Reserve Bank of New Zealand Deputy Governor Grant Spencer gave an excellent speech yesterday examining the growing imbalances in the New Zealand housing market and calling for a broad policy response from the Government on multiple fronts. Below are some of the key extracts.

On housing market conditions and risks, Spencer notes:

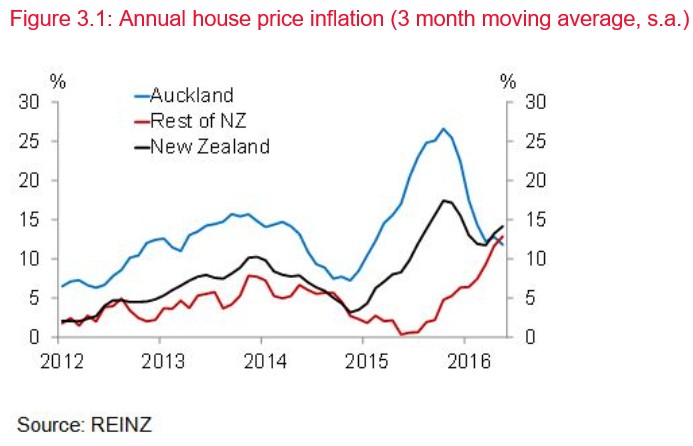

New Zealand is experiencing a housing market boom. House prices are increasing at 13 percent per annum nationally, and at 15-20 percent in Auckland and close-by regions. Evidence from housing cycles in several advanced economies suggests that the longer this continues, the more likely there will be a severe correction…

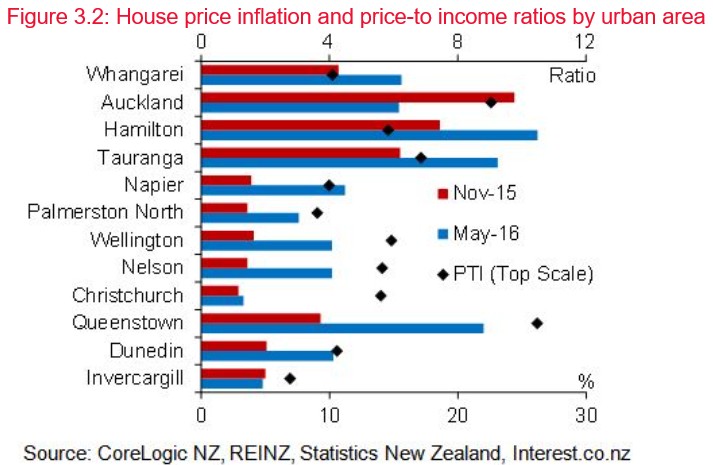

Auckland house price inflation in excess of income growth has seen the median house price to income ratio grow to 9.7 times in the most recent Demographia survey, making Auckland the fourth most expensive city relative to income out of 367 cities worldwide. This ratio is at an historical peak, having doubled since the early 2000s. Outside Auckland, house price to income ratios in most centres are around 4 to 6 (Figure 3.2). However, if house prices in the regions continue to grow at current rates, those ratios will worsen. Overall, New Zealand house prices relative to incomes are 32 percent above their long run average, and the second highest in the OECD. The IMF estimates that New Zealand house prices are around 20-40 percent overvalued based on long run affordability metrics.

The Reserve Bank is mandated to promote the soundness and efficiency of the financial system. Our concern is that a severe housing correction would pose real risks for financial system stability and the broader economy. The banks are heavily exposed to housing with mortgages making up around 55 percent of total assets. Household debt, at 163 percent of household income, is at a record level…

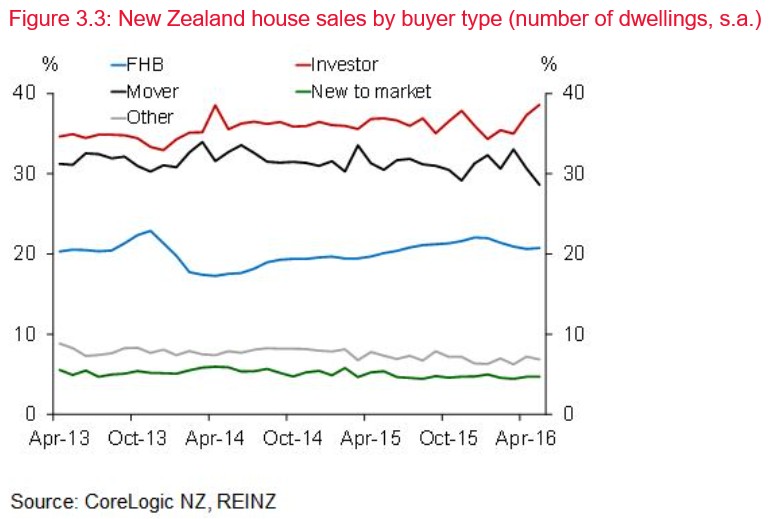

A dominant feature of the housing market resurgence has been an increase in investor activity (Figure 3.3). In recent months, investors have accounted for around 43 percent of sales in Auckland and 38 percent in other regions. Investor borrowing has maintained much of its momentum even though it is taking place at somewhat lower average LVRs. The prospect of capital gains appears to remain a key driver for investors in the face of declining rental yields.

The Reserve Bank considers that rising investor participation tends to increase the financial stability risks relating to the household sector in severe downturn conditions. Evidence from the UK and Ireland shows mortgage default rates significantly higher for investors (at any given LVR). There are likely to be a variety of reasons for this, but an important one is that owner-occupier households need to move out of their own home if they default, giving a powerful incentive to continue servicing their mortgages if at all possible. Investors do not face the same incentive for their rental properties and are also more likely to face income shocks (like rental vacancy) at the same time that house prices fall…

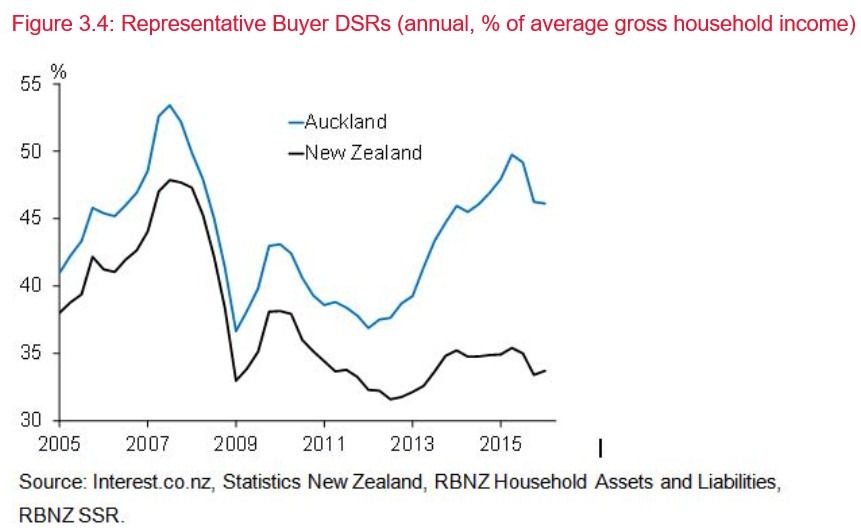

While a large increase in mortgage rates is unlikely in the current global environment, at today’s high debt-to-income ratios, a relatively small increase in interest rates could put significant pressure on some borrowers. This is particularly the case in Auckland, where DSRs for new buyers are close to 50 percent (Figure 3.4). A 1 percentage point rise in interest rates for these new buyers would boost the proportion of income devoted to mortgage servicing by around 5 percentage points…

Many domestic and international factors are contributing to the strength of the market. The current record low interest rates are a world-wide phenomenon linked to post-GFC caution and very low inflation in the global economy. Also driving local housing demand has been an unprecedented net migration inflow over recent years reflecting New Zealand’s stronger economic performance relative to many other advanced economies.

While strong demand has been underpinned by low interest rates, rising credit growth and population increases, the housing supply response has been constrained by planning and consenting processes, community preferences in respect of housing density, inefficiencies in the building industry, and infrastructure development constraints. The resulting housing market imbalance has been exacerbated by New Zealanders’ on-going preference for investment in bricks and mortar over financial investments, due in part to the ready availability of credit and a tax system that favours debt funded capital gains…

We estimate the shortage of houses in Auckland has increased over the past year and may now be in the order of 20,000-30,000 houses. Furthermore, the overall housing shortfall is expected to increase further as supply is growing more slowly than demand…

Spencer then calls for a broad policy response, imploring the Government to take action and assist the RBNZ to mitigate risks, which it cannot do on its own:

On-going supply-side constraints combined with rapid growth in the demand for housing continue to create significant imbalances in the housing market, particularly in Auckland. In order to relieve those imbalances, a range of initiatives is needed to increase the long-term housing supply response and moderate housing demand. The relevant policy areas extend well beyond financial policy and the responsibilities of the Reserve Bank. In this regard, we see the Reserve Bank as part of a team effort.

The Productivity Commission’s Report, Using land for housing, released in October 2015, notes that an insufficient supply of land ready for new housing remains at the heart of the rise in house prices seen in Auckland and other high growth areas of the country. Costly and restrictive planning rules and regulations, insufficient provision of infrastructure required to make land ready for development, and a planning system unable to respond adequately to changing demand patterns were among the factors the Commission cited as contributing to the shortfall in housing-ready land.

The Commission proposed a range of measures for the Government and local councils…

While boosting the capacity for development and housing supply is paramount, it is also important to explore policies that will keep the demand for housing more in line with supply capacity. Two areas for on-going consideration include tax and migration policy. On the tax front, the implementation of the bright line test for housing investors introduced in October last year has helped curb short-term speculative activity in the housing market. Consideration might be given to further reducing the tax advantage of investing in residential housing.

Like taxation of investor-owned housing, migration policy is a complex and controversial issue. However, we cannot ignore that the 160,000 net inflow of permanent and long-term migrants over the last 3 years has generated an unprecedented increase in the population and a significant boost to housing demand. Given the strong influence of departing and returning New Zealanders in the total numbers, it will never be possible to fine-tune the overall level of migration or smooth out the migration cycle. However, there may be merit in reviewing whether migration policy is securing the number and composition of skills intended. While any adjustments would operate at the margin, they could over time help to moderate the housing market imbalance…

The Bank’s interest rate policy must have regard to financial stability concerns, but the global environment is likely to keep interest rates low for some time yet. Macro-prudential policy can assist in containing the growing risk to financial stability as the current housing market reaches new extremes. In light of the growing risk, the Reserve Bank is closely considering measures that could be progressed in the coming months…

One is tighter LVRs to counter the growing influence of investor demand in Auckland and other regions, and to further bolster bank balance sheets against a housing market downturn… we expect that such a measure could potentially be introduced by the end of the year.

Another option is a new debt-to-income (DTI) speed limit to complement the LVR requirements by improving the resilience of household balance sheets to income or interest rate shocks. A DTI limit would make defaults less likely in a downturn. Furthermore, a DTI and LVR in combination would constrain credit growth and house price pressures on a more sustainable basis than would LVRs alone. A DTI would be a new instrument that would need to be agreed with the Minister of Finance… We intend to consult with the banks on the viability of a DTI policy and data issues before making a decision on implementation.

A third option is a housing capital overlay. The Reserve Bank has already indicated that it will be conducting a full review of bank capital requirements over the coming year. We will consider whether macro-prudential overlays have a role to play as part of that process.

As usual, the RBNZ has shown how a central bank and prudential regulator should be run. It has expertly explained the state-of-play and risks, highlighted its limitations on the policy front, and then called-on policy makers for assistance on both the supply and demand sides, including action on land supply, planning, tax policy, and immigration.

The RBNZ has effectively used its high profile to shame policy makers into reform, ensuring they cannot continue to ignore these issues lest they suffer the wrath of voters.

Advertisement

Now compare this open and transparent approach to the RBA and APRA. They rarely speak-up on issues and never explain to the public what reforms are needed to restore balance to the housing market and broader economy. They avoid political confrontation at all costs.

Accordingly, our policy makers have been given a free pass to continue blowing the bubble via ineffective supply-side policies, distortionary tax policies, weak controls on money laundering, as well as sustained high immigration, much of it from questionable sources.

In short, the RBNZ is a real central bank and prudential regulator, whereas RBA/APRA are nothing more than paper tigers.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.