Despite the recent slowdown, housing finance data highlights that investor activity in the housing market is starting to rise again and when you look at total returns from housing it’s no surprise…

The CoreLogic RP Data Accumulation Index which has been published since June 2009 highlights the total returns from residential property. The total returns include both the increase in values as well as gross rental returns…

Over the 12 months to May 2016, combined capital city home values have increased by 10.0% while total returns have been recorded at a higher 13.9%. Looking at the individual capital cities, all cities except for Perth have recorded positive total returns over the past year…

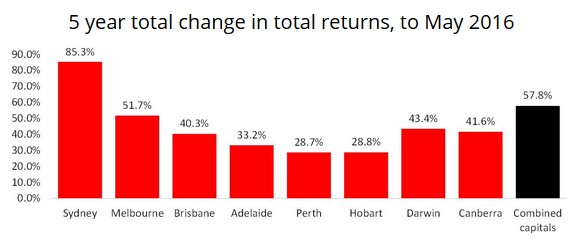

The third chart highlights the total returns over the past five years across all capital cities. Again, Sydney in particular, has seen far superior total returns compared to all other capital cities…

This data… highlights why housing investment has been so popular. In a low interest rate and subsequently low return environment housing has, over recent years, offered attractive returns. Whether this continues to be the case remains to be seen.

One wonders why RP Data ignores the cost of borrowing when compiling its total returns data? After all, virtually everyone borrows to invest in housing, so why on earth would you count the yield without then netting-off the outgoings (particularly the mortgage)?

Advertisement

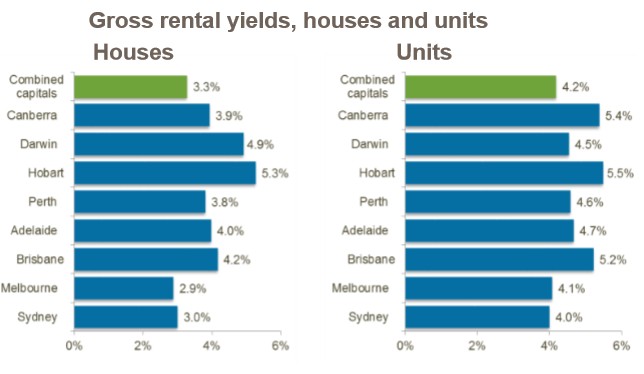

Indeed, RP Data’s latest rental data revealed that gross rental yields nationally have fallen to a record low of just 3.3% for houses and 4.2% for units (see below), which is well below the discount investor mortgage rate of 4.90%, according to the RBA. Add in other costs of ownership (e.g. rates, maintenance, body corporate, and agents’ management fees) and the income equation worsens.

Hence, most new housing investors are running a negative carry trade and are effectively paying their investment home a dividend in the hope that it repays them with capital growth.

Advertisement

The typical Australian housing investors is, therefore, speculating on continued capital growth, which is the very definition of ponzi-financing.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.