By Chris Becker

You get a car! You get a car! You all get a car! Yes, central banks are turning into Oprah handing out free cash to all and sundry in an effort to Viagra-ise risk markets eight years after the GFC, with the Bank of Japan and the Bank of England both expected to add to the flooded pool of liquidity later this week. A possible second referendum on Brexit with a new PM is also bringing bid back to the Pound, as European stocks almost reach their pre-Brexit highs and the FTSE making gains! Commodities are mixed on the reflation bid, with Brent crude soaring over 4% dragging WTI up with it, while industrials like copper flounder. Gold fell again but is looking oversold while Aussie dollar rose with the commodity complex.

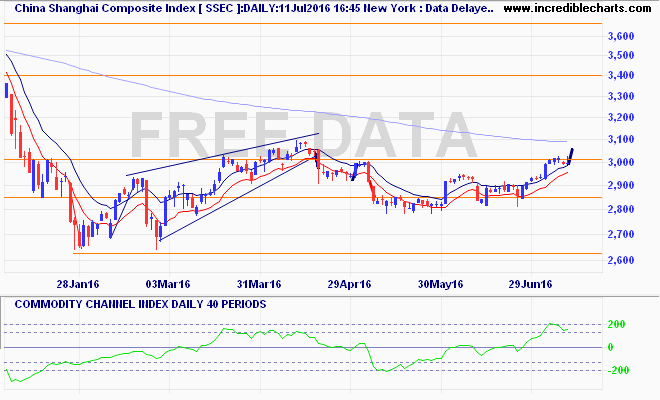

Recapping Asia yesterday and the Shanghai Composite finally had a solid close above resistance at 3000 points, rising 1.8% to 3050 points. The next level to reach here is the 200 day moving average and the March high and then we might be off to the races to 3400 points. I’m watching though for internal breakdown via momentum indicators for a short swing setup as always: