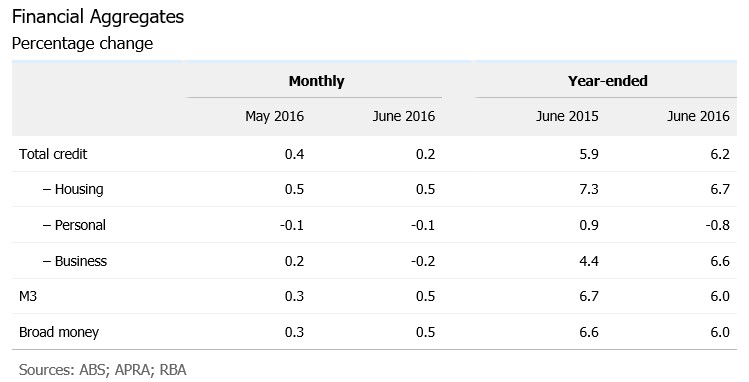

The Reserve Bank of Australia (RBA) has released its private sector credit aggregates data for the month of June:

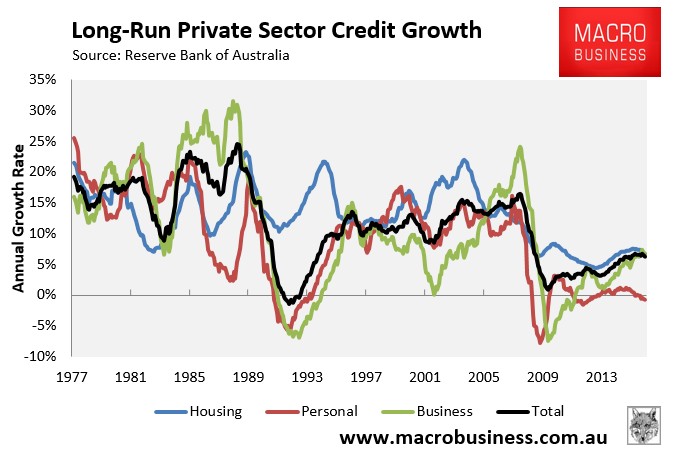

A chart showing the long-run breakdown in the components is provided below:

Personal credit growth (-0.1% MoM; -0.3% QoQ; -0.8% YoY) is still in the gutter, whereas business credit growth (0.2% MoM; 0.8% QoQ; 6.6% YoY) is solid but slowing. Housing credit growth (0.5% MoM; 1.4% QoQ; 6.7% YoY) is also solid, but remains below its long-run average growth rate (although in dollar terms it remains high).

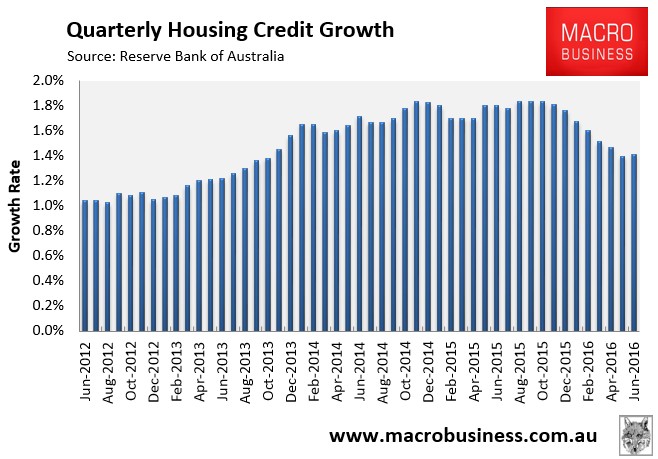

The below chart shows that quarterly housing credit growth has stabilised after slowing abruptly over the first half:

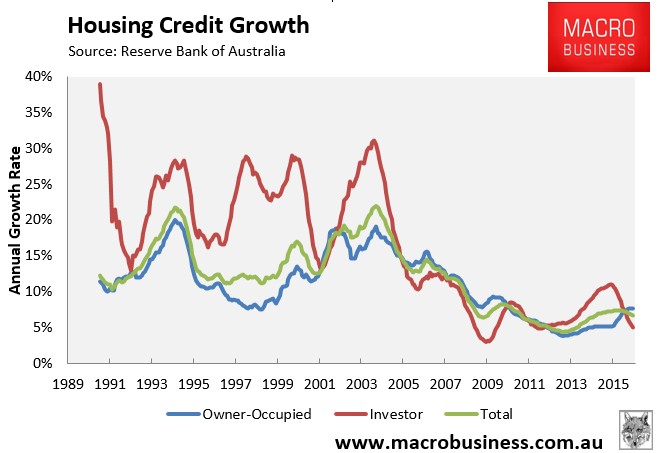

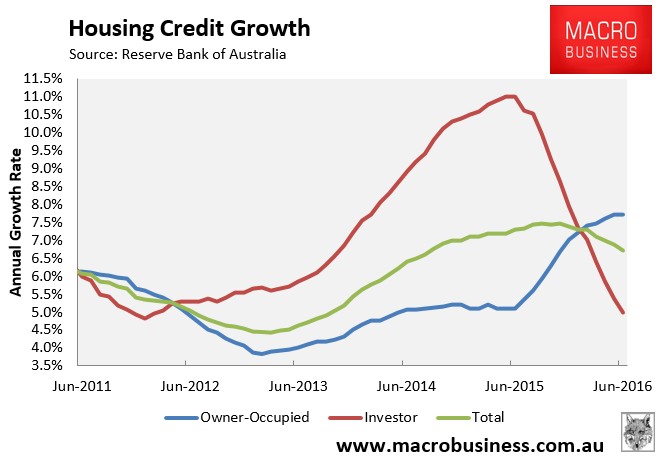

A long-run breakdown of owner-occupied credit (0.51% MoM; 1.56% QoQ; 7.72% YoY) and investor credit (0.42% MoM; 1.11% QoQ; 5.00% YoY) is provided below:

Investor credit growth continues to slow abruptly, whereas owner-occupied credit growth has stabilised. And the overall trend in housing credit growth is down:

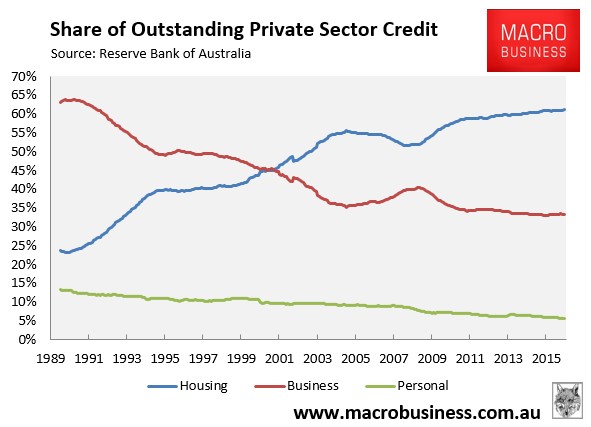

The share of loans going to housing hit another all-time high at 61.1% as at June 2016. By contrast, the share of total loans to businesses was at 33.24% as at June, which is fractionally above June 2015’s record low:

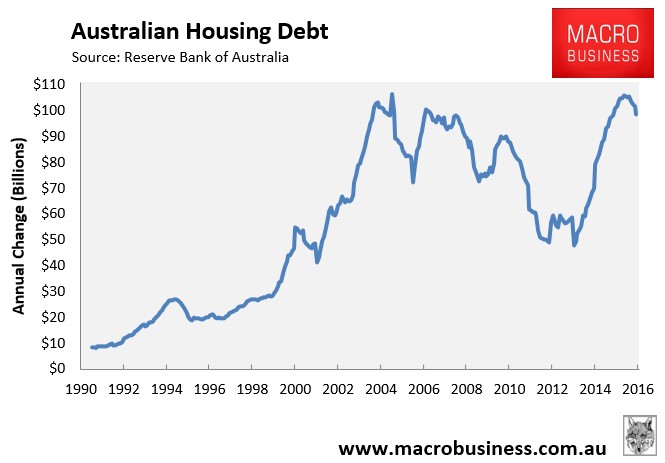

Finally, in nominal dollar terms, the annual change in outstanding Australian mortgage debt retraced again in June from February’s record high. That said, mortgage credit still grew by a strong $98.5 billion in the year to June 2016, although this was down 2% year-on-year:

Thus, housing credit remains a weakening (albeit imperfect) indicator for Australian housing, which again contradicts somewhat the recent surge in house prices.