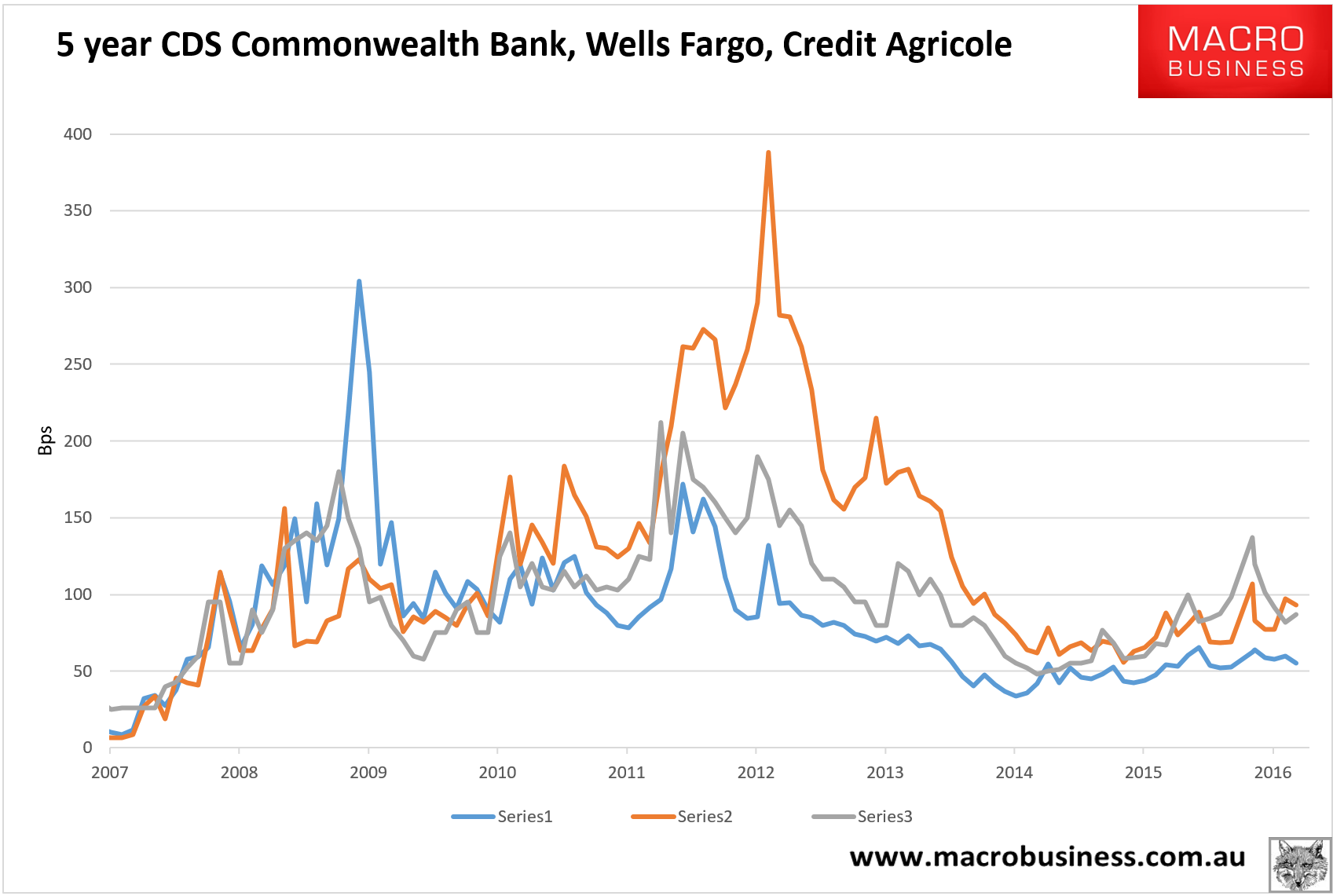

Some clear evidence that yesterday’s S&P negative watch on everything Australian debt did impact banks spreads. CBA CDS widened 2% to 87bps:

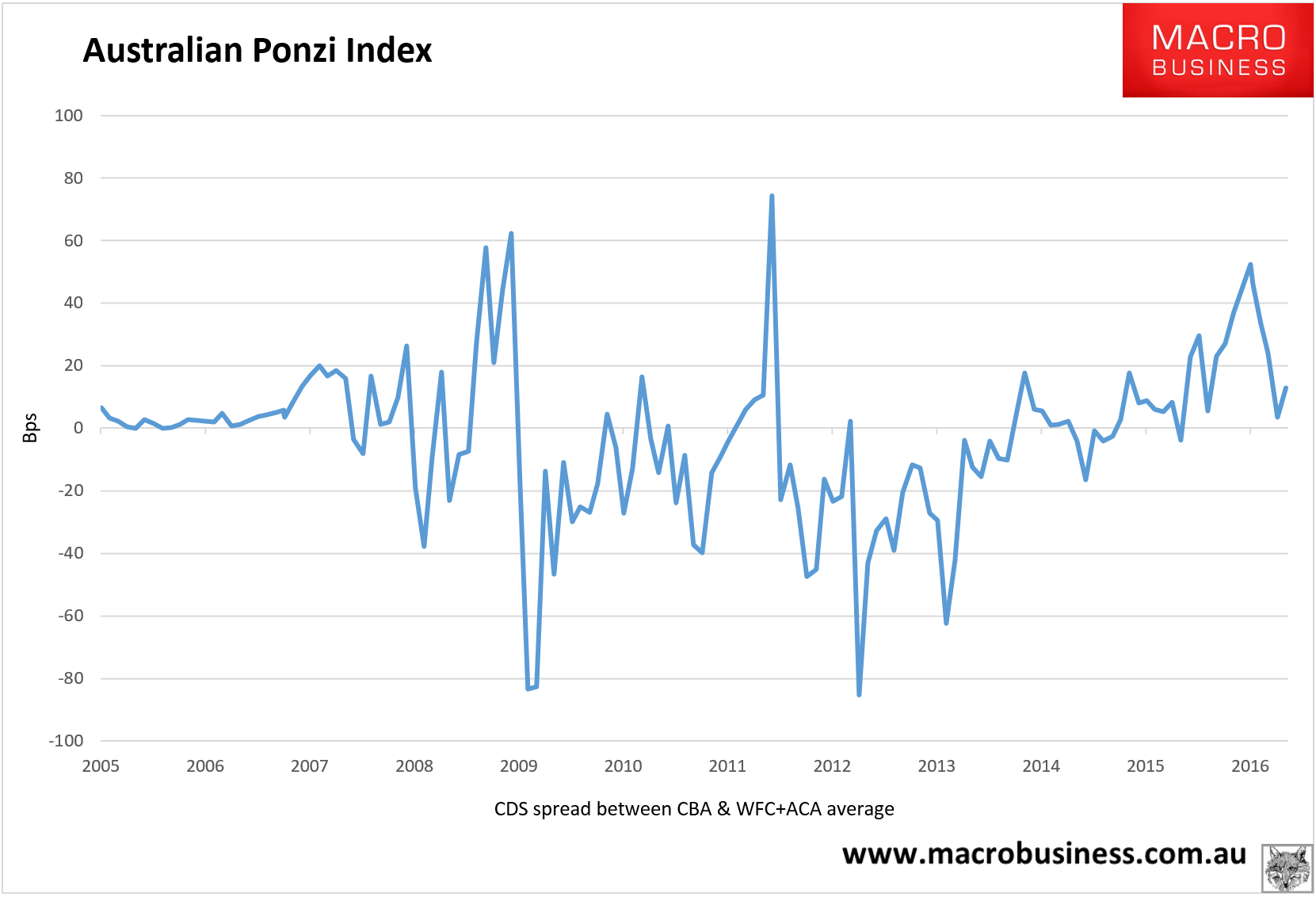

On the same day, our European proxy, Credit Agricole, saw an easing in spreads of -1.6% and our US proxy, Wells Fargo, eased -3.5%. Thus the Australian Ponzi Index rose strongly from recent lows:

Advertisement

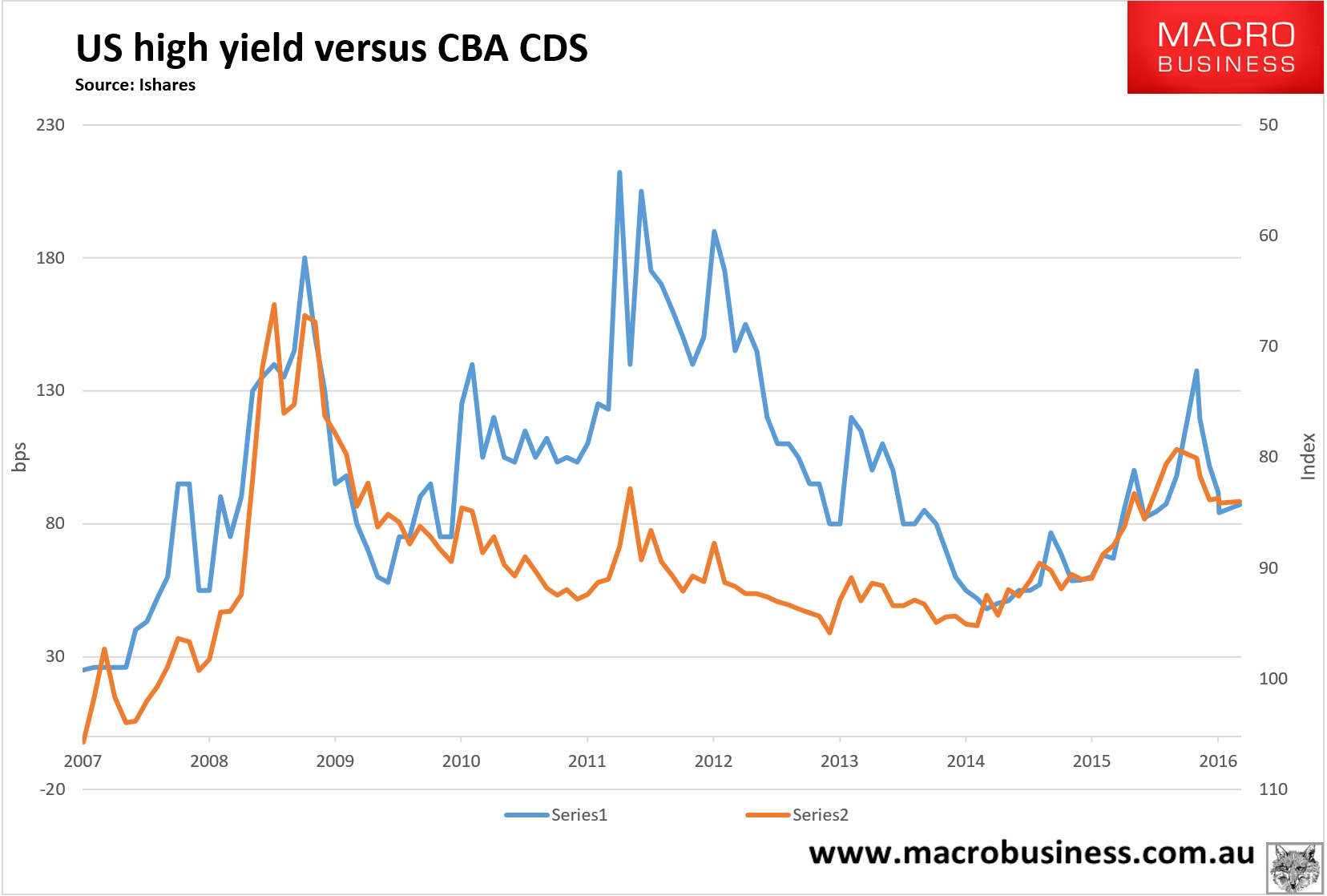

There was no movement in global high yield to speak of: