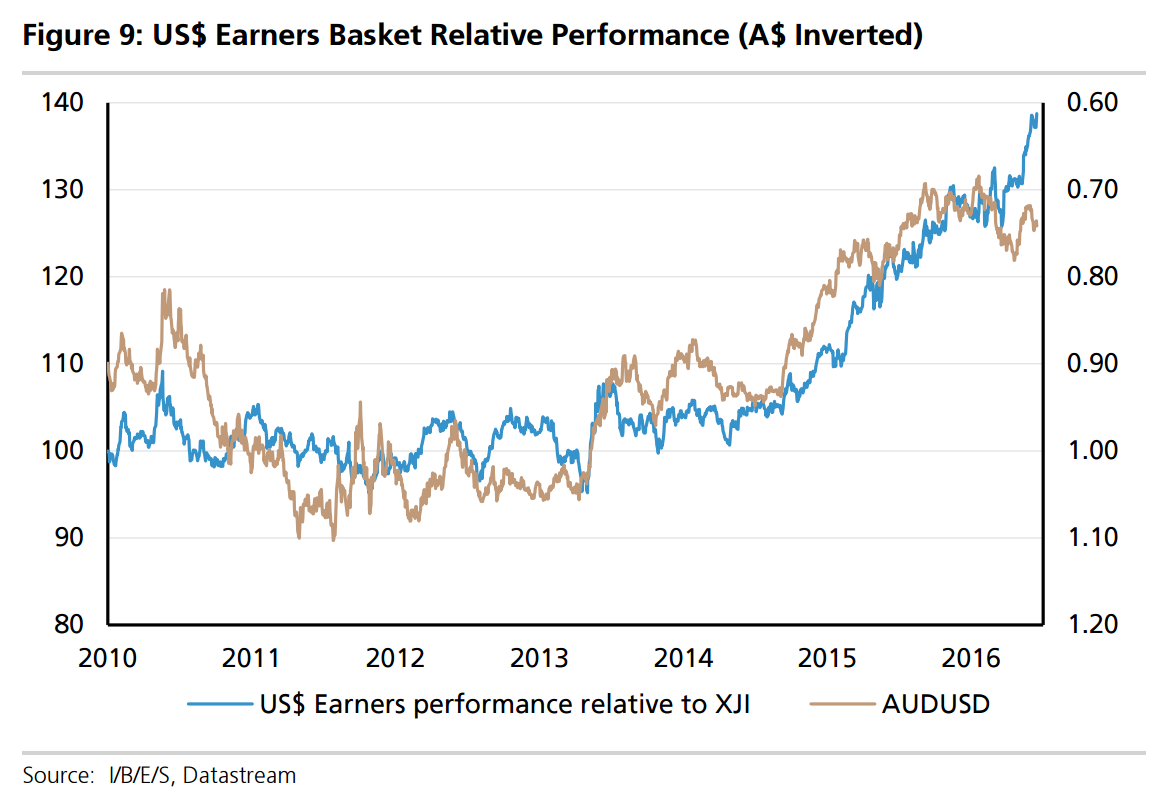

Foreign currency earners have continued to do reasonably well even as the A$ has rallied. This may be a function of the perceived quality and defensive growth characteristics of many stocks in this basket but it does seem a relatively fully priced and well held trade in a number of instance, despite our view that the A$ has downside. We a still believe the A$ has a downside skew based on a number of potential factors: 1) the Fed resuming its tightening cycle 2) the RBA instigating another cut and 3) some further weakness in the iron ore price. We still see some value in some of the higher beta or more cyclical exposures (Incitec Pivot, Macquarie Group, QBE Insurance Group) but this obviously needs to be calibrated against the current near-term risk backdrop. Our favoured defensive exposures are Resmed (new addition) and Aristocrat Leisure. We have trimmed CSL but retain a moderate overweight position.

Readers will recall this way my favourite allocation from 2012 onwards (a great way to play the falling AUD). Mid last year I began to see this as a “sell the rallies” trade not because I expected the AUD to rise but because I reckoned that global shares were close to peaking and falling as the Fed tightened. It was roughly the same time that I switched to buying gold miners instead.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.