Against the backdrop of lower rates and tighter regulation of home loans, we believe additional re-pricing is likely with potential for differentiated pricing on different types of home loans. We think future cuts in the RBA cash rate would provide banks with the opportunity to re-price and our Economics team recently called for three additional rate cuts to a trough level of 1.00%. We currently forecast an additional 10bp of re-pricing on owner-occupier loans (OOL) and 20bp on investor property loans (IPL). Further, we think banks are likely to consider further price differentiation for investor property loans, interest-only loans and offset accounts.

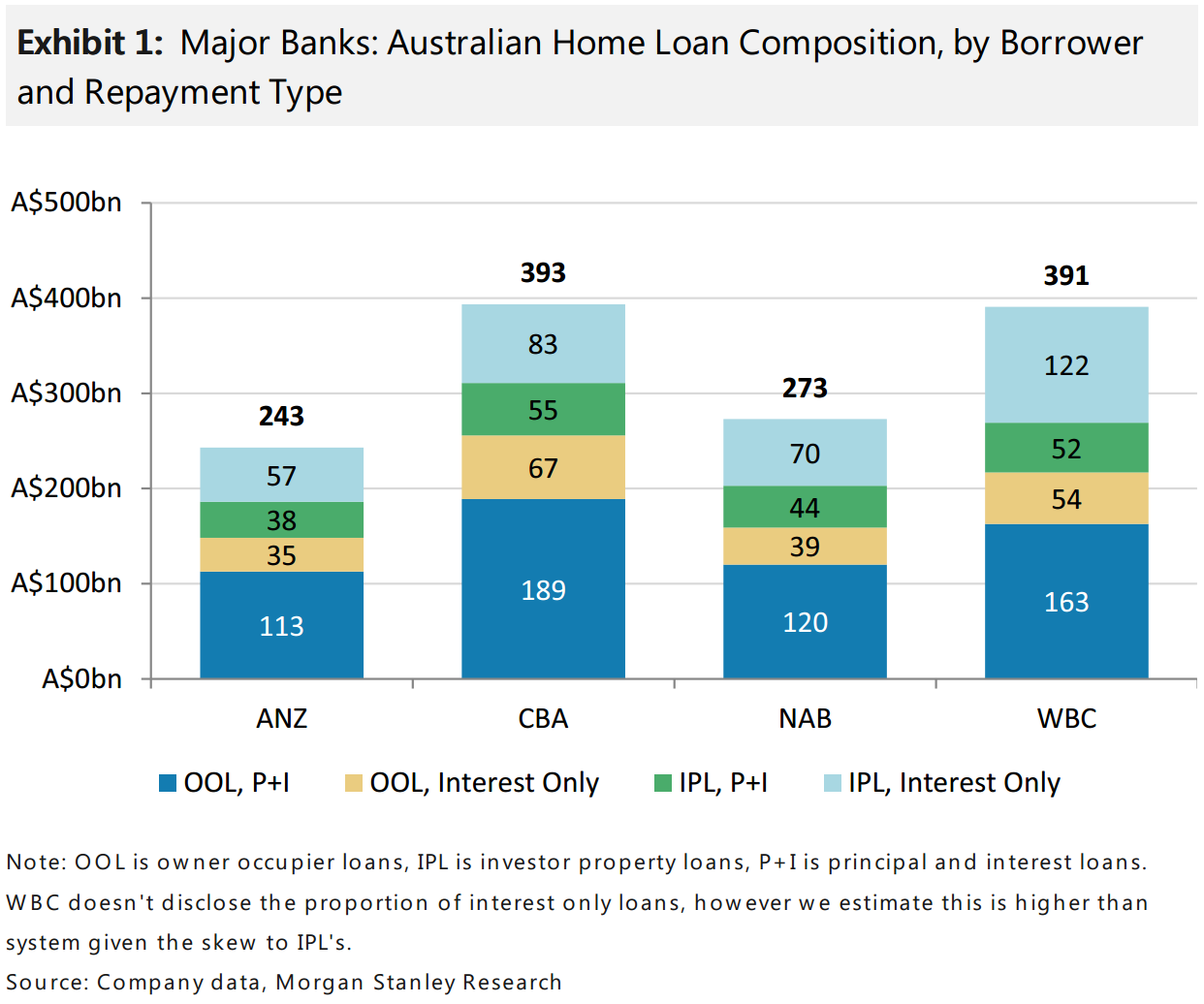

Our Chart of the Week shows the composition of the major banks’ Australian housing loans.We note the following: (1) ~39% of all Australian housing loans are interest-only; (2) NAB discloses that ~61% of IPL’s and ~25% of OOL’s are interest only, while ~35% of its interest only loans are to OOL; (3) We estimate that 10bp of interest-only loan repricing has the biggest benefit at WBC (+1.5% profit benefit), and the least at ANZ (<1% profit benefit); (4) OOL repricing has a broadly similar impact on cash profit across the major banks, with 10bp of re-pricing providing a ~1.3% benefit; (5) WBC and NAB are most leveraged to IPL re-pricing with 10bp adding ~1.4% and ~1.2% to cash profit, respectively.

That strikes me as very conservative thinking. I expect banks to hold back many more bps than that. The last cut was repriced via deposits, from Banking Day:

A number of authorised deposit-taking institutions have cashed in on last month’s cash rate reduction by cutting their savings account rates by a greater margin than their variable mortgage interest rate cuts.

According to the latest Mozo Banking Roundup, 19 authorised deposit-taking institutions looked to boost their margins by hitting depositors hard.

Among the big banks, ANZ cut its variable home loan rate by 19 basis points and cut its Online Saver rate by 25 bps. Commonwealth Bank cut its variable home loan rate by 25 bps and cut its NetBank Saver rate by 30 bps.

CBA was not the only deposit-taker to cut savings account rates by 30 bps over the past month. Others included G&C Mutual Bank, Illawarra Credit Union, and QPCU.

The institution with the most striking disparity in rate movements was ME, which cut its variable home loan rate by five bps and cuts its Online Savings Account rate by 25 bps.

G&C Mutual Bank wasn’t far behind, cutting its variable home loan rate by 12 bps and its savings account rate by 30 bps.

Bonus rates came in for some heavy treatment. ING Direct cut the bonus rate on Savings Maximiser by 50 bps, G&C Mutual Bank cut the bonus rate on its Bonus Saver account by 44 bps and Illawarra Credit Union cut the bonus rate on its Saver account by 40 bps. Commonwealth Bank cut its GoalSaver bonus rate by 35 bps.

Some institutions were kinder to their depositors. Citibank cut its variable home loan ate by 21 bps but only cut its Online Saver rate by 15 bps.

However, the overseas experience is that below 2% it becomes hard to cut deposit rates, from Goldman:

Advertisement

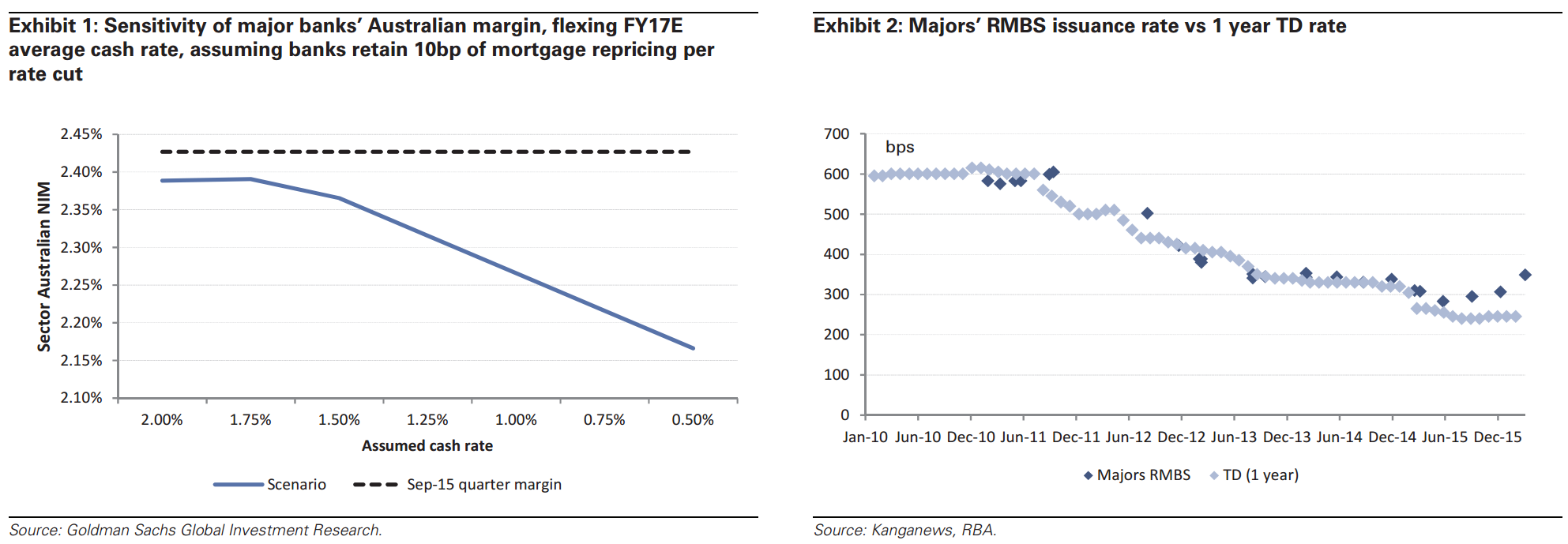

Our macro team has recently reinstated their view that the Reserve Bank of Australia (RBA) will cut cash rates two more times in CY16 (Australia and New Zealand Economics Analyst: Forecast Change: Why the RBA will cut again, February 18, 2016). In this piece we undertake a detailed, bottom-up assessment of the extent to which margins are at risk as cash rates fall, extending on the work we first published in March 2015 (Assessing the rate cut risk to banking net interest margins; prefer ANZ (CL-Buy), March 27, 2015).

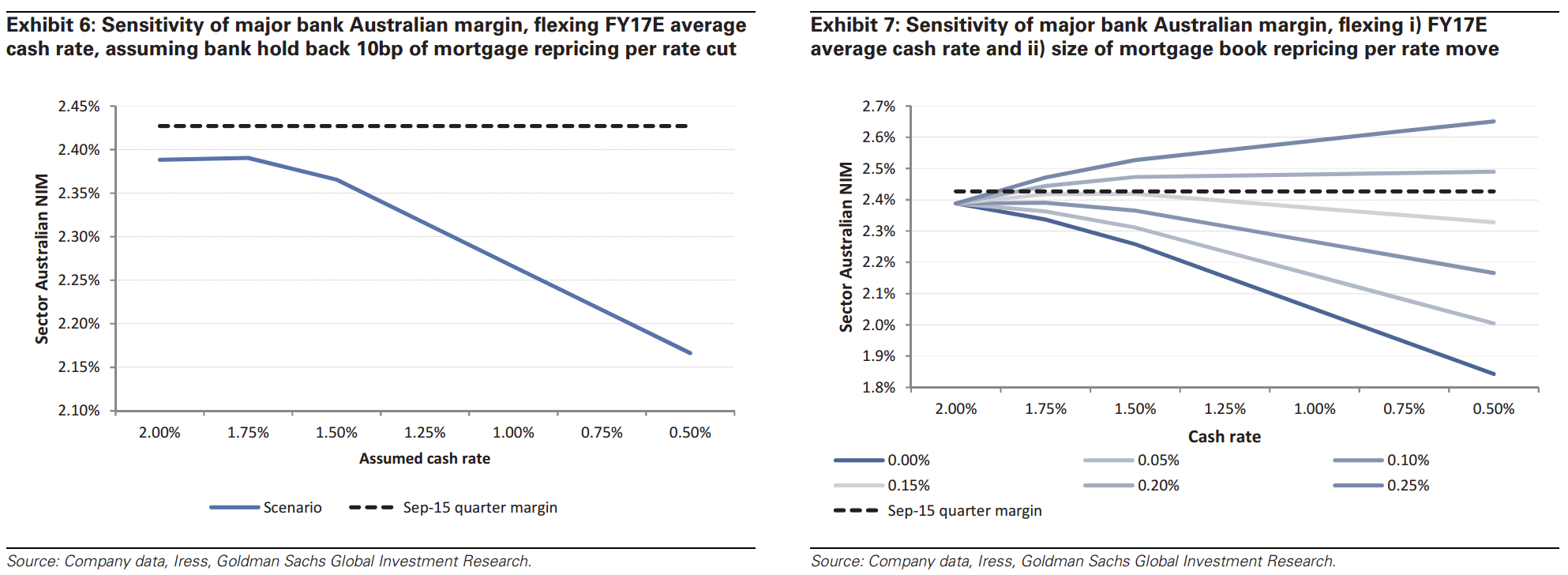

We conclude that even if cash rates remain unchanged at 2.00%, margins will fall by about 4 bp versus the Sep-15 quarterly margin (previous GSe -2bp), driven by the grind lower of the replicating portfolio and higher wholesale funding costs, partially offset by the mortgage book repricing that has been announced by the banks since 4Q15. Beyond that, if we assume the major banks hold onto 10bp of mortgage repricing per rate cut then: x if cash rates fall 25bp to 1.75%, we estimate this will have no meaningful impact on margins; or x if cash rates fall 50bp to 1.50%, then margins will fall by a further 2bp, equating to a cumulative 6 bp reduction in margins versus the Sep-15 quarterly margin (Exhibit 1; versus previous GSe -2bp, therefore refer to earnings changes below).

However, if the cash rate was to fall below 1.50%, every additional rate cut thereafter would shave about 5 bp off sector margins. The sensitivity of margins to falling rates accelerates once the cash rate falls below 1.50% because the various levers the banks have at their disposal become less flexible as the cash rate approaches zero and we would particularly highlight the following:

1. Our expectation is that term deposit (and cash management to a lesser degree) pricing will become quite sticky as the cash rate falls below 2.0%, as was the experience in the both the United Kingdom and Canada in 2008/09. This will particularly be the case as the domestic banking regulator, APRA, shifts its focus in 2016 towards the Net Stable Funding Ratio (NSFR), which is likely to place pressure on the banks to both term out and improve the quality of their funding (i.e. preference for deposits over wholesale). Furthermore, we note that the recent move out in funding costs has historically correlated with higher rates being paid by the banks on deposits (Exhibit 2).

2. We estimate that the replicating portfolio represents about a 5bp p.a. margin headwind for the banks over the next 2-3 years.

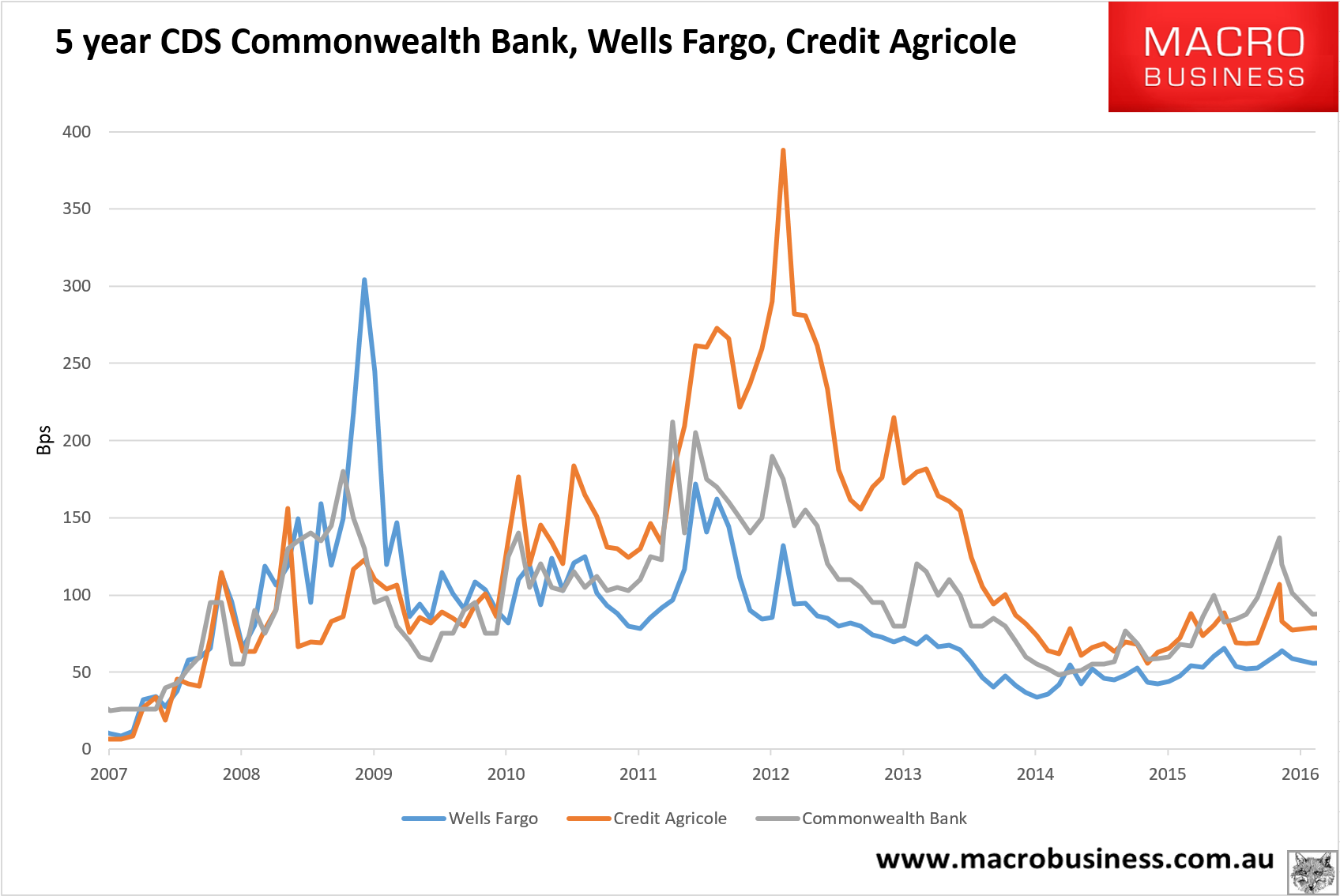

Especially if you’re wholesale funding costs are rising. Despite a recent reprieve that had CBA CDS at 88.5 bps yesterday:

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.