In our view, lower cash rates should provide some support to bank share prices in the near term. However, we retain our negative stance, as RBA rate cuts create additional margin headwinds forFY17 and highlight the reasons for our caution on credit quality.

Lower cash rates: Our Macro colleagues, Chris Nicol and Daniel Blake,expect the RBA to lower the cash rateto 1.00% in 2017 to address weak growth and disinflation (refer Australian Transition: Asia Insight: Scoring a Difficult Transition; Cutting RBA Trough Rate to 1% ). They highlight the slowdown in housing activity, the capex cycle and fiscal policy as headwinds for the Australian economy.

More near-term focus on the dividend yield: While ANZ has cut its dividend, the other majors are determined to hold theirs despite elevated payout ratios. With 2016 dividend risk reduced and cash rates heading lower, an average major bank dividend yield of ~6.5% should provide some support for share prices in th elead-up to the August 2016 reporting season.

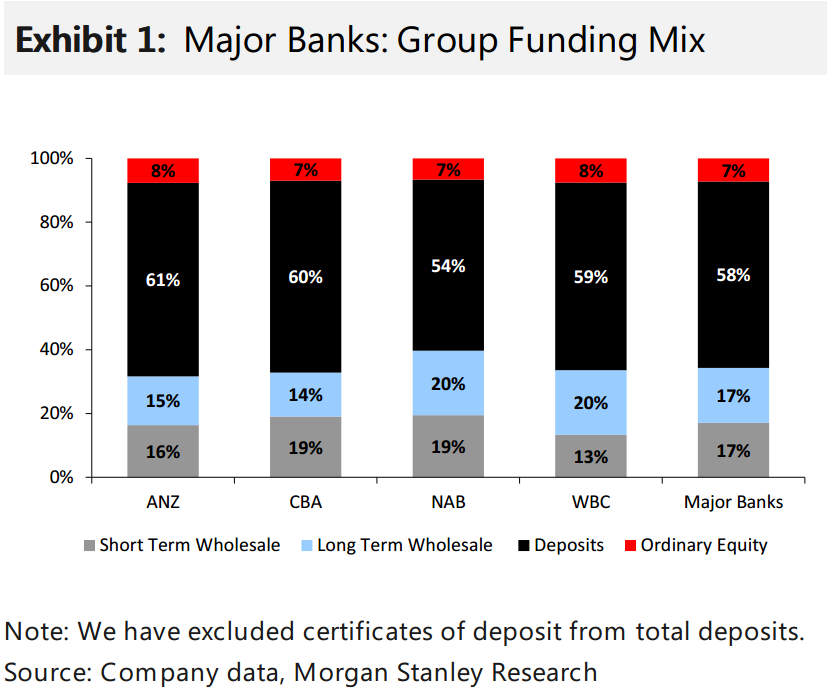

Downside risk to margins in FY17E: We already see margin headwinds from competition and changes to funding requirements. In addition, our analysis highlights that up to ~15% of the majors’ Australian funding can not be priced lower. All else equal, we estimatethat every 25bp cut in the cash rate reduces major banks’ margins by 2-3bp and earnings by 1.5-2.0%.

Implications for mortgage pricing: Our forecasts already assum ea further 10bp of repricing on OOLs and 20bp on IPLs after the Federal Election in order to ensure flattish margins in FY17E. If the RBA cuts rates to 1.00%, the need for additional home loan repricing will become more pressing.While we believe the majors retain sufficient oligopoly power to do this (so our margin forecasts are unchanged), the political environment and customer implications put more onus on the banks to introduce differentiated pricing (refer CotW: Differentiation in Hom Loan Repricing). All else being equal, the majors need to reprice SVRs by an average of ~8bp to offset the impact of a 25bp rate cut.

Good or bad for the loan-loss outlook? At first glance, lower rates would appear to reduce th erisk of higher loan losses, as they support the cash flow / consumer spending of indebted households and reduce the interest burden on stressed businesses. However, the potential for another 75bp of rate cuts highlights the weak income and investment trends in the economy. With the banks describing credit quality as “sound”and consensus assuming that loan losses are flat next year, we still see risk of earnings downgrades and dividend cuts in a challenging economic environment.

Modest loan growth: Rates have already fallen 300bp since 2011, so we doubt that further cuts area catalyst for materially stronger loan growth.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.