From The Age:

Independent economist Saul Eslake, the Grattan Institute’s John Daley and Industry Super’s Stephen Anthony all said Labor’s decision had increased the risk that Australia’s credit rating could be knocked down a notch by international ratings agencies, which would potentially drive up borrowing costs for federal and state governments and hurt the economy.

And they have called on both sides of politics to exercise greater spending restraint and pursue more ambitious budget repair.

The decision to run bigger deficits in the next four years if Labor wins the July 2 election was announced by Mr Shorten and shadow treasurer Chris Bowen on Wednesday and comes despite the federal opposition’s recent warnings about Australia’s credit ratings.

…Asked to assess this decision by Labor on Wednesday, Mr Eslake said that, “given that Mr Bowen has expressed concern, rightly, that Australia is at risk of losing its AAA rating, it hardly seems sensible for a would-be Labor government to tolerate a significantly greater budget deficit over the next four years”.

…Mr Daley said that “yes, they have placed the AAA rating at risk” because ratings agencies would see that successive governments and oppositions of all persuasions were again delaying tough budget decisions.

…Treasurer Scott Morrison said on Wednesday that the opposition had ” basically given up on the budget task”.

…”I can assure you the ratings agencies will be looking at what their costings and what their funding, if they were to be in government, over four years and how they plan to do that.”

It’s true. Labor appears to have given up on the AAA rating. And, yes, that’s not very good.

But let’s face it, what choice have they? They’re working from Treasurer’s Budget that has already lost the AAA, as Treasury itself basically confessed:

The medium-term economic and fiscal projections are sensitive to the assumptions that underpin Treasury’s estimate of potential GDP — that is, assumptions about population, productivity and participation. They are also sensitive to the assumed pace of the economy’s return to potential — that is, the assumption that the adjustment period lasts five years.

Analysis reported in the 2016-17 Budget shows that a faster (two year) adjustment to potential requires comparatively faster growth in real GDP and employment as the output gap closes and spare labour is put to use. This leads to lower unemployment and faster growth in wages and domestic prices, increasing nominal GDP and improving the projected underlying cash balance over the medium term even as long-run real GDP is unchanged from the Budget projections. A more gradual adjustment period (eight years) is estimated to have broadly opposite effects on the projections.

Analysis in the 2016-17 Budget also shows that lower trend productivity growth than assumed in the Budget projections would directly reduce potential growth — leading to permanently lower real GDP and wages with only a small impact on prices. In this scenario, lower nominal GDP leads to lower projected tax receipts which weakens the projected underlying cash balance over the medium term. By contrast, assuming faster trend productivity growth than assumed in the Budget projections results in higher nominal GDP and tax receipts, strengthening the underlying cash balance.

…The medium-term projections show that, without considerable effort to reduce spending growth, it will not be possible to run underlying cash surpluses, say in the order of one per cent of GDP, without tax receipts rising above 23.9 per cent of GDP. Even if payments were reduced from the levels projected at the 2016-17 Budget to the long-term average of 24.9 per cent of GDP by the end of the medium term, tax receipts would still need to rise to around 24.2 per cent of GDP by 2026-27, well above the average of the past 30 years, to achieve a surplus of one per cent of GDP. Reducing spending growth has proved difficult in practice.

…Australia has a relatively strong fiscal position by international standards. However, Commonwealth Government debt levels are projected to reach recent historical highs, both on a gross and net basis. These debt levels are not an immediate concern given historically low interest rates and a growing economy. But should Australia experience a significant negative economic shock or increased interest rates or debt levels rise above current projections over the medium term, the debt burden will impose an increasingly significant cost on the fiscal and economic outlook. It is crucial for Australia to maintain its top credit rating to ensure the Commonwealth’s borrowing costs, and those across the economy more generally, are kept as low as possible.

The RBA agreed:

Plans to balance Australia’s federal budget by around 2021 are implausible, says Reserve Bank policymaker and economist John Edwards, adding that the nation risks losing its prized AAA credit-rating status.

Mr Edwards said the plan outlined by Treasurer Scott Morrison in the government’s 2016-17 budget to bring the budget back into balance by 2021 was too slow as it relies on rising income tax collections to be achieved.

“I don’t think we can disregard the possibility that the ratings agencies will lose patience with a fiscal trajectory which is simply not plausible, relying as it does on increased personal tax collections,” Mr Edwards, a Reserve Bank of Australia board member, said in an interview with The Wall Street Journal.

If Australia lost its AAA rating, it would be a “big deal,” he added.

“Given that we have higher foreign liabilities than similar rated countries, and given that debt as a share of GDP is rising more rapidly than many other highly rated countries, there is always a risk we are going to be kicked out of the (AAA) club,” he said.

Mr Edwards said a return to budget balance over the next two years would be a smarter idea, saying the government has favored tax cuts for corporations over the mounting task of lowering the budget deficit, which would protect the economy against shocks.

Moody’s did too:

“The projected increase in revenues as a share of GDP is based on a return to robust nominal GDP growth which generally comes with a higher revenue-intensity of growth. Our forecast for nominal GDP growth is somewhat more muted than the government’s. We estimate that the adjustment to an environment of lower commodity prices is still underway and will continue to weigh on corporate profitability and wage growth. As a result, improvements in the government’s revenues may be somewhat more muted than currently budgeted.

Even PM Turnbull knows it:

The reality is that forecasts – there are always risks with forecasts. I think everyone understand that. The further out you go, the more speculative those assumptions are. Let’s go back 10 years. 10 years ago, 2006, there wasn’t an iPhone. People didn’t have smartphones. Facebook was 1-year-old. It was a different world. A very very different world. It’s a long list. You can think of all the differences yourselves. Ten years hence is a long way out and that is why in the Budget we set out four years, that’s why we have a 4-year forward estimate, and we recognise that there are risks associated with that.

What will the iron ore price be? What will the foreign exchange rate be? What will be happening in the Chinese economy? What will be happening in Europe? These are all risks. Let’s not kid ourselves. There are plenty of economic risks on the horizon particularly in the global economy.

Scott Morrison’s Budget outlook is pure fantasy yet it forms the underpinning for both party’s election costings in the Pre-Election Fiscal Outlook (PEFO).

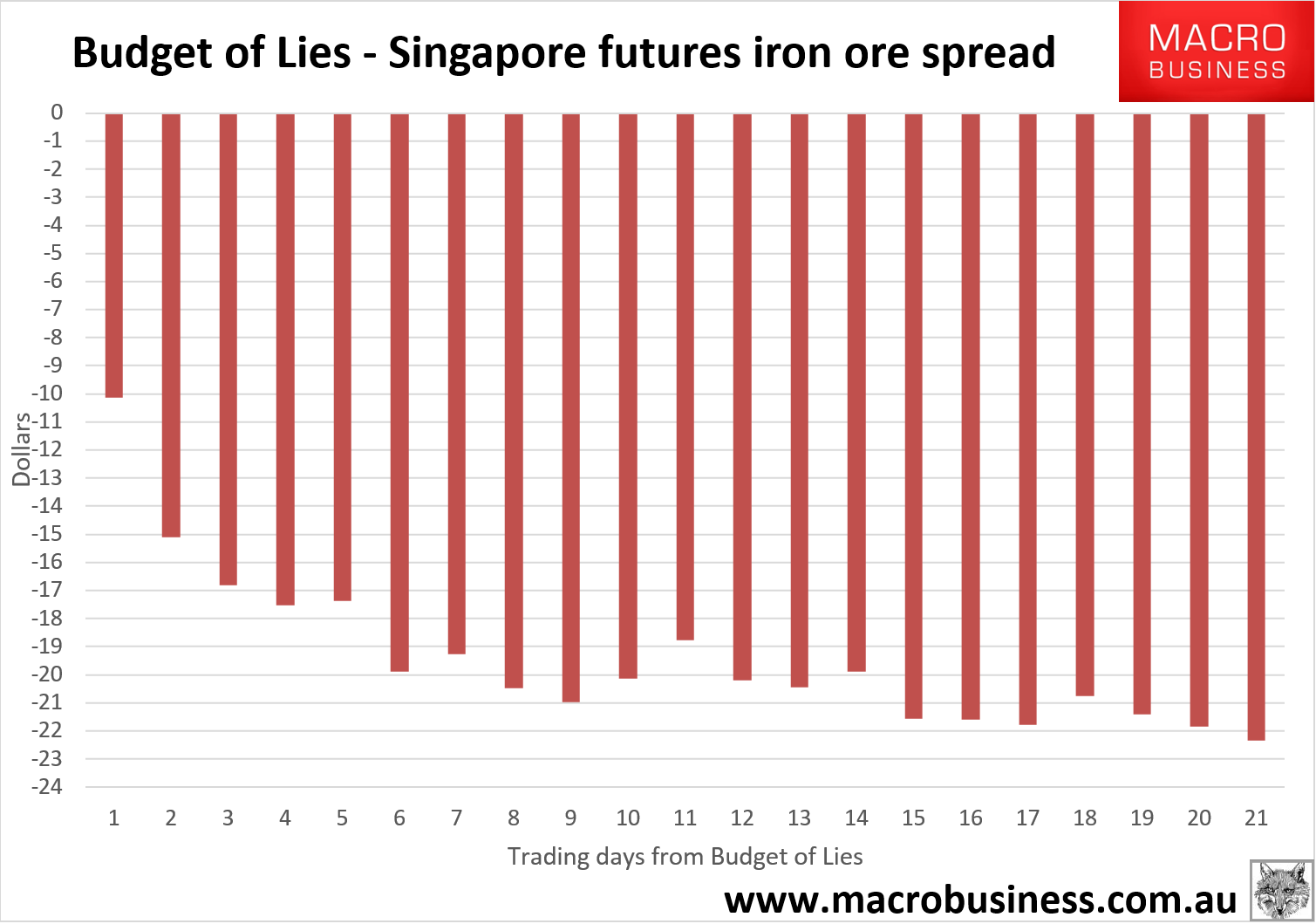

So why would Labor pledge to keep it now? They’ll fail simply because the economy can’t take the tightening required, revenue will drop and the deficit widen anyway, then they’ll get blamed for losing the rating. Even if they win government it makes much more political sense to let Scott Morrison’s absurd forecasts take the blame. It is his PEFO of Lies after all, as iron ore futures are still pricing -$20 on the Budget outlook:

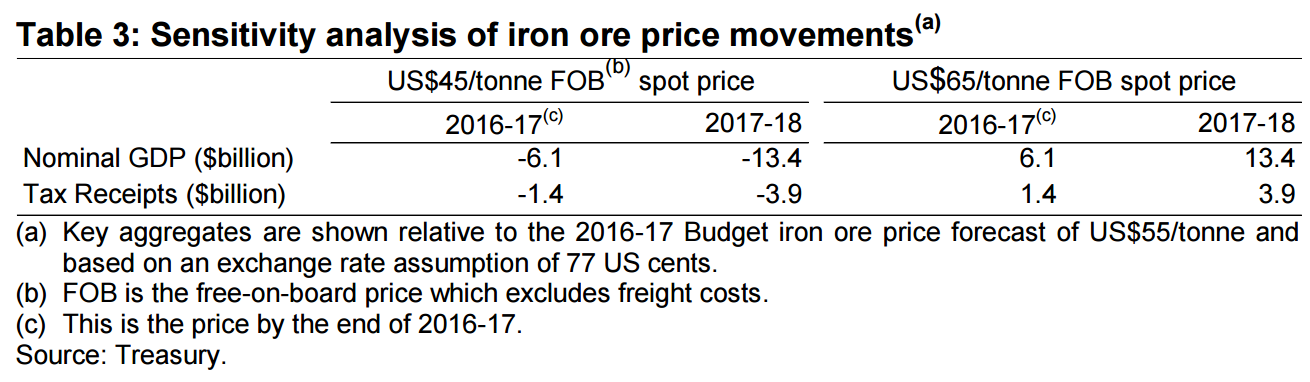

The 2016/17 Budget of Lies is behind by roughly -$20 per tonne, a full 40% drop on the Treasurer’s fantasy outlook. Taking the most reliable futures market in Singapore, on iron ore alone the Budget is currently mis-pricing nominal GDP by some $25 billion and tax receipts by $8 billion per annum.

But that is only the beginning. Other assumptions are just as bad:

- dwelling investment to grow 2% when we already know it has peaked in ABS data;

- business investment is expected to fall -5% when hard ABS data is already measuring it at -14%;

- wages and demand growth based on 1.6% productivity gains and 2.5% wages growth when the current trend is sharp falls and 1.6% wages growth in the last quarter (and still falling);

- nominal growth is supposed to be 4.25% but when you add the right outlook it falls to 2.5%, the same as this year, at best.

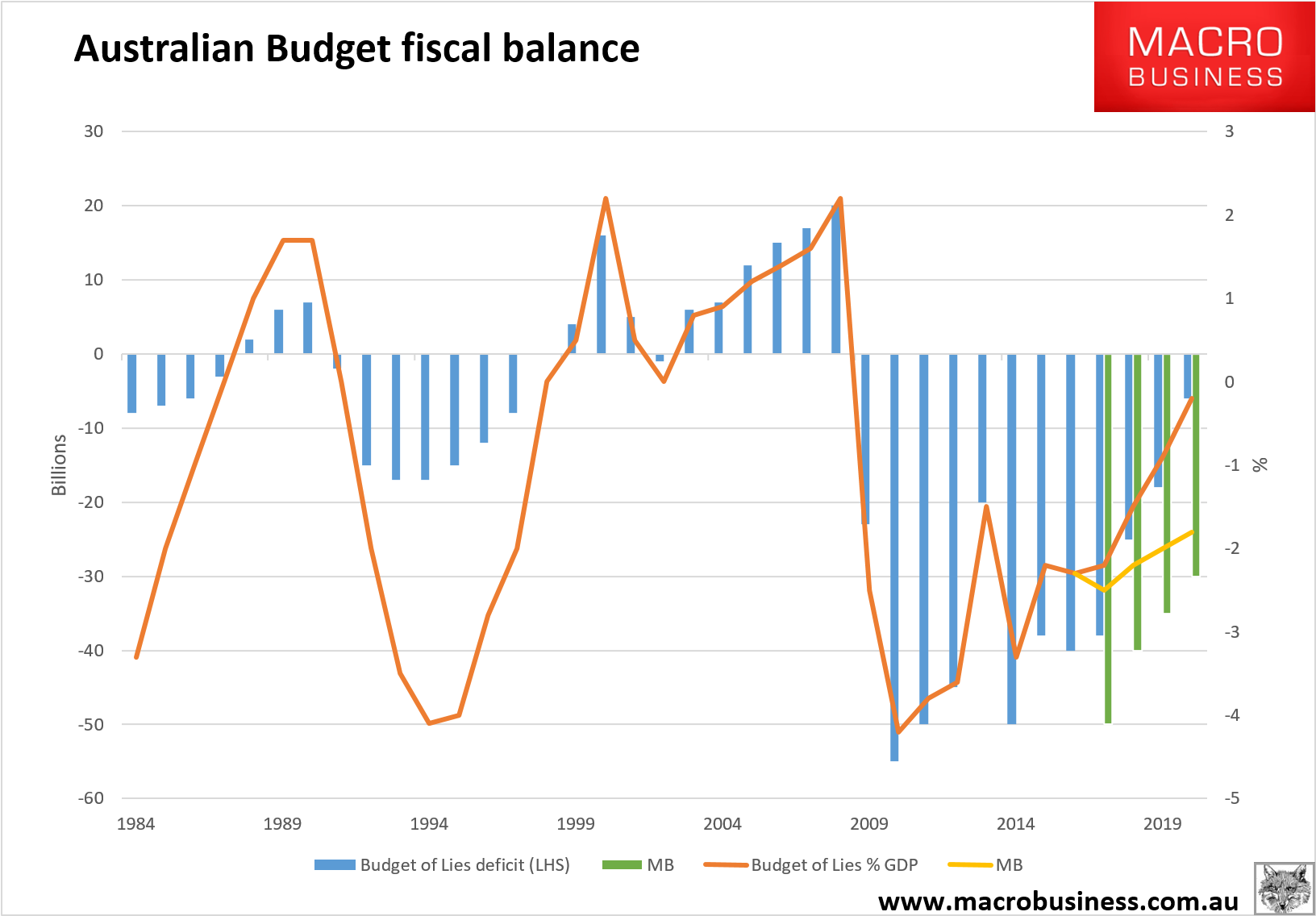

So, the deficit reduction outlook is also a lie. Here’s what the chart looks like when you apply realistic assumptions:

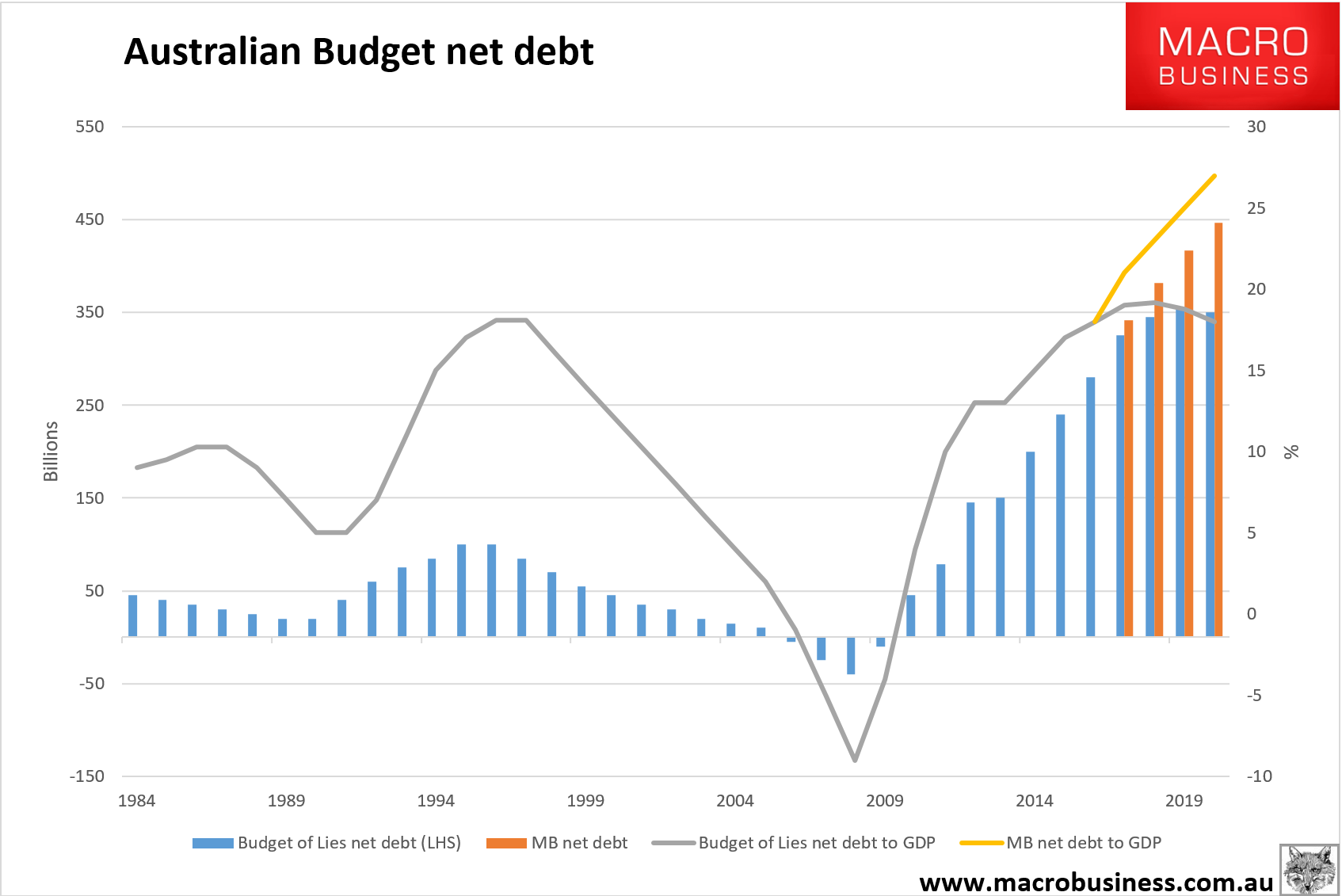

And the net debt outlook as well with realistic assumptions:

It’s a long line of Treasurer’s that have failed to reform the Budget to preserve the sovereign rating but none is more cynical than Scott Morrison and his surplus of hypocrisy.