by Chris Becker

Another solid day of action in Asia, mainly in currencies as the fallout from Friday’s NFP print plus continued Brexit shenaginans are felt on risk markets. First to currencies, where I’ve got a triple whammy for you:

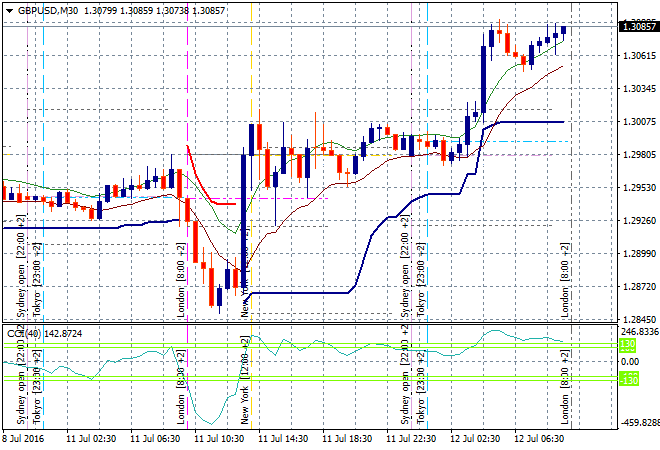

First the pound has rallied through the Asian session – unusual but not unexpected given the Brexit shakeout. It looks like the once great Empire will have a new Conservative PM by this time tomorrow and markets are liking the certainty…if not thinking about the future! This breakout on the intrasession charts is not confirmed by the dailies, so watch out:

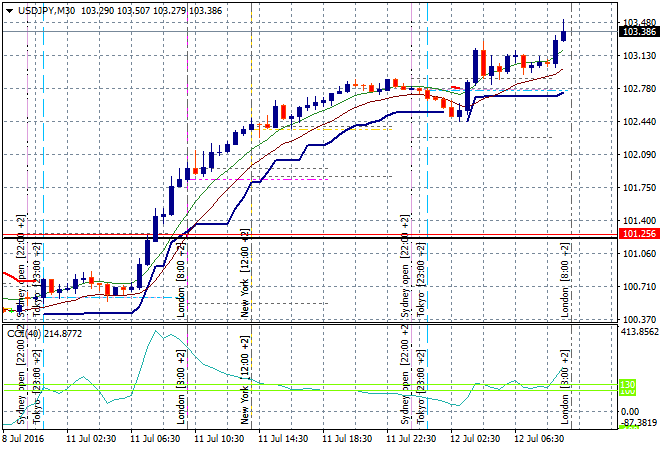

Yen is going the other way as more stimulus looks set to be thrust upon another failed Empire. Just before The City opened, USDJPY pipped up above 103, almost breaking out on the daily charts but clearly making a run for it here.

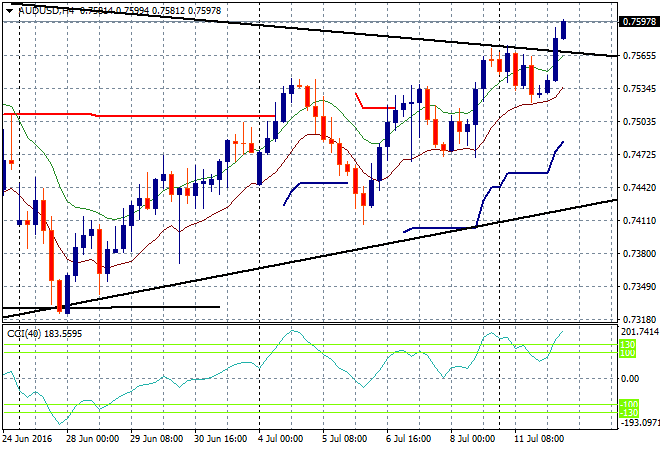

Finally to the currency we all love to hate, the Aussie dollar also broke out but more significantly is breaking longer term markets, hitting the 76 handle and breaking above the downtrend line from the pre Brexit high. My target remains the 78 handle or a little higher, which is still setting up for a nice longer term short.

In stocks, the Shanghai Composite broke out post-lunch break and is currently up nearly 2% to 3050 points while the Nikkei is up higher on the back of the weaker Yen, nearly 2.5% at the close. The ASX200 is the ugly girl at the ball, only up 0.3% but it did do better in the middle of the session. Banks did the heavy lifting today, with the financials index up nearly 1%

The economic calendar heats up tonight with Germany’s final CPI print for June, followed by the results of the BOE financial stability meeting, including a speech by Governor Carney to the British Parliament regarding Brexit. So all eyes on the Pound and Euro! Not much in the US session, the wholesale inventory report for May plus some bond sales. The key thing to watch is if US industrial stocks can maintain the momentum following the risk-on move from Friday’s employment figures.