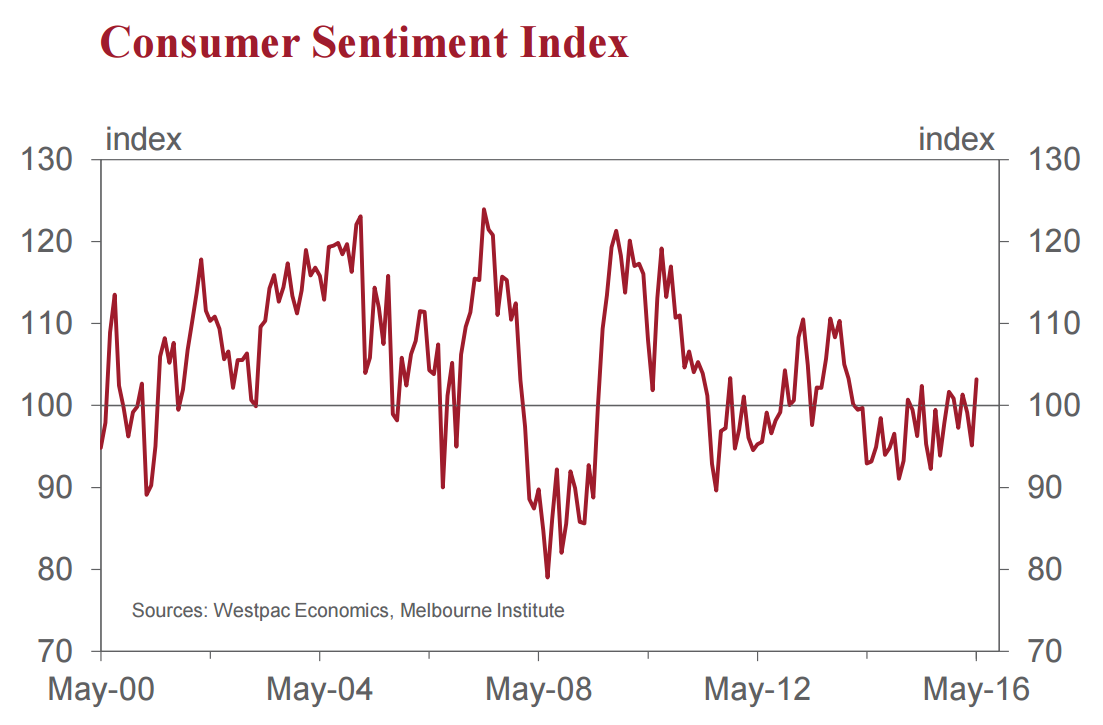

The Index has now reached its highest level since January 2014.

This result would have been affected by two very significant events: the Commonwealth Budget and the Reserve Bank’s decision to cut the overnight cash rate from 2% to 1.75%.

Our analysis indicates that the dominant driver of the boost to confidence has been the rate cut.

Sharp increases in the Index in response to rate cuts are fairly common, although they depend somewhat on other events at the time and whether moves were expected. The last four rate cuts have seen the Index rise on average 6.6%, with gains ranging from 3.5% to 8.5%.

Supporting this view has been a stunning 15% increase in the confidence of those respondents in the survey who currently have a mortgage.

On the other hand we were able to gauge respondents’ specific assessments of the Budget by asking the special question: “What impact do you expect the Federal Budget to have on your family finances over the next 12 months?” The net percentage was -22.4% compared with -22.5% in 2015 and -56.1% in 2014 (a negative means respondents saying ‘deteriorate’ outnumber those saying ‘improve’).

Since we started asking this question in 2010 all net responses have been negative and the 2016 response is the second highest over that period (the highest being –17.1% in 2010). But this result is hardly the sort of glowing response that would explain an 8.5% jump in the Sentiment Index.

Other aspects of the survey were also encouraging. Both Westpac and the Government are forecasting the unemployment rate to fall further to 5.5% by mid- 2017. Consistent with this view was a 5.8% fall in the Westpac Melbourne Institute Index of Unemployment Expectations to its second lowest level since January 2012. If sustained, this fall in the Index will be consistent with our expected steady improvement in labour market conditions.

All components of the Index improved in May. The sub-index tracking respondents’ assessments of their family finances compared to a year ago increased by 3.2% while the sub-index tracking the one year outlook for family finances lifted by 7.2%.

The economic outlook also improved. The sub-index tracking the one year outlook jumped by 13.2% and the sub-index tracking the 5 year outlook rose by 14.8%. 11 May 2016

The ‘time to buy a major household item’ sub-index increased by 4.9%.

A word of caution is appropriate at this juncture. The Reserve Bank strongly favours the ‘family finances vs a year ago’ subindex as an indicator of future spending patterns. This component increased the least in the survey and is still below its level of two months ago.

Consumers’ assessments of housing conditions improved, although there was a fall in confidence around the outlook for house prices. The ‘time to buy a dwelling’ lifted by 12.1%, although it is still 6.4% below its level a year ago. The strongest gains were in the most volatile state – New South Wales.

On the other hand, we saw a more subdued outlook for house prices with a 2.6% fall in the Westpac Melbourne Institute Index of House Price Expectations. This Index is now 15.9% below its level of a year ago.

The Reserve Bank board next meets on June 7. We expect the Board to keep rates on hold at that meeting although we are expecting a further rate cut at the August meeting. The Reserve Bank targets inflation and its latest forecasts point to the underlying inflation rate holding at 1.5% in 2016 – below the bottom of the 2-3% target band. That is uncomfortable but nevertheless acceptable if the forecast is for inflation to move back comfortably within the band in 2017. Current forecasts are for underlying inflation to only move to the bottom of the band in 2017, despite the Bank including a follow up rate cut in its forecast assumptions (due to its practice of adopting market pricing for its interest rate assumptions for the forecast).

It seems likely that it will have to deliver that cut in August after it has had time to further analyse the inflation trends in the June quarter and the March quarter national accounts.

I expect this to fade pretty quickly and do not expect any great follow through in house prices as:

the Chinese bid evaporates;

investors struggle;

the election weighs, and

and the second half gets tougher with the capex triptych, AAA downgrade and Budget failure.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.