From Macquarie Securities:

Surviving feels like the appropriate tactic in the current market. We are getting more defensive – reducing exposure to Financials and Resources and up weighting further into the growth and yield plays.

The question for portfolio and country allocation is whether banks now offer better risk reward over REIT’s and other yield plays (we are not buying them for earnings growth). The fundamental valuation case for banks is difficult to ignore. They trade at a 30% discount to REIT’s, they are close to a record high yield differential over bonds (450bps) and they have never had a more favourable yield differential over REIT’s (nearly 200bps). However, yield is being priced off both declining bond yields and a combination of earnings certainty, growth and volatility. Banks have none of the latter and on a relative basis REIT’s will grow 4% faster than banks over the coming 12 months according to bottom up forecasts.

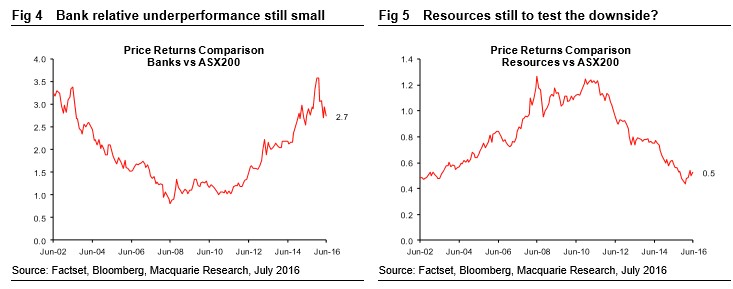

Banks face an increasing multitude of concerns. We are not subscribers to the valuation argument at this stage. It is true that banks are now at a 30% discount to the market and at a reasonable discount to their historic relative valuation (0.9x). However, they no longer resemble the past and until relative earnings growth improves, we worry that the valuation support doesn’t stand in isolation. Against these concerns, we prefer to pay an even larger premium for yield and consequently take our banks overweight back to neutral. We are not moving underweight on banks. They still have some earnings levers to pull and they could well grow faster than the market in 2017. This remains a tail event outcome but earnings expectations are aggressively optimistic for Industrials and ultimately resources if the A$ remains above US$0.75 (current levels)…

Outside of banks, we were already defensive (overweight Telcos/Utilities/Infrastructure and underweight Resources) but it feels this is not enough given the escalation of risks – stock specific and macro related – and the absence of upside catalysts outside of another round of monetary easing which is likely on its way but only after more pain for risk assets we would guess.

We are reducing exposure to Financials and Resources and up weighting further into growth and yield. Too little too late? It feels like the market has fallen a lot but at ~5200 it is still 8% off the YTD lows and we are trading a long way off pure valuation support (the long term average). A bear case scenario would easily see the market take out its lows and trade outright cheap. At 14x forward earnings and 3% EPS growth this equates to an index level of ~4700 – for every 1PE point this is around 330 points on the index…

We think markets have gotten a little ahead of themselves in the post BREXIT rebound. Second order effects either via financial market tightening and the risks that this poses for growth remain significant. The spread in returns for financial versus non financials and the widening in peripheral bond spreads continue to highlight the ongoing risk via financial market contagion.

Our house view is that BREXIT will have only a modest impact on global growth and that central banks will provide the necessary shock absorber. This may be the case, but we think this reduces downside risk rather than creating a lot of upside risk. We are more cautious on how equities will react to the ongoing uncertainty and second round growth risks. The self fulfilling nature of weakness in the financial stocks (recapitalizing may prove difficult given regulatory hurdles in the EU and the dilution in building capital buffers) is another overhang on our own financials.

We believe this creates a backdrop where it will be difficult for our bank and resource stocks to outperform. Banks are now at the epicentre of rising political risk on top of capital, collateral, competition and funding concerns. Unlike pure yield plays (i.e REITS & Telco’s), bank earnings growth becomes harder to generate as rates move lower (repricing just becomes an offset).

We are taking our Banks position back to Neutral and increasing our Underweight position in Resources. Our key strategy is to get even more Defensive – we have increased our weights in REITs to Overweight (previously Neutral) and in stock specific names within Telcoms, Infrastructure & Utilities that drive a bottom-up overweight.