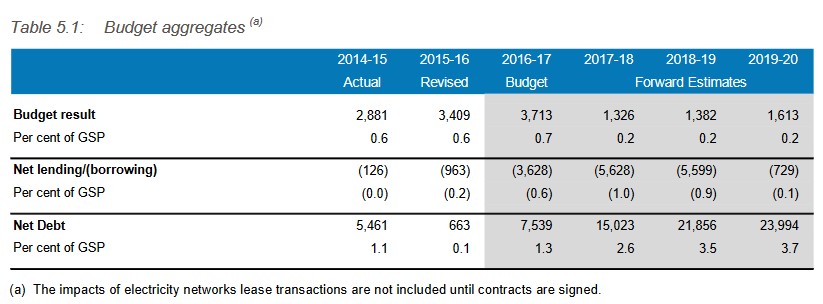

The NSW Budget for 2016-17 has been released, and as expected, it revealed a big Budget surplus of $3.7 billion, with smaller surpluses expected over the forward estimates:

The expected budget result in 2015-16 is a $3.4 billion surplus. The improvement in 2015-16 reflects stronger revenue than estimated at the time of the 2015-16 Budget, but is comparable with the forecast at the time of the 2015-16 Half-Yearly Review. In 2016-17 a slightly higher surplus of $3.7 billion is expected.

Surpluses averaging $2.0 billion are expected across the budget and forward estimates years. These more modest surpluses reflect slower revenue growth due to moderating transfer duty receipts and lower growth in GST revenue.

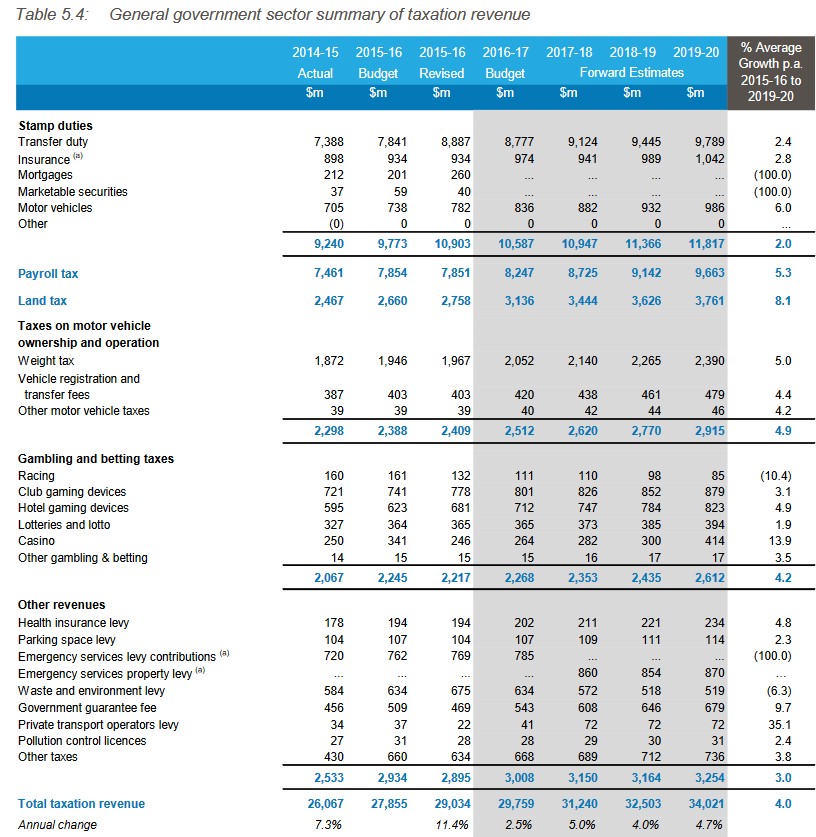

The most dubious part of the Budget’s forecasts, in my opinion, relate to the stamp duty projections. As shown in the next table, stamp duty receipts are projected to grow by 2.4% per annum over the forward estimates:

Advertisement

While around 80% ($835 million) of this projected growth relates to the 4% surcharge on foreign property purchases, there is reason to believe that the NSW Government is being overly optimistic in its stamp duty projections.

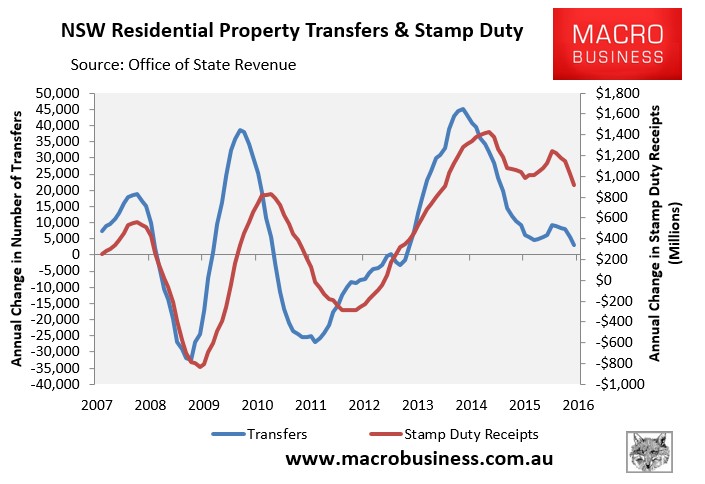

Blind Freddy can see that the Sydney housing market is at the tail end of an epic boom that has seen the city’s median house price climb to around $1 million. In all likelihood it will experience a correction in prices and transaction volumes over the forward estimates, hitting stamp duty receipts hard.

Indeed, the below chart shows just how volatile NSW stamp duty receipts are, and suggests they are nearing a correction:

Advertisement

The post-GFC correction in stamp duty receipts in NSW saw a peak-to-trough decline of around 30%. However, given the unprecedented size of this boom, the NSW Government should expect a much bigger correction in receipts next time around – most likely over the forward estimates.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.