Here’s yesterday’s S&P release in full (apologies for delay, was sick yesterday):

Australia Outlook Revised To Negative On Growing Fiscal Vulnerabilities; ‘AAA/A-1+’ Ratings Affirmed

OVERVIEW

The sovereign credit ratings on Australia benefit from the country’s strong institutional settings, its wealthy and resilient economy, monetary policy flexibility, and low government debt.

The country’s high external and household indebtedness, as well as vulnerability to weak commodity export demand, moderate these strengths.

We are revising the rating outlook on Australia to negative from stable because we believe that without remedial action the government’s fiscal stance may no longer be compatible with the country’s high level of external indebtedness. We are also affirming the ‘AAA’ long-term and ‘A-1+’ short-term sovereign credit ratings on Australia and Efic.

RATING ACTION

On July 7, 2016, S&P Global Ratings revised its rating outlook on the Commonwealth of Australia to negative from stable. At the same time, we affirmed our ‘AAA’ long-term and ‘A-1+’ short-term unsolicited sovereign credit ratings on Australia. In addition, we revised the outlook on Export Finance & Insurance Corp. (Efic) to negative from stable and affirmed the ‘AAA’ long-term and ‘A-1+’ short-term issuer credit rating on the company. Efic is wholly owned by the government, which guarantees all of its obligations.

RATIONALE

The negative outlook on Australia reflects our view that without the implementation of more forceful fiscal policy decisions, material government budget deficits may persist for several years with little improvement. Ongoing budget deficits may become incompatible with Australia’s high level of external indebtedness and therefore inconsistent with a ‘AAA’ rating.

Along with strong institutions, a credible monetary policy, and floating exchange rate regime, Australia’s public finances have traditionally been a credit strength for the sovereign rating. Since the global financial recession of 2008-2009 and more recently the end of the mining boom, Australia’s fiscal position has continued to weaken with successive governments, delaying an eventual return to budget surpluses. Given the outcome of the July 2, 2016, double-dissolution election, in which neither of the traditional governing parties may command a majority in either house, we believe fiscal consolidation may be further postponed.

The central government’s current projection date for a balanced budget in fiscal year 2021 (the year ending June 30, 2021) is now eight years later than the previous government’s earlier projection of fiscal year 2013, which it made in 2009; and, if achieved, it would come more than 10 years after the global recession initially pushed the central government budget into deficit.

Since this time last year, fiscal deterioration has continued, albeit to a more moderate degree than in earlier years. The government’s budget for fiscal 2017 forecasts that budget deficits to be, on average, 0.5% of GDP weaker each year over fiscal years 2016-2019, compared with its previous budget. This also means that, at the central government level, budget deficits have been little changed over the three years to fiscal year 2016.

While we expect that fiscal deficits will improve over the medium term, we are more pessimistic about the central government’s revenue outlook than the government was in its latest budget projections. S&P Global Ratings projects iron ore prices to be close to US$20 per metric ton, lower than the level assumed in the government’s budget in the remainder of calendar 2016 and in 2017, although the impact on the mining sector’s profits may be partly offset by a weaker currency. Aside from commodity prices, we also consider that there remains downside revenue risk if Australia’s inflation and wage growth is weak for longer than the budget anticipates. In addition, there remain government savings decisions, equivalent to 0.1%-0.2% of GDP each year, to which the parliament so far has not assented, and may continue to block post-election.

Our fiscal measures incorporate all levels of local, regional, and central government (the general government). At the state government level, we expect fiscal deficits to re-widen in the next couple of years, after narrowing in recent years, largely as states boost their infrastructure spending plans. This is adding to the outlook for general government sector fiscal deficits, although the impact on debt will likely be tempered by state asset privatizations. Overall, we expect net general government debt to remain low but to peak a little higher than we previously thought, at about 23% of GDP, reflecting our revised fiscal outlook. Low interest rates are also helping keep the general government sector’s interest expense burden low at less than 5% of revenues.

We consider that Australia’s general government sector fiscal outcomes need to be stronger than its peers’, and net debt needs to remain lower, to remain consistent with the current ‘AAA’ rating. This is because Australia’s economy carries a high level of net external debt. Several ratios reveal this weakness. Australia’s external debt net of public and financial sector assets (our preferred stock measure) is over three times current account receipts (CARs). The current account deficit will reach nearly 5% of GDP this year and only moderate slightly during the forecast horizon to just over 3%. Australia’s 2016 gross external financing requirement of US$630 billion is over half of GDP.

That said, Australia’s high stock of external debt and structural current account deficits are mostly generated by the private sector and they reflect the productive investment opportunities available in Australia, foreign investor confidence in Australia’s rule of law, the high creditworthiness of its banking system, and the positive yield available on highly rated debt. A portion of Australia’s external debt has also funded a surge in unproductive household borrowing for housing during the 1990s and 2000s, which was intermediated by the banking sector. Household debt (including debt for small businesses) now stands at more than 180% of household income.

We expect Australia’s external borrowers to maintain easy access to foreign funding. We note that the Reserve Bank of Australia (RBA, the central bank) has maintained a freely floating exchange rate regime for over three decades; that the Australian dollar represented 1.9% of allocated international reserves as of March 31, 2016; and that the currency is represented in a comparable percentage of spot foreign exchange transactions.

We consider Australia’s banking system to be one of the strongest globally, and assign a Banking Industry Country Risk Assessment score of ‘2’ (on a scale of ‘1’ to ’10’, with ‘1’ being the lowest risk). Australia’s domestic bond market is deep and although external borrowing is high it is mostly denominated in the nation’s own currency or hedged.

We also view Australia as possessing a high degree of monetary credibility. This key credit strength helps the country to attenuate major economic shocks—as could come, for example, from a sharp downturn in China’s economy or a slump in Australia’s property market. The RBA’s success in anchoring inflation expectations would, we believe, allow it to lower policy interest rates from their current level of 1.75% to support growth even should the currency weaken further, given the historical low pass-through to inflation.

Australia is a wealthy, diversified and resilient economy, with GDP per capita of an estimated US$51,000 in fiscal year 2016. This high level of wealth derives from strong institutional settings and decades of economic reform, which have facilitated the country’s flexible labor and product markets. The economy’s resilience and flexibility, we believe, ultimately help cushion government finances from economic shocks and are a major support to Australia’s creditworthiness.

Economic growth is now lifting after a period of below-trend economic performance. We estimate headline GDP growth to be around 3% in fiscal year 2016, and the unemployment rate has fallen from last year’s cyclical high. Significant currency depreciation is spurring services exports, particularly education and tourism. Low nominal interest rates, coupled with pent-up underlying demand, have been encouraging growth in dwelling investment for some time, and household consumption growth has strengthened. And while resources investment is still falling, resource export volumes keep rising as new capacity is brought on line–even though commodity export prices are much weaker than before. We expect growth to remain firm over our forecast period, and project real per capita GDP growth to average about 1.3% per year over 2016-2019.

The outlook on Efic is reflective of our equalization of the ratings on the company with the sovereign ratings due to the legislative guarantee the government provides over Efic’s obligations.

OUTLOOK

The negative outlook on Australia reflects our view that prospects for improvements in budgetary performance have weakened following the recent election outcome, and that general government sector deficits may remain material over our forecast period, with government debt continuing to rise, unless more budget savings measures are legislated or there are improvements in the revenue outlook.

There is a one-in-three chance that we could lower the rating within the next two years if we believe that parliament is unlikely to legislate savings or revenue measures sufficient for the general government sector budget deficit to narrow materially and to be in a balanced position by the early 2020s. We will continue to monitor, over the next six to 12 months, the success or otherwise of the new government’s ability to pass revenue and expenditure measures through both houses of parliament.

We could also lower the rating with any further weakening of Australia’s external position. This could come from current account deficits remaining at the higher end of the historical range, from a further weakening of terms of trade, or from an increase in the banking sector’s cost of external funding.

The ratings could stabilize if new budget savings or revenue measures were enacted that appeared sufficient to reduce fiscal deficits materially over the next few years. A sharp narrowing of current account deficits and external debt due to a favorable export performance could also cause us to change the outlook to stable, although this appears unlikely over the next two years.

KEY STATISTICS

OK, so the negative outlook (and inevitable) subsequent downgrade come from:

too much offshore debt;

failed fiscal consolidation, and

the absurd outlook in the Budget of Lies.

Advertisement

Ironically, what strikes me is how generous is S&P’s economic outlook. The Budget of Lies forecast $60CFR iron ore and S&P is forecasting $40CFR. My outlook to 2019 (and that of the futures market) is $40 next year, $35 in 2017 and $30 after that.

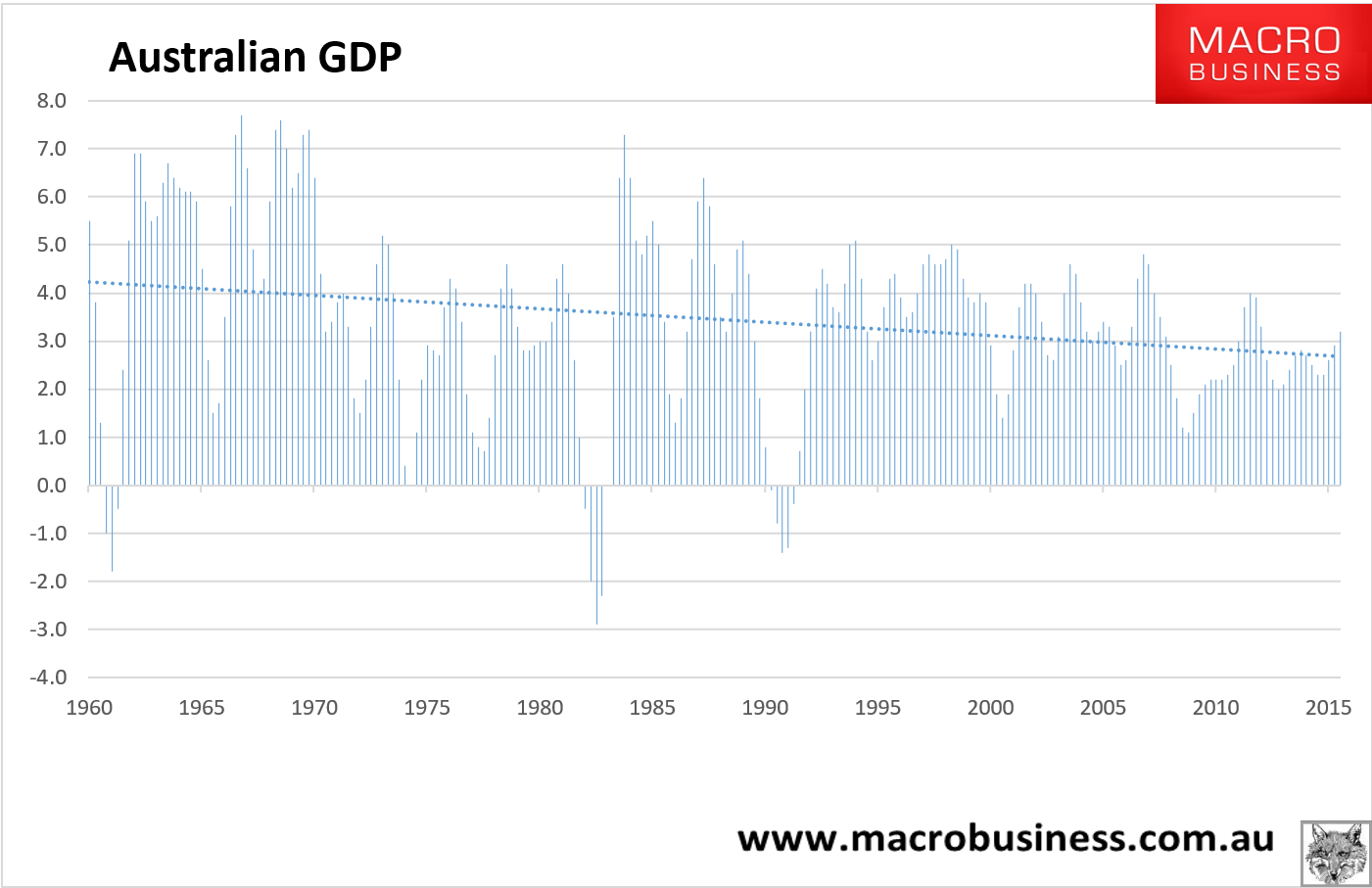

I’ll happily admit that I’m at the bearish end of forecasts but S&P is not. Yet even so, its outlook for growth is very generous at 3% in perpetuity, a rate we’ve barely managed post-GFC with an average of 2.5%:

Advertisement

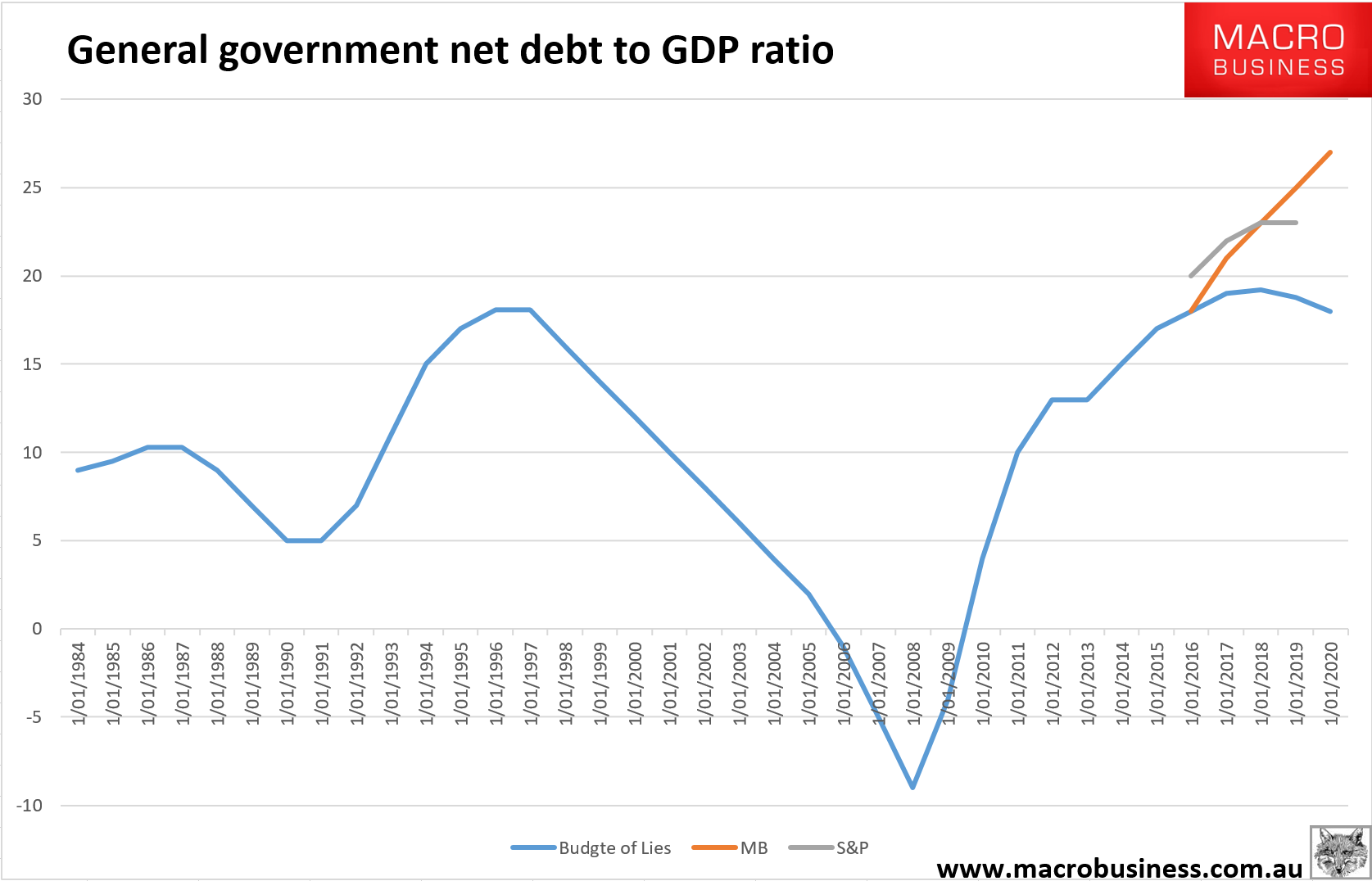

Put those two things together then MB gets a much steeper outlook for government debt to GDP than does S&P:

So, the downgrade will definitely come and not just one. None of this includes the impact of any new global shock which is also assuredly coming.

Advertisement

After markets closed yesterday, S&P also put the banks of negative watch:

We are therefore taking similar action on the four major Australian banks–Australia and New Zealand Banking Group Ltd., Commonwealth Bank of Australia, National Australia Bank Ltd., and Westpac Banking Corp.–and a range of strategically important subsidiaries of these banking groups.

The negative outlooks on these banks reflect our view that the ratings benefit from government support and that we would expect to downgrade these entities if we lower the long-term local currency sovereign credit rating on Australia. We are also affirming the issuer credit ratings on these banks and their strategically important subsidiaries that benefit from government support.

The stable outlooks on Macquarie Bank Ltd. and Cuscal Ltd. are unaffected by the sovereign action.

We are keeping UDC Finance Ltd. and National Wealth Management Holdings Ltd. on CreditWatch with negative implications. Both are subsidiaries we have previously identified as being subject to structural or ownership changes.

We have not changed our view of the stand-alone credit profiles of the Australian major banks or their rated group subsidiaries or our view of the unsupported group credit profile of these banking groups.

At the same time, we revised the outlooks to negative from stable on a range of strategically important entities of these banking groups (see ratings list below). The outlooks on Macquarie Bank Ltd. (A/Stable/A-1) and Cuscal Ltd. (A+/Stable/A-1) are unaffected by the outlook change on Australia. Although ratings on these entities also benefit from government support, a one-notch downgrade of the local-currency sovereign rating would not in our opinion significantly reduce the government’s ability to support these entities at their current rating levels.

We would expect to lower the ratings on affected entities if we downgrade the long-term local currency sovereign credit rating on Australia to ‘AA+’ from ‘AAA’ and our view of the stand-alone credit profile of these entities remains unchanged. In this scenario, we would expect to lower our issuer credit ratings on the Australian major banks–and senior debt issued by these banks–by one notch to ‘A+/A-1’ from ‘AA-/A-1+’, and keep our ratings on hybrid and subordinated debt issued by these banks unchanged because these ratings do not incorporate any uplift from government support.

We could revise the outlook on these entities back to stable if we revise the outlook on Australia’s ‘AAA’ local currency sovereign credit rating back to stable. Downward pressure on the ratings on the Australian major banks, Macquarie Bank Ltd., and Cuscal Ltd. could also emerge independently of any rating action on the sovereign if, in our opinion, there is a reduced tendency for the government to support systemically important banks due to changes in the resolution framework or from other factors.

To sum up, this is not an immediate disaster but it illustrates that:

Advertisement

Australia’s growth model is broken. It cannot expand without more offshore debt, that simple;

the economy is now so government dependent – owing to the long term hollowing out of everything non mining and non banking – that it is an embarrassment;

austerity won’t fix the deficit unless it addresses this structural deficiency. Cuts to government spending must shift the pattern of growth in the economy as well or they will simply slow growth and blow back as lower revenues. This reform must boost tradables over consumption and means lower housing subsidies, lower super subsidies and productivity reform in all guises;

we’ll all no doubt draw comfort from a muted market response but that is because we’re in the midst of the greatest single central bank engineered global chase for yield in 500 years, and

the fallout will come but not until that reverses in the next shock.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.