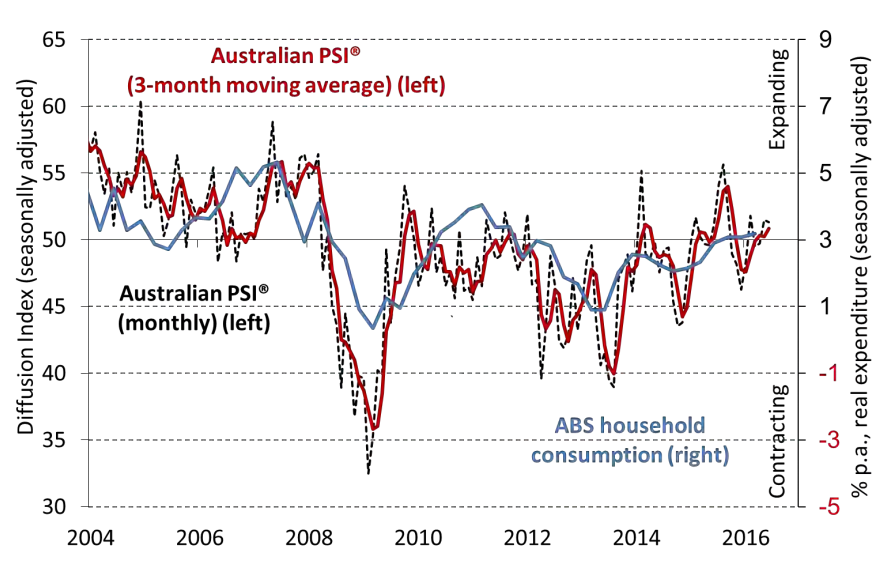

• The Australian Industry Group Australian Performance of Services Index (Australian PSI® ) fell by 0.2 points to 51.3 points in June, indicating a modest expansion in activity across the services sector for a second consecutive month (results above 50 points indicate expansion, with higher numbers indicating a stronger rate of expansion).

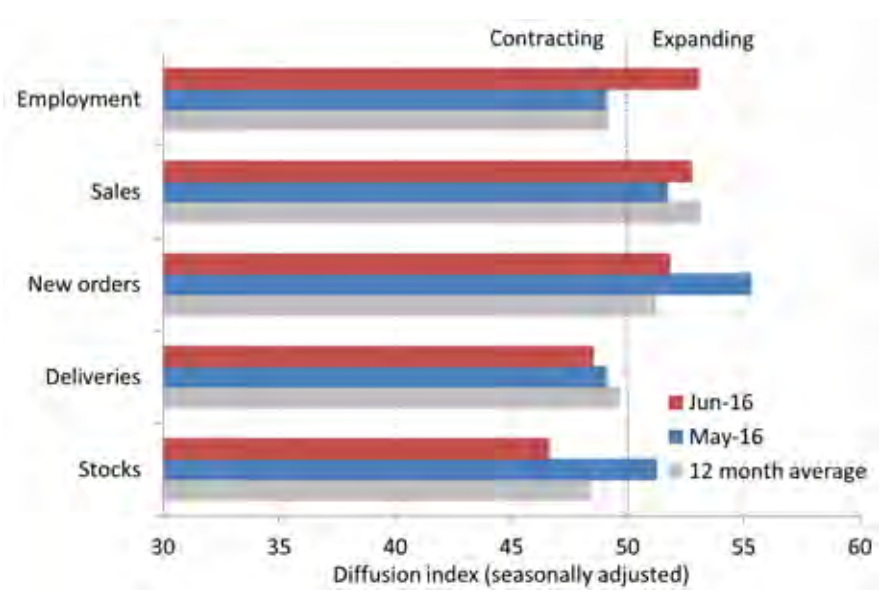

• Of the five activity sub-indexes in the Australian PSI® , employment (53.1 points) lifted 4 points into positive territory in June, its first positive reading since August 2015. Sales (52.8 points) picked up 1.1 points while new orders (51.8 points) lost 3.5 points, indicating a positive but slower pace of growth. Stocks (46.6 points) slipped into negative territory (down 4.6 points from May), while deliveries (48.5 points) remained negative, indicating a reduction in inventories and supplier deliveries for the end of the financial year in June.

• Two of the nine services sub-sectors in the Australian PSI® expanded in June (in three month moving averages) and two were stable. Retail trade (66.5 points and a record high for this sub-sector) and finance & insurance (66.8 points) expanded in June. Health &community services (49.4 points) and property & business services (49.4 points) were stable in June. Communication services (44.7 points), wholesale trade (42.0 points), personal & recreational services (39.9 points), hospitality (37.3) and transport & storage (36.2) all contracted, with a relatively faster rate of contraction evident in hospitality and transport.

• The input costs (63.3 points) sub-index of the Australian PSI® expanded more strongly in June, possibly indicating further price rises for imported products due to Australian dollar fluctuations. Selling prices (44.6 points) fell in June and wages (50.8 points) were stable for a second month, reflecting the low-inflation environment for local prices and wages at present.

• Respondents noted that recent winter weather may have had a positive effect on retailers and some other services businesses this month. However, the election period leading up to 2 July may have held back spending and orders for business-oriented service sectors in June.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.