By Gerard Minack from Minack Advisors

Australia’s slow slump in national income hasn’t yet overwhelmed policy makers, but that seems a growing risk. The RBA now has one less bullet in its depleted holster; fiscal policy hasn’t been reloaded since the GFC fusillade; and the Chinese cavalry isn’t likely to arrive this time. Recession remains a reasonable risk on a 12-18 month view.

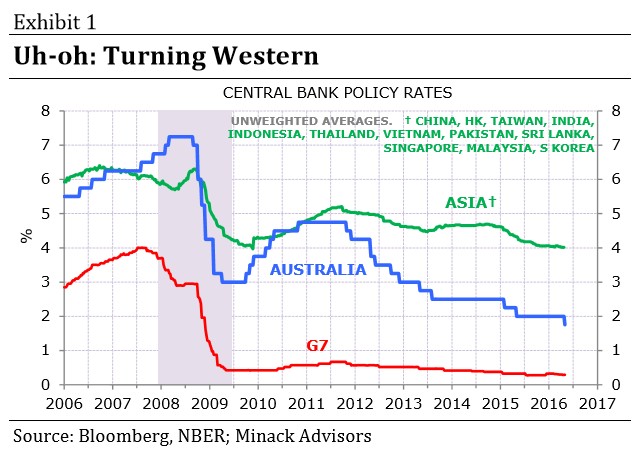

Aggressive policy, first in Australia then in China, saw Australia (and Asia) quickly rebound from the global financial crisis. Australia lifted rates back to Asian levels and senior RBA officials downgraded the GFC to the ‘north Atlantic crisis’ (Exhibit 1).

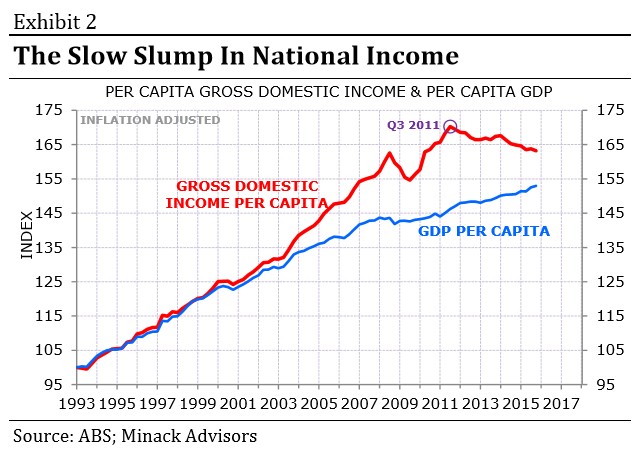

That was then. For the past four years declining export prices has caused a slow slump in national income. Australia is now in the midst of the longest period of falling per capita income since quarterly data started in 1959 (Exhibit 2). Australian rates are looking less Asian and more Atlantic.

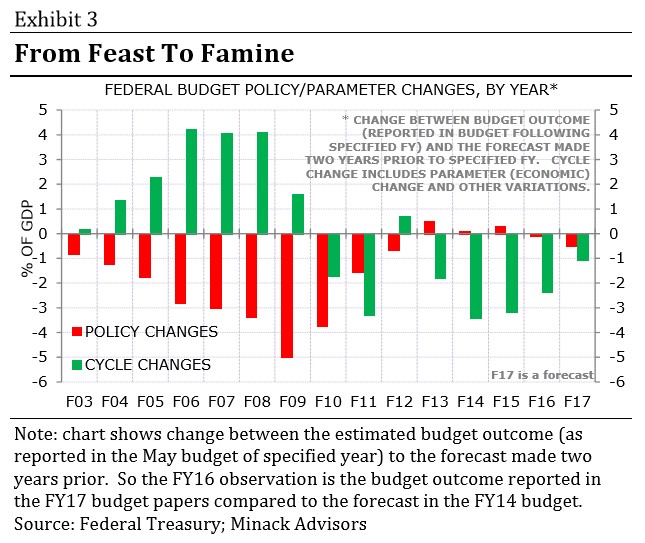

The Federal government was the largest beneficiary of the boom and now is the largest casualty of the bust. The boom gifted Canberra annual windfalls worth 2-3% of GDP – windfalls that were largely spent. The bust is now costing the budget 2-3% of GDP – losses that have largely not been passed on through tighter fiscal policy (Exhibit 3).

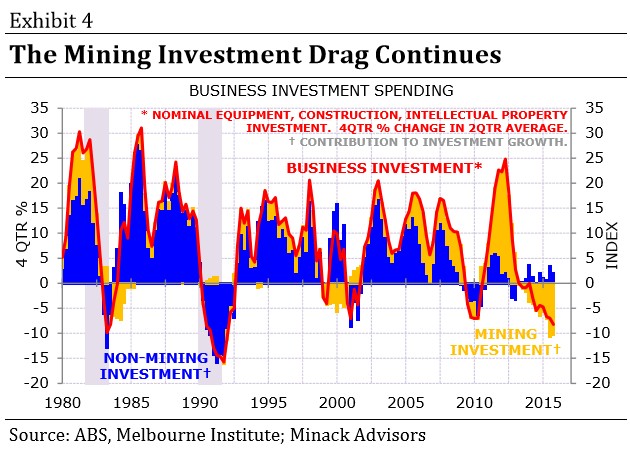

The income boom-bust was accompanied by the mining investment boom-bust. The ongoing decline in mining investment will almost certainly continue to offset investment spending elsewhere through the course of this year (Exhibit 4).

The declines in income and investment could have caused a recession (particularly if fiscal also had been tightened). Instead, the impact has been partly offset by the falling A$ and easier RBA policy.

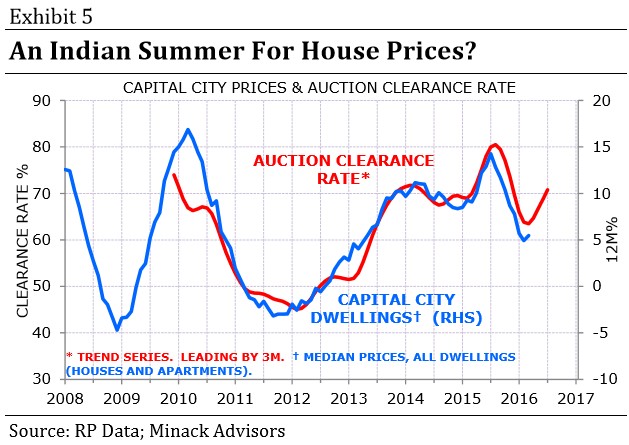

Low rates have been notably successful lifting housing activity and house prices. Domestic demand increased by 1% through 2015, of which housing-related activity contributed 0.6 percentage point. The latest rate cut may add to prospective near-term house price gains (Exhibit 5).

Looking ahead, however, there are three problems. First, the drags – falling mining investment and the normalising terms of trade – continue but there is now less room for policy to provide an offset.

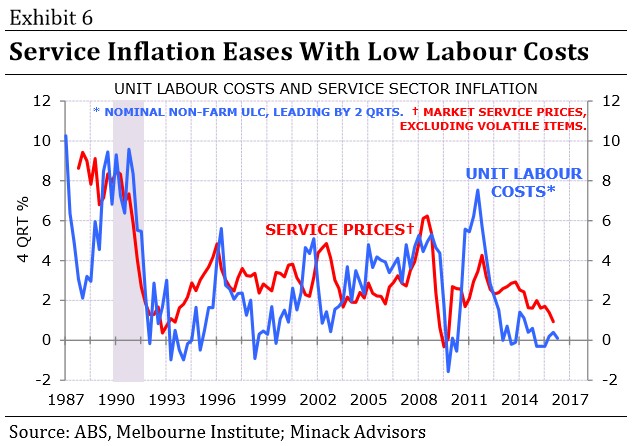

Second, Australia is now seeing a material drop in underlying inflation pressure. This is partly a reflection of weakness in global activity and pricing, but it’s also a reflection of the domestic income recession. The result is unit labour costs barely rising which is dragging down inflation (Exhibit 6).

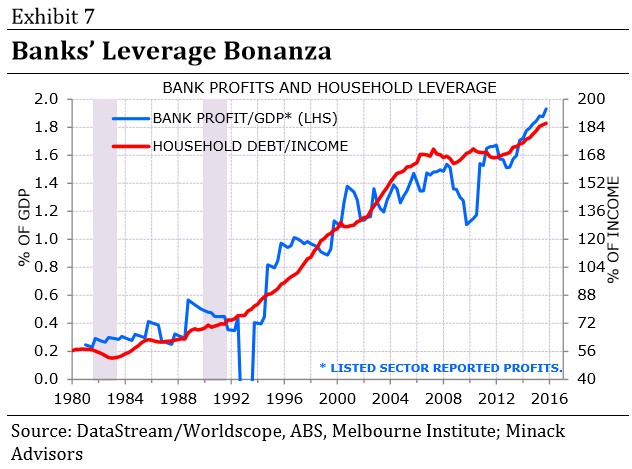

Third, the cyclical success of low rates has exacerbated the structural excess in household leverage and house prices. This may be the final phase of the three decade super-cycle of escalating household debt, house price re-rating, and super-normal bank profits (Exhibit 7).

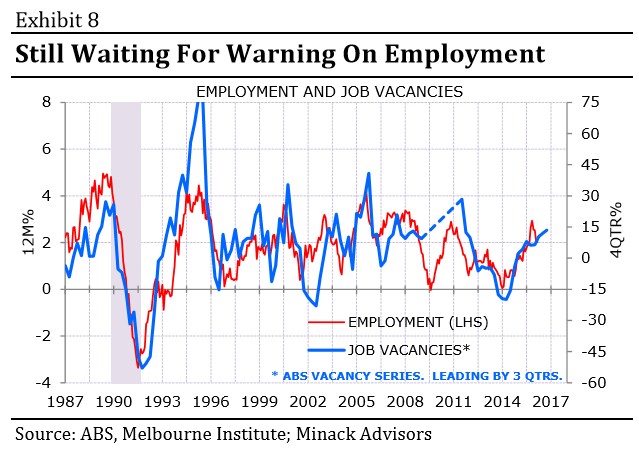

Although the risks are rising, my view on timing remains the same: don’t make recession an investment base case until leading indicators of labour demand soften. For now they are not: hiring intentions remain reasonable; the number of job vacancies is consistent with solid jobs growth (Exhibit 8). The leading labour indicators are not particularly far-sighted, so do not count against a recession heading into next year. But I want to see the indicators turn to confirm the recession risk.