Advertisement

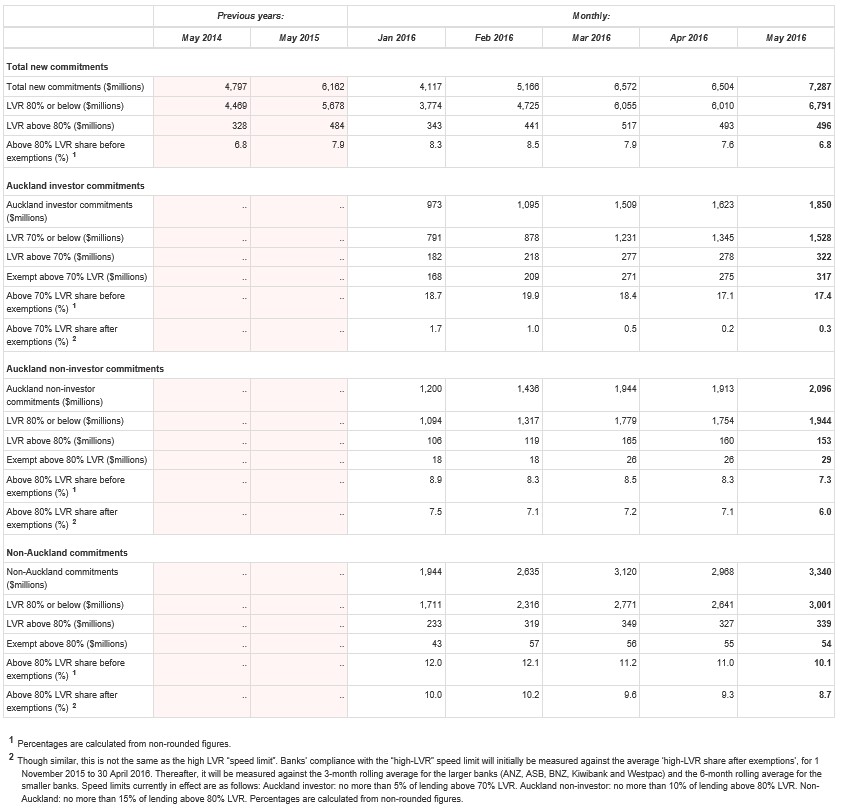

Property investors continue to flood back into Auckland, with the latest data from the Reserve Bank of New Zealand (RBNZ) showing that Auckland investors increased their share of mortgages to 47% in May – the highest level in monthly records dating back to November 2015:

The share of investors in Auckland is also well up on the rest of New Zealand where investors comprised only 25% of total non-Auckland mortgages.

Advertisement

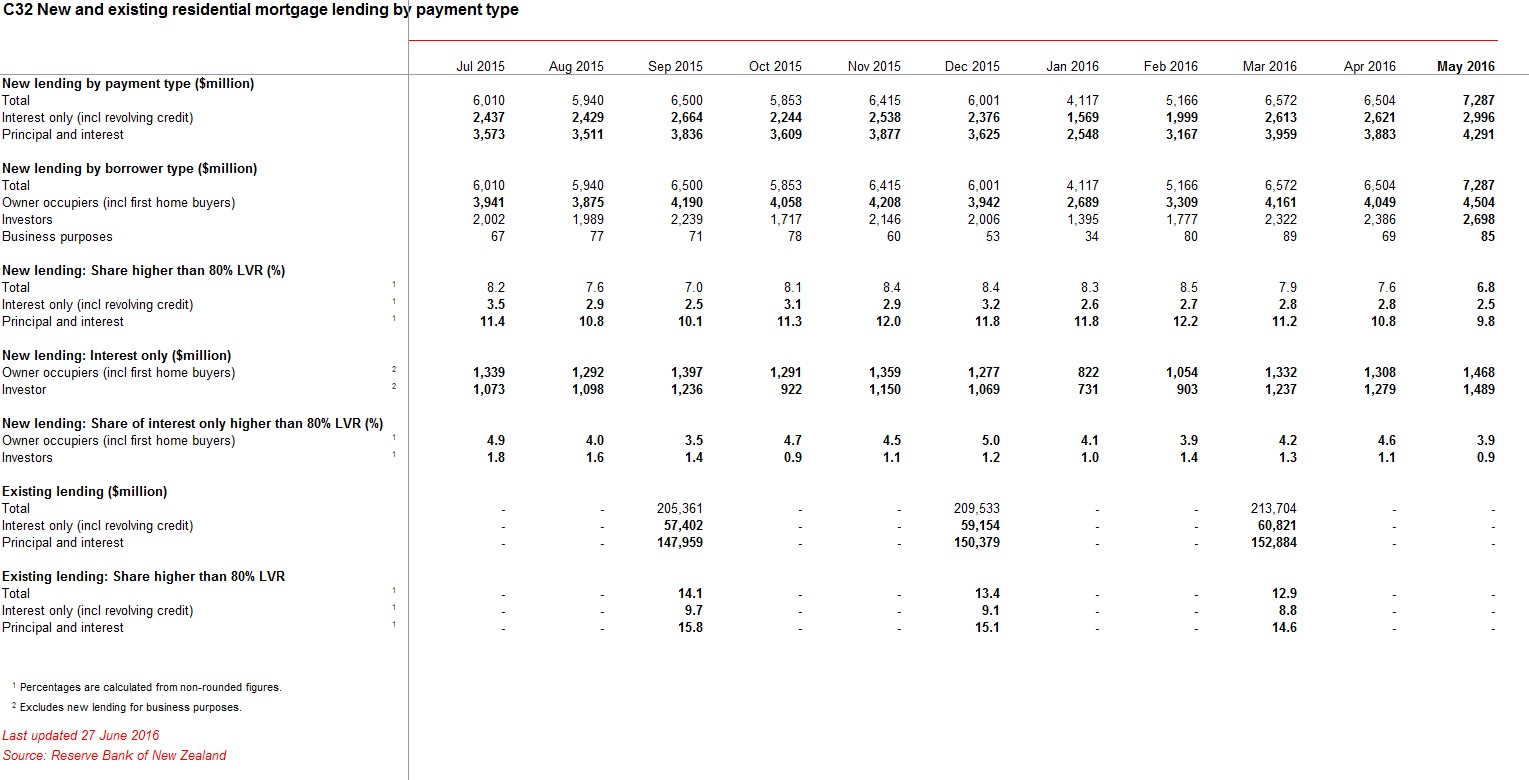

Worse, the share of investor loans that are interest-only has risen to 55%:

With Auckland’s median house price nearing $1 million, and clearly in the throws of a speculative bubble, the alarm bells should be ringing loudly within the RBNZ.

Advertisement

About the author

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.

Advertisement