From UBS, comes more on the well-timed and much needed surge in public investment:

Reiterating our view of stronger public spending supporting GDP ahead

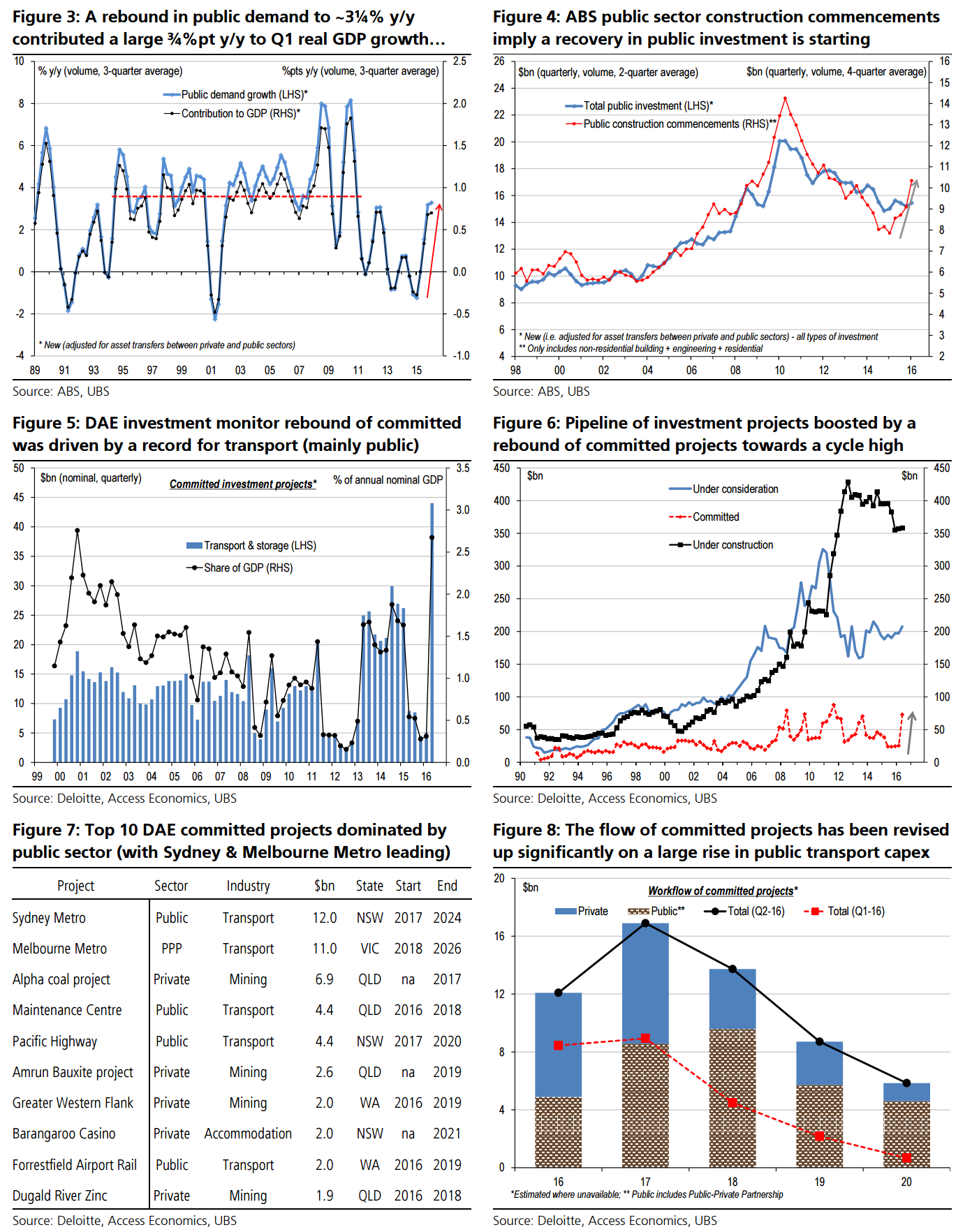

We recently highlighted (Public spending surprises…capex boost ahead) that there has been a long-awaited – but stronger than expected – rebound in government spending (or public demand). Real public spending has lifted to a trend of ~3¼% y/y, adding a significant ~¾%pt to GDP, the biggest since the tail-end of the GFC stimulus.

Public capex set to surge ahead based on commencements & Budget forecasts

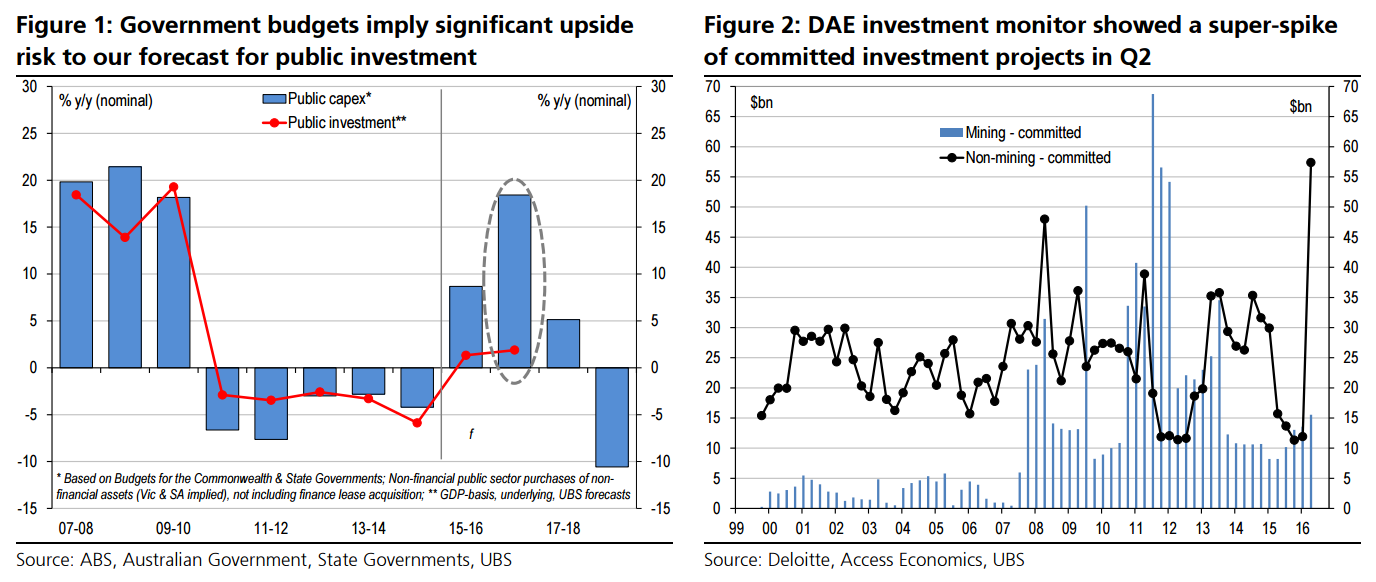

Meanwhile, the capex/investment part of public spending is now also turning up sharply. After public investment collapsed by ~30% from 2010 to 2015, the recent bounce of construction commencements now points to a recovery ahead (Figure 4). Indeed, our detailed analysis of Government budgets implies that public capex/investment could potentially jump by ~15% y/y in 16/17, which is well above our current forecasts (Figure 1).

DAE Investment Monitor ‘confirms’ – with a ‘super spike’ in committed projects

Further to this, our analysis has now also been ‘confirmed’ by the just released Deloitte/Access Economic Investment Monitor. The DAE data showed a ‘super spike’ in Q2 of committed investment projects (Figure 6), up 205% y/y (to $73bn, or 4.4% of nominal GDP). While there has also been a notable bounce of mining from a depressed level (+90% y/y to $16bn or 0.9% of GDP), the key driver has obviously been nonmining (+266% y/y to a record $57bn or 3.5% of GDP), dominated by a spike of public-related spending on transport mainly in NSW & Victoria (Figures 2, 5 and 8). We also detail the top 10 committed projects in the DAE data, showing this concentration (Figure 7). Overall, the DAE data adds to our view that a much faster pace of public spending could provide a significant medium-term buffer against any future drag from a peaking housing market.

That’s one Hell of a spike even if nothing like what is needed relative to rising populations.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.