Australia’s economy started 2016 on a strong note following a robust performance in 2015. Real GDP expanded 1.1% quarter-onquarter and 3.1% year-on-year in the January-to-March period, driven robust growth in exports and private consumption. Notably, commodity export volumes are proving resilient to China’s slowdown, in part because of continued demand for Australia’s relatively high quality metals and ores. Meanwhile, the weaker Australian dollar has boosted the price competitiveness of services exports such as education and tourism, which rose 6.1% quarter-on-quarter in January-March. Low interest rates and the wealth effects from rising house prices continue to support robust household spending. We expect these factors to continue to sustain growth, and forecast real GDP to rise by 2.5% through 2016 and 2017.

By contrast, nominal GDP has been relatively weaker, up only 2.1% year-on-year in the first quarter. We expect the deterioration in terms of trade and, as a result, muted corporate profitability and wages to continue to weigh on nominal GDP growth.

In turn, this economic environment will make the government’s objective to return to a fiscal surplus by fiscal 2021 difficult to achieve. The government projects the fiscal deficit of the Commonwealth government to narrow to 0.3% of GDP in 2019-20 from an estimated 2.4% in 2015-16. But large spending commitments on education, health, and social security and welfare, which account for around 60% of total Commonwealth government spending, will be tough to curb. Moreover, slow growth in wages will continue to pressure income tax receipts, which account for the biggest share of government revenues. Furthermore, budget outcomes have been worse than projected in recent years because nominal GDP and iron ore prices have turned out lower than assumed by the government, resulting in lower revenue intake. We forecast lower nominal GDP growth in the medium-term than assumed in the latest budget, signalling some downside risks to revenues.

As a result of constraints on spending cuts and lacklustre revenue growth, we expect the government debt-to-GDP ratio to rise further, to more than 39% of GDP in 2017 from around 36% in 2015 and 19% in 2010. This implies that fiscal room to buffer potential negative shocks is eroding somewhat.

Persistent low inflation pressures prompted the Reserve Bank of Australia (RBA) to cut rates by 25 basis points to a record low 1.75% in May. The decline in headline inflation in the March quarter lowered the year on year rate to 1.3%, well below the central bank’s 2% to 3% inflation target.

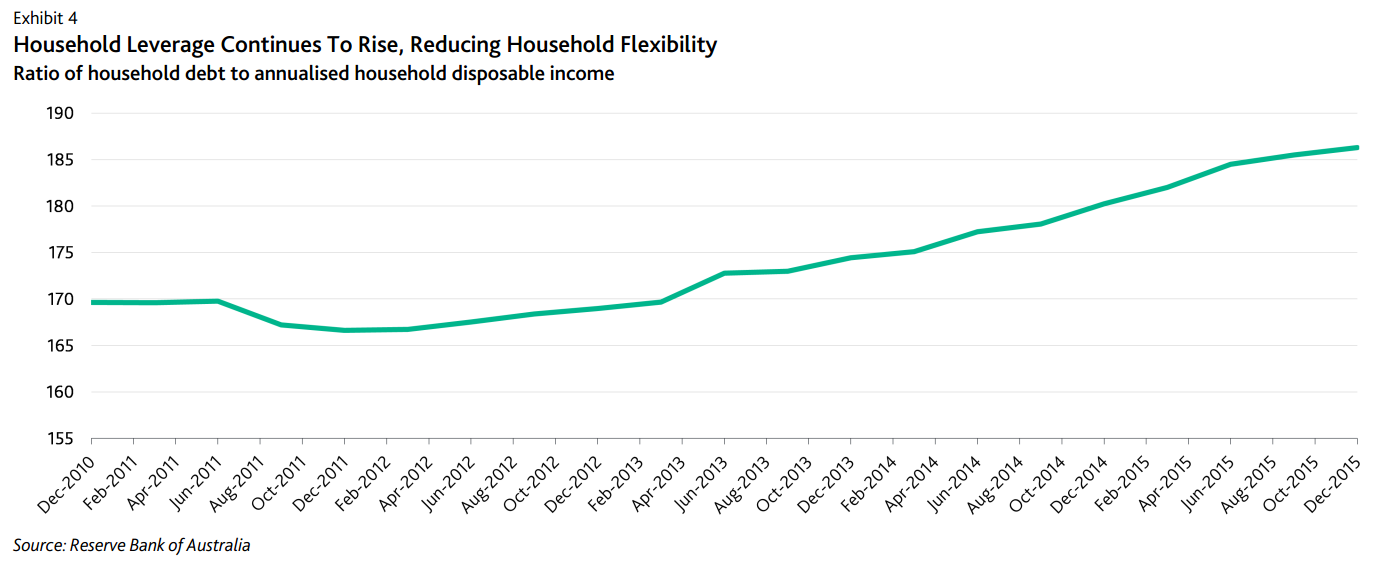

The low interest rate environment is supporting housing demand, pushing up house prices and driving credit growth. According to CoreLogic RP data, house prices in Australia’s five-largest cities increased more than 10% year on year in May, led by gains in Sydney (up 13%) and Melbourne (up 13.9%). Strong house price increases in recent years have also been accompanied by a build-up in household debt, which leaves the economy and financial system vulnerable to a negative shock.

Australia’s current account deficit narrowed to AUD20.8 billion in the March quarter, from the December quarter’s AUD22.6 billion deficit, largely reflecting a sharp fall in imports. Still, the current account deficit remains large at around 5% of GDP, wider than the 4.7% shortfall in 2015. We expect the current account to remain firmly in deficit through 2016 and 2017 given continued weakness in export prices. Notwithstanding this, Australia should be able to continue financing its current account deficit, as the country’s strong institutional and policy framework as well as its large and diverse economy will likely keep attracting international capital inflows.

Boring, just get on with the downgrade. And banks:

Australian banks are facing a growing number of headwinds due to increasing household leverage and persistently low interest rates, which are increasing the banks’ sensitivity to shocks. These headwinds may, over time, put pressure on the credit profiles of Australia’s major banks, particularly in the context of their very high ratings.

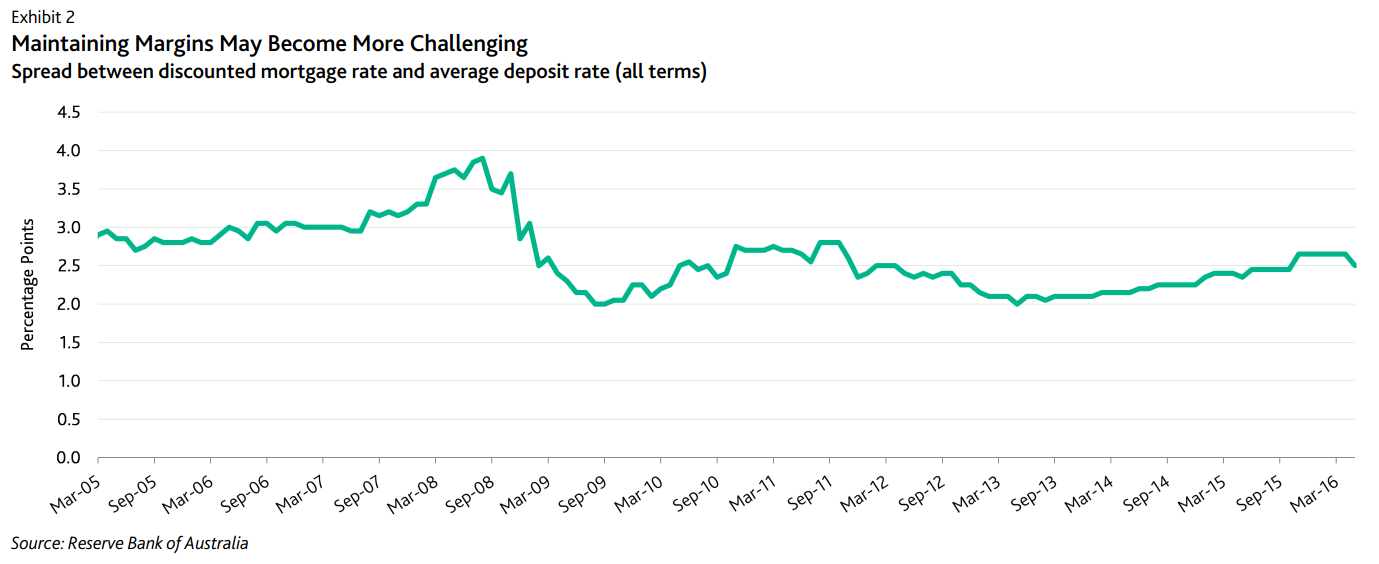

» We expect the banks’ interest margins and profit growth to come under downward pressure. Although to date the banks have managed to preserve margins through strong pricing power, Australia’s accommodative monetary policy – which is likely to persist over the next 12 months – will negatively impact the banks’ net interest margins. In addition, an expected increase in retail deposit competition – partly as a result of the incoming regulatory Net Stable Funding Ratio requirements – and, potentially, loan pricing competition will expose interest margins further.

» Australia’s credit conditions and housing risks are starting to pose increasing challenges. The low nominal income growth prevalent over the recent years and a buoyant housing market in key regions have led to an increase in household debt and overall credit-to-GDP ratios. The sustained house price appreciation and the resultant greater divergence between house prices and incomes has likely made households more vulnerable to financial and asset market corrections. Coupled with bank portfolios that have unusually high levels of concentration to residential mortgages, we believe that risks to Australian banks are increasingly skewed to the downside.

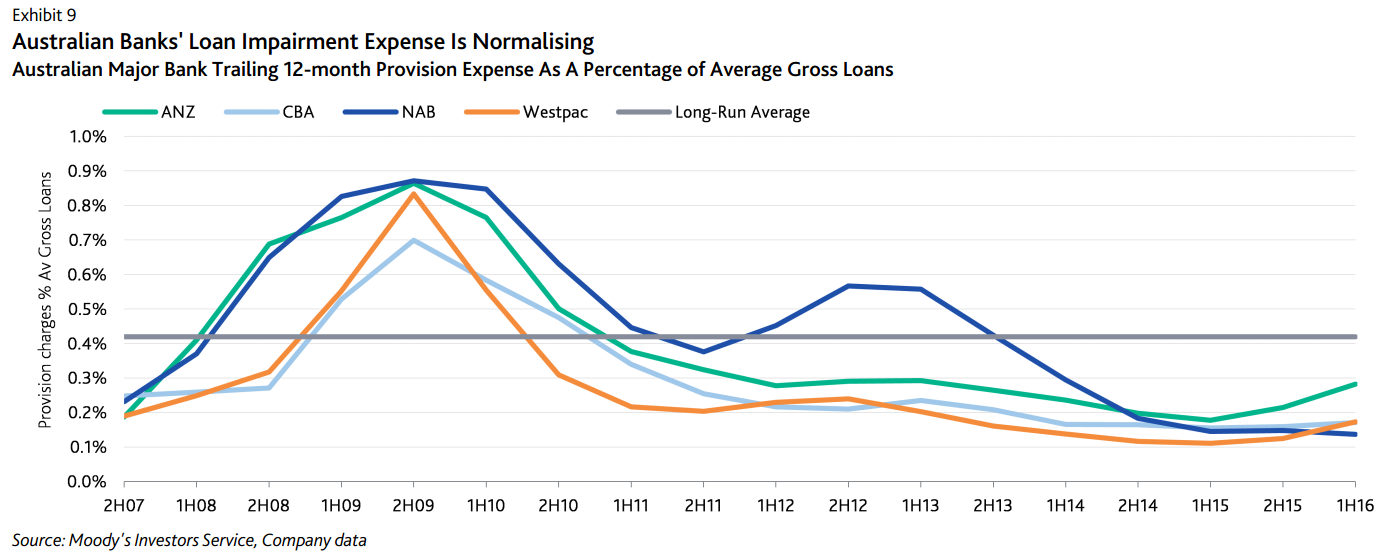

» Without countermeasures, slowing profit growth and rising housing risks could negatively impact the growth of loss absorbing buffers. Over recent years, regulation has strengthened the banks’ capital positions. Their funding and liquidity profiles have also improved, with a lower reliance on short-term wholesale funding and higher holdings of liquid assets. These improvements have been positive offsetting factors, supporting their ratings. However, we anticipate that the path of future balance sheet strengthening is likely to be slower than in previous years – at a time when risks continue to rise.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.