For years, MB has argued that one’s principal place of residence must be included in the assets test for the Aged Pension on both equity and Budget sustainability grounds.

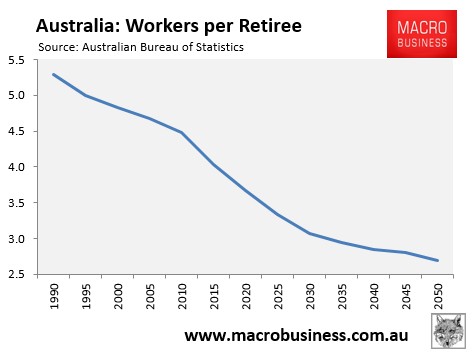

The underlying need for further Aged Pension reform can be boiled down to: 1) the fact that the ratio of workers supporting retirees is set to decline for decades:

And 2) that the Aged Pension (currently $44.2 billion in 2015-16 and rising to $52 billion by 2019-20) is the largest and one of the fastest-growing Budget expenses.

These factors alone make it inevitable that Aged Pension reform will be required sooner or later.

The release today of the 2016 Household, Income and Labour Dynamics in Australia (HILDA) survey added further weight to this argument.

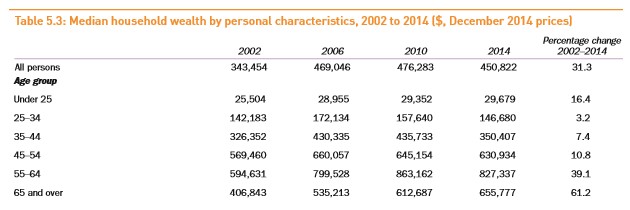

The HILDA survey showed a rapidly growing wealth divide, whereby median wealth increased by 61% among those aged 65 and over between 2002 and 2014, compared with just a 3.2% increase in wealth among those aged 25 to 34:

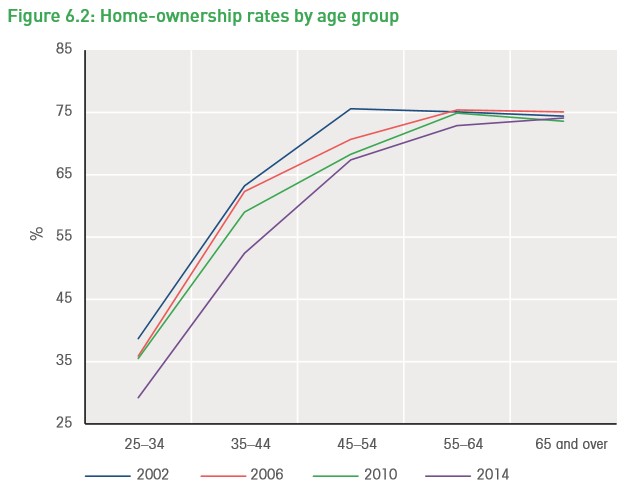

The HILDA survey also showed that while home ownership has collapsed for younger cohorts, those aged 65 and over have experienced stable ownership whereby roughly 75% own a home:

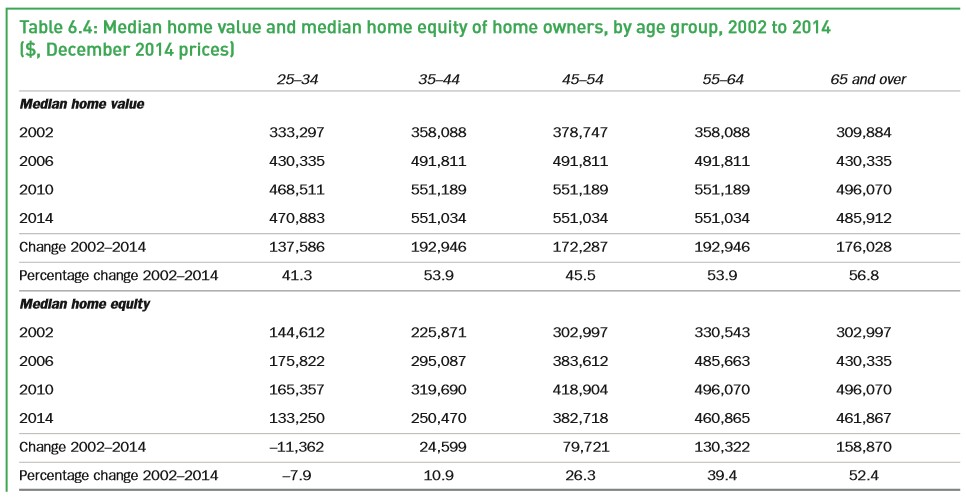

Meanwhile, those aged 65 and over have also experienced the biggest rise in median home equity, which stood at a whopping $461,867 as at December 2014:

So, Australia effectively finds itself in the perverse situation whereby relatively poorer younger Australians are heavily subsidising the retirements of their well-off parents and grandparents, whose biggest asset (their principal place of residence) is largely excluded from their ability to fund their own retirements.

This situation makes absolutely no sense from either a budgetary or an inter-generational equity perspective.

For these reasons, MB strongly supports the following reforms to the Aged Pension to better balance Budget sustainability and equity:

- Include one’s principal place of residence in the assets test for the Aged Pension at some point in the future (e.g. 1 July 2020), thus allowing current retirees and prospective retirees adequate time to make arrangements.

- Once implemented, raise the overall assets test for the Aged Pension, and perhaps the base rate as well.

- Extend the existing state sponsored reverse mortgage scheme, the Pension Loans Scheme, to all people of retirement age so that asset (house) rich retirees can continue to receive a regular income stream in exchange for a HELP-style liability that is recoverable from the person’s estate upon death, or upon sale of the person’s home (whichever comes first).

Under this plan, house-rich pensioners could continue to receive a regular income stream as they do now under the Aged Pension, but with less drain on the Budget and on younger taxpayers. Whereas poorer renting pensioners would receive greater financial assistance.

Without reform to the Aged Pension, the burden of Budget cuts/tax increases will fall entirely on the growing pool of younger (and renting) Australians. This situation is clearly unsustainable from a Budget perspective and inequitable from an inter-generation one.

Other notable analysts have similarly called for the family home to be included in the assets test for the Aged Pension, including The Productivity Commission, The Grattan Institute, The ACCI, and the The CIS.

Unfortunately, while the economics is straight forward, the political economy is not. Watch landed retirees continue to fight like wounded bulls against reform.

unconventionaleconomist@hotmail.com