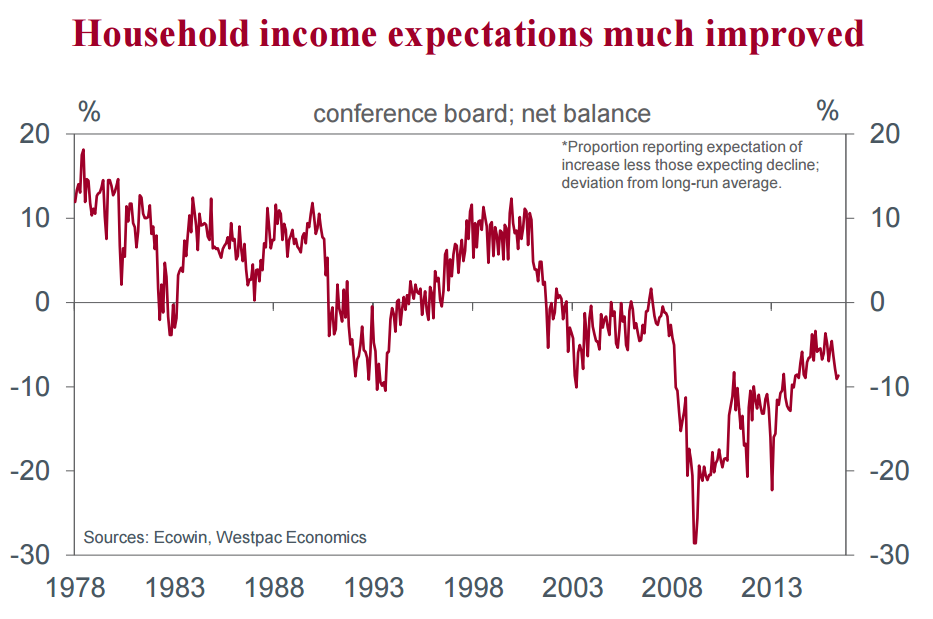

Notable over the past year is that headline consumer confidence has remained consistently above-average and broadly consistent across income cohorts. Added to this has been the longer-term improvement in income expectations.

Should confidence persist, the Committee will likely remain optimistic on the outlook and the chances of (eventually) achieving their mandate.

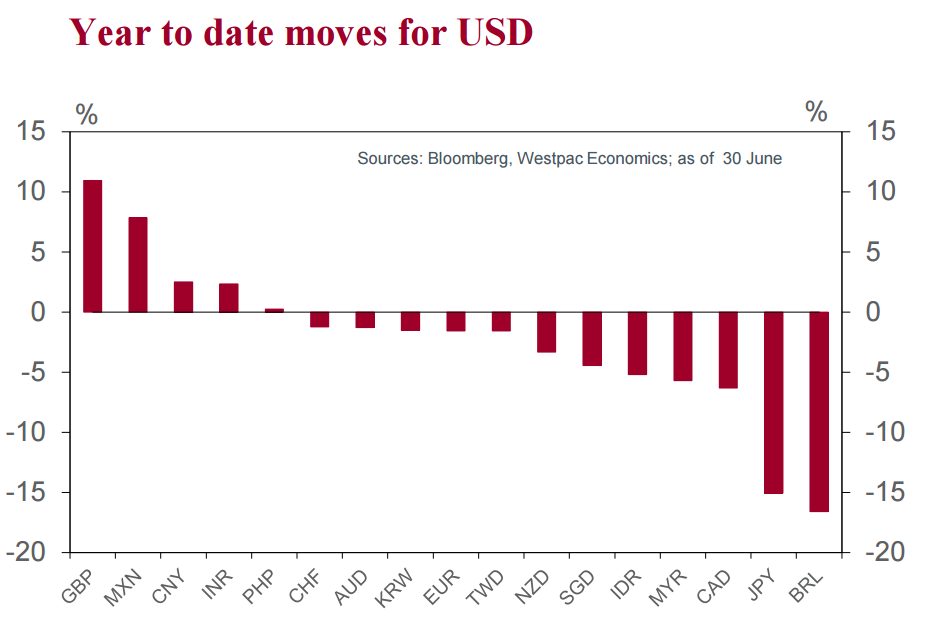

The second major factor is the impact of the USD. Obviously a weaker pound and (potentially the) Euro sees the USD strengthen – note, having a higher trade weight, the EUR/USD trend has a greater impact on the US economy than sterling.

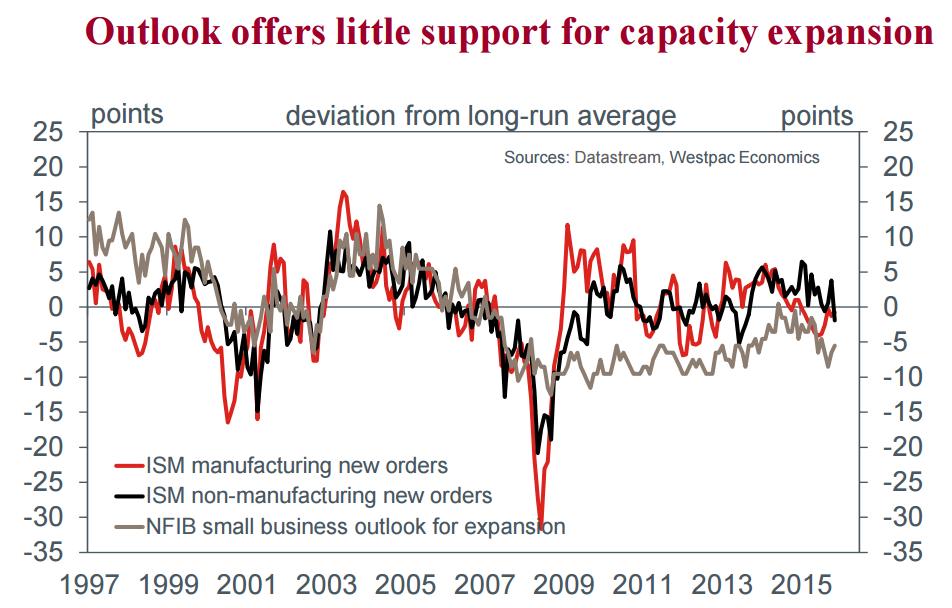

We know from the business surveys that the consistent appreciation of the USD in recent years has weighed heavily on US firms’ competitiveness as well as their willingness to invest in real capacity. Amid weak real growth globally and market uncertainty, a stronger USD (for longer) would further cement this weak trend.

Herein then lay their test for further action: any decision to alter the stance of policy will depend on the FOMC being confident enough in the US consumer and investment to stay anxiety vis a vis the globe.

Sorry Elliot. Those income expectations are at recessionary levels. Consumer confidence is weak for this stage of the business cycle, firms are winding in investment (except in capital management fiddles) and the US dollar is now structurally stronger.

It’s not near easing yet but the Fed is done tightening, which helps explain some of the recent market ebullience.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.