The NAB survey for June is out and it is cruising:

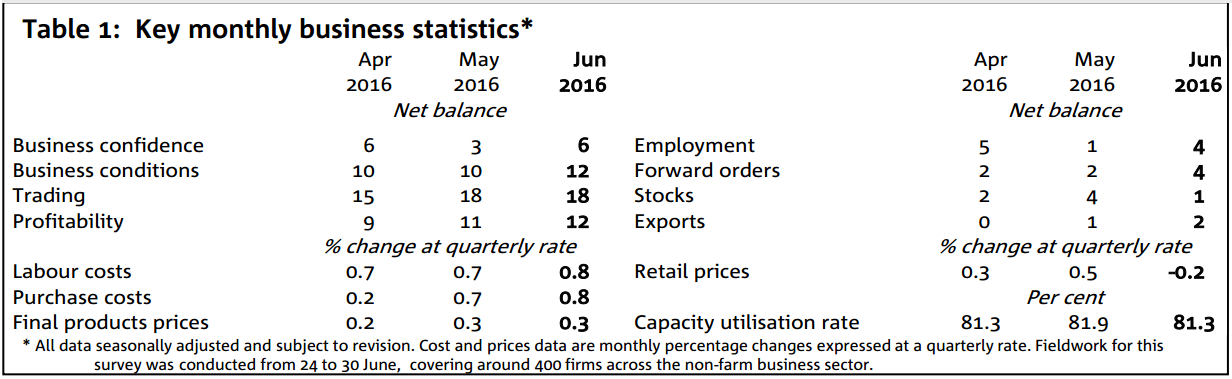

This month’s NAB Business Survey was undertaken right amidst the heightened uncertainty around the Brexit referendum, and ahead of the Australian Federal election. Despite the disruptive nature of these events (evident in the financial market volatility following the Brexit vote), it was encouraging to see that business confidence continued to see support from consistently above average conditions in non-mining sectors. In fact, business confidence jumped in June to +6 index points, which is consistent with long-run confidence levels. While there is potential for the unsettled post-election political environment to have an impact on confidence, this month’s outcome suggests that firms remain more focused on economic conditions. In that respect, it was reassuring to also see an improvement in some of the leading indicators, including forward orders and capex – although capacity utilisation did ease back a little.

• Business conditions lifted from their already elevated level in June, to +12 index points (from +10), which is around its highest since the GFC. Services remain the best performers, although retail pulled back considerably – consistent with a large drop in retail prices, which could reflect an escalation of competitive pressures in the sector. That is a surprising contrast to wholesale – sometimes considered a bellwether for the economy – which has been consistently improving of late. The rise in business conditions was due to a notable improvement in employment demand, although profitability also rose, while trading conditions were unchanged at very elevated levels. Employment conditions are now back above long-run average levels, suggesting solid near-term employment growth. Inflation measures in the Survey were broadly steady, although a drop in retail prices may have implications for CPI.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.