From Domainfax:

After banks put the brakes on lending to property investors in 2015, several are now easing off the pressure and trying to spur on more borrowing among buyers who drove the recent housing boom.

Westpac, the country’s biggest lender to landlords, this week began allowing customers to include the tax benefits from negative gearing in their loan assessments, unwinding changes made last year, and last month it started accepting smaller deposits from investors.

Bank of Queensland last month raised its maximum loan to valuation ratio (LVR) for investors to 90 per cent, from 80 per cent, a change that allows investors to have smaller deposits.

Australia’s biggest credit union, CUA, also lifted its maximum LVR to 85 per cent, from 70 per cent.

Other banks are using the other big “lever” at their disposal to ramp up growth – price.

Lenders including Bankwest, ME and UBank have cut three-year fixed rates for investors below 4 per cent, and brokers say lenders including Commonwealth Bank are prepared to offer discounts of up to 1.5 per cent off their advertised interest rates.

…AMP Capital chief economist Shane Oliver said APRA’s 10 per cent cap appeared “quite excessive in the scheme of things” when compared with the much slower growth in household incomes.

…When there are also fears of an apartment glut in some inner-city areas, Dr Oliver said the prospect of looser credit standards and stronger growth in housing investor debt amplified the potential for serious problems to emerge, if there was a slump in house prices.

“The higher prices are when that occurs, then the greater the risk is of a sharp destabilising fall,” he said.

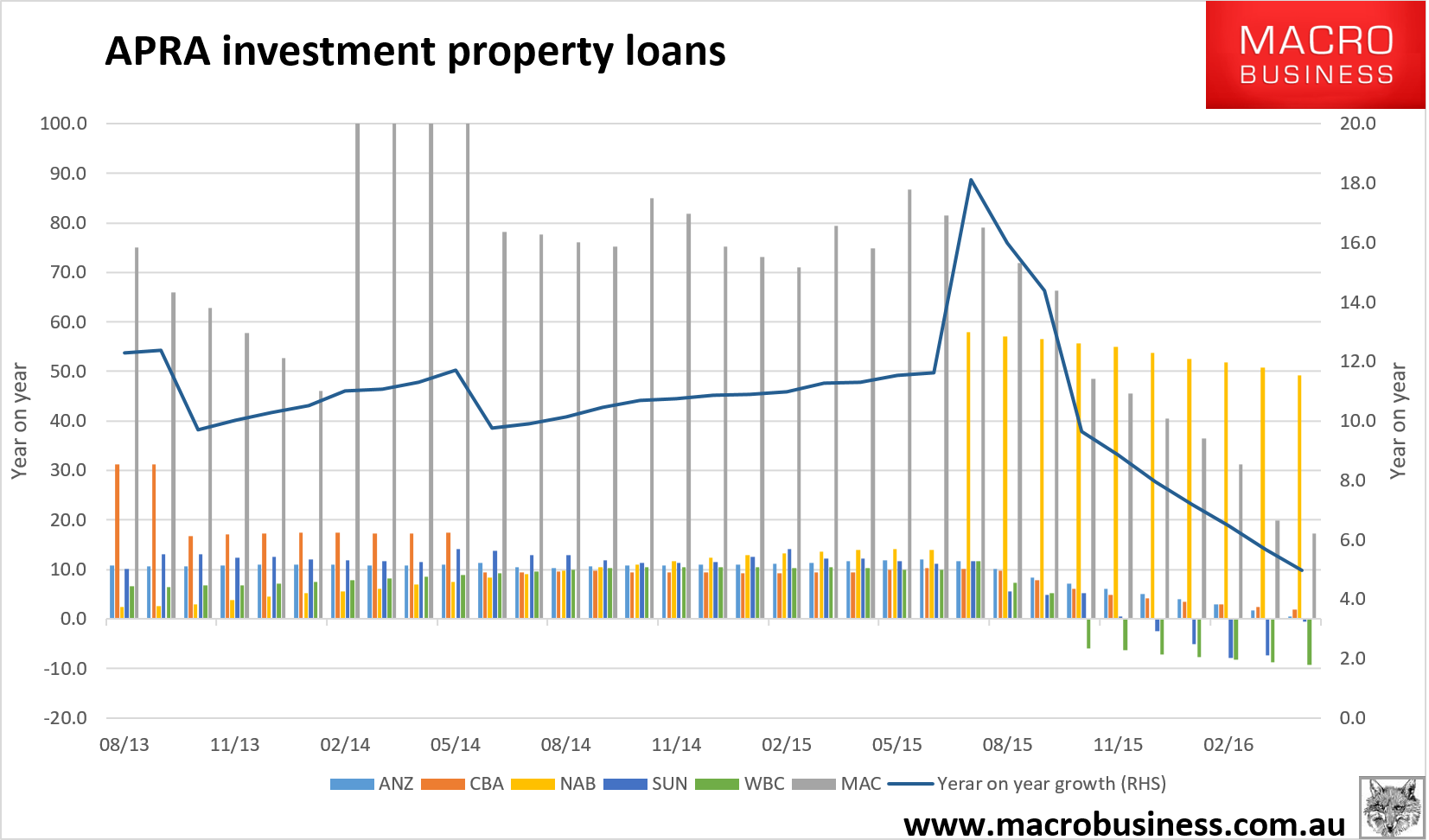

It’s clear that house prices are firm with investor lending growth at 5% for major banks on APRA data:

As Dr Oliver says, the last thing the economy needs right now is re-acceleration in the investor bubble which will respook the RBA. When our Shane tells you you’re too loose then you know you’re on the flaccid side of slack. With incomes going backwards and nominal GDP at 2%, property speculator credit growth at 10% is the definition of imprudent.

This is made all the more urgent by the shift down in the US economy registered in Friday night’s data. The RBA is going to see more and more pressure to cut as the Australian dollar remains too high and adds tradable disinflation to non-tradable.

There is an argument for APRA to wait until after the election given a Labor win and the prospect of negative gearing reform will work as a fiscal headwind to specufestor demand but that is the only impediment to tightening macroprudentially again and, frankly, the gap between income and credit growth is so big it’s time to move anyway.

APRA must immediately move to protect the gains it has already made and lower its investor lending cap to 5% or lower year on year growth.