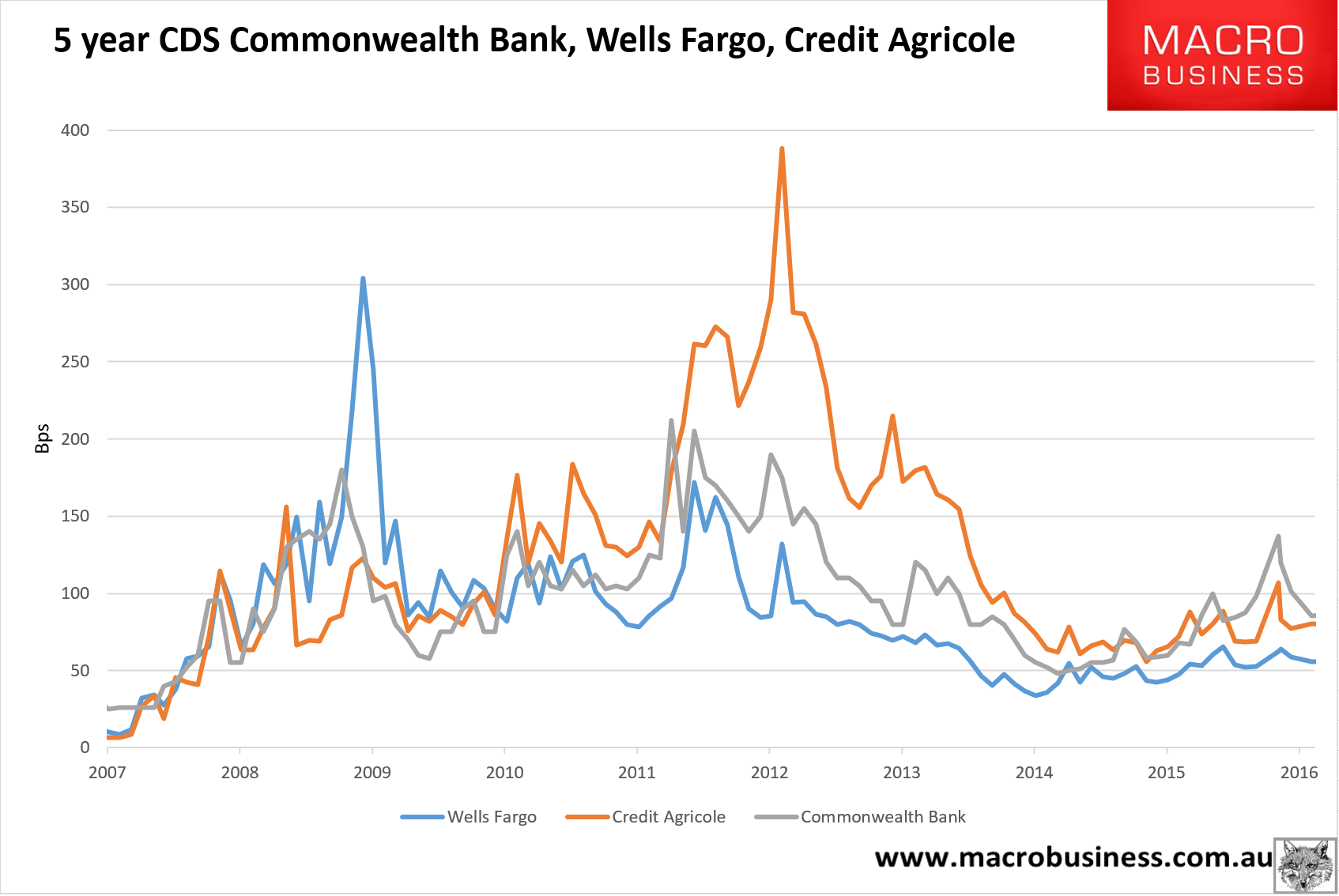

Commonwealth Bank CDS prices continue to plunge hitting 85.5bpd Friday:

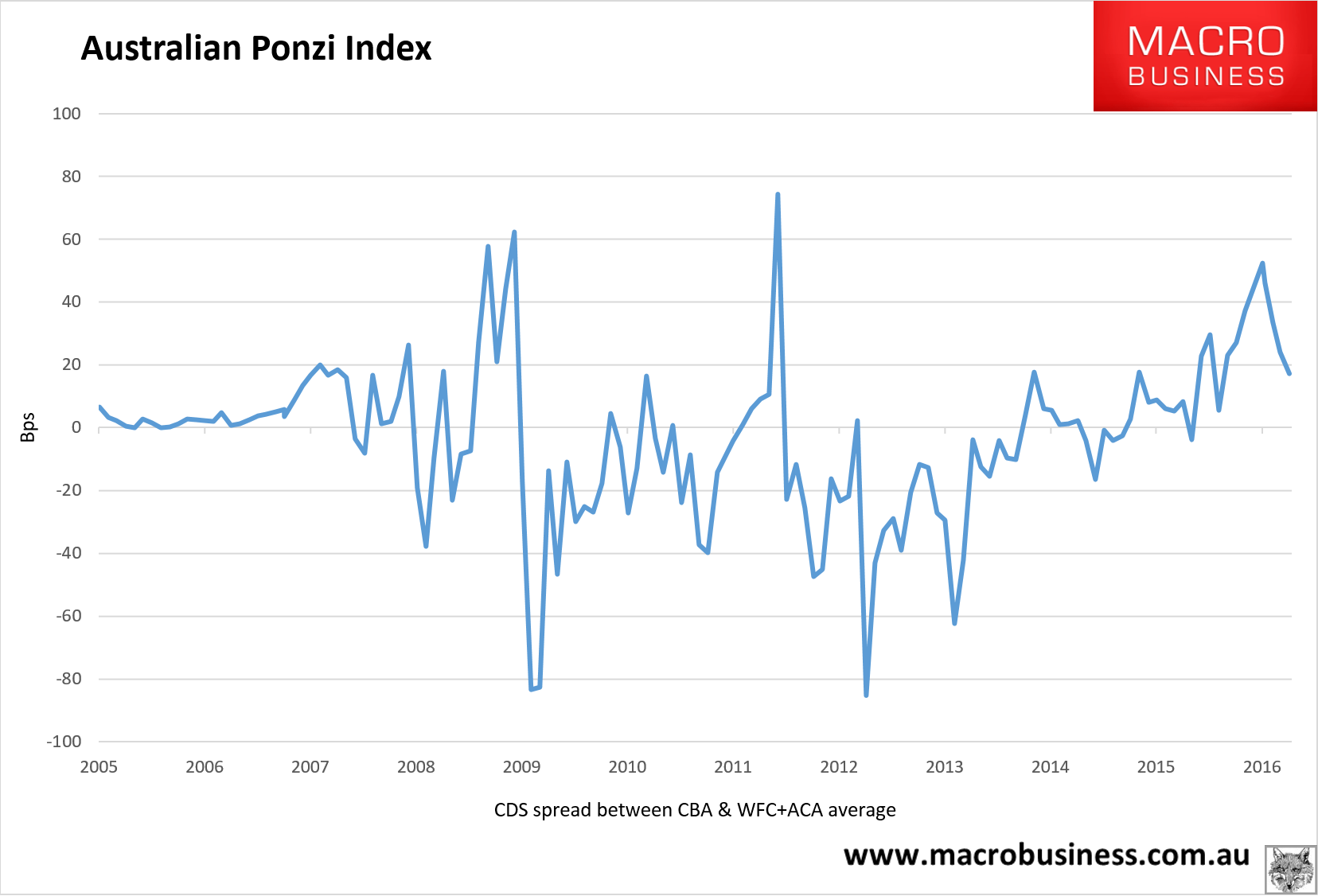

Our European proxy, Credit Agricole, has blown out a little and US proxy, Wells Fargo, has been stable. Australian banks are still leading the global systemic bank spread widening but the gap has narrowed markedly:

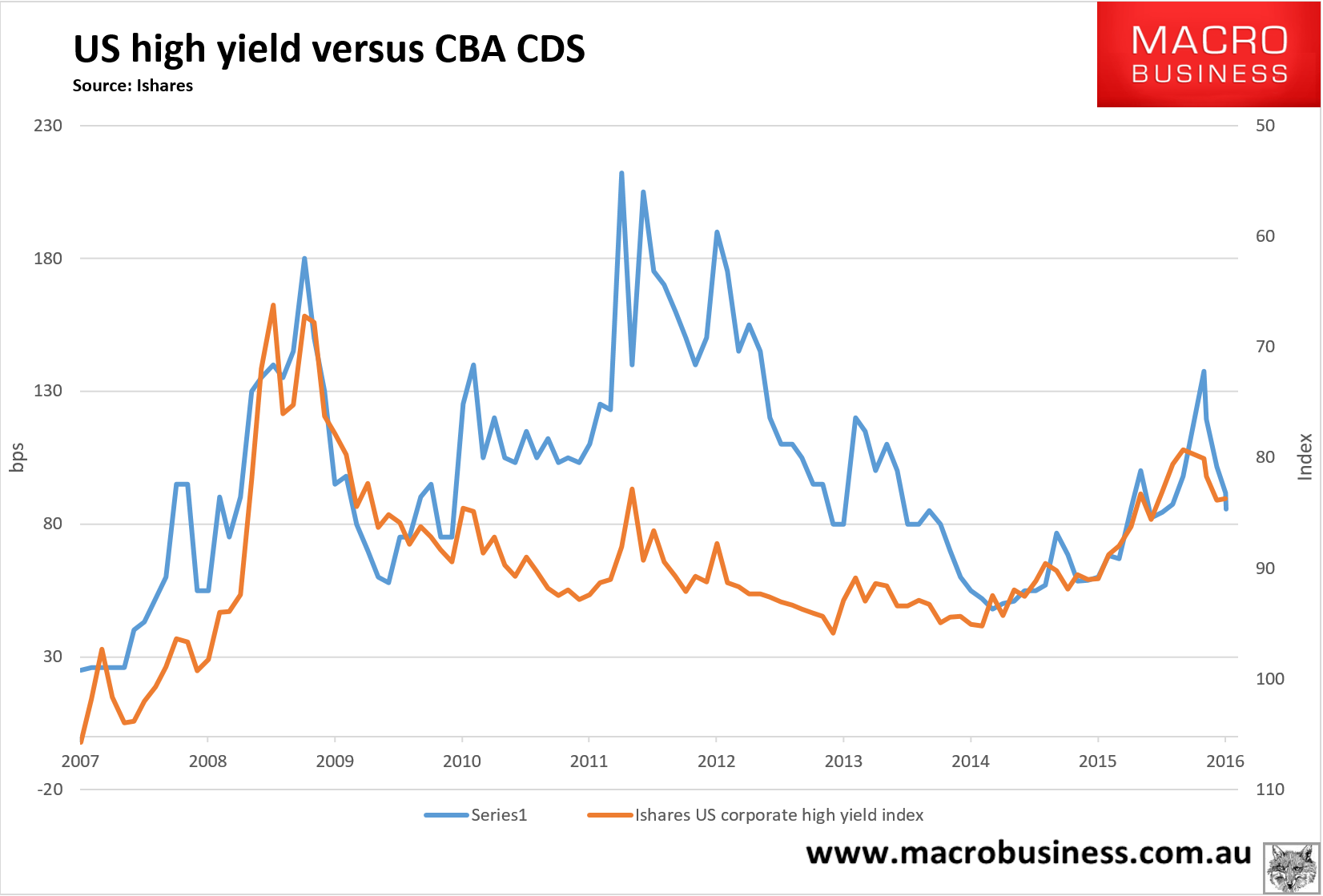

The easing in spreads has been driven by hopes for Chinese growth, easing fears about US rate hikes and the global high yield rally. Those three have Aussie banks performing much better than even US high yield:

The easing opened the debt issuance flood gates in May, from ADCM review:

The month of May saw both the largest monthly volume of corporate issuance since May 2014, and the return of true corporate and non-financial issuers to the market, in some volume.

A total of A$13.1 billion of bonds were issued in the domestic corporate bond market in May, the same volume was seen in May 2014. This is almost twice the average monthly issuance over the intervening period, of a little over A$7.3 billion.

Issuance activity overall was more buoyant in May 2014, with only A$6.35 billion of the total issuance volume being attributable to benchmark sized issuance from bank and SSA sector issuers. Benchmark issuance from the same sectors accounted for a considerable A$9.4 billion of the May 2016 total issuance volume.

nab set the tone for May 2016 by raising a total of A$3.2 billion for five years, at the start of the month. The A$2.9 billion of FRNs issued by nab, in the two tranche issue, is the largest single tranche yet seen.

nab was followed towards the end of the month by Westpac, with a A$2.3 billion five year, raising. Other benchmark issues through the month ranged in size from A$500 million by the Sydney Branch of Bank of China, to A$800 million by the International Bank for Reconstruction and Development.

The other highlight of the month was the return of non-financial issuers to the market. Up until the start of May only one non-financial issuer had been seen, this being Korea National Oil Corporation, which issued A$325 million of bonds in February.

AirServices Australia raised A$400 million early in the month. AirServices Australia qualifies as a non-financial issuer but whether it qualifies as a true corporate issuer is debatable.

There can also be some debate about the qualification of the next to issue, this being Ford Motor Credit Company LLC. Ford raised A$450 million via a global issue, and this follows the A$500 million of global bonds the company sold last December.

Port of Brisbane finance vehicle, QPH Finance Co Pty Ltd, was next to market and was the first domestic true corporate issuer. The company sold A$250 million of seven year bonds, the week before last.

Hyundai Capital Services completed the non-financial issuance for the month by selling a A$350 million of five year bonds.

In all, A$1.45 billion of non-financial issuance was seen in May and it appears that June will see even more.

The Aussie bank spreads have already corrected further than I thought they would or should. My guess is we’re near some kind of bottom but you never know with the Fed now sidelined.