Michael Potter from conservative think tank, the Centre for Independent Studies (CIS), has penned a terrible piece in The Australian today defending negative gearing.

Let’s assess Potter’s key arguments:

…the negative gearing abolitionists now trumpeting that the RBA is supporting a change would do well to look at it more closely.

…restricting negative gearing might make the financial system more stable, but at what cost to the rest of the economy? And the issue of stability is already being addressed with a recent tightening of prudential requirements for investor loans.

This leaves only the RBA’s stated downsides of changes to negative gearing: fire sales of negatively geared properties (which the ALP tries to address with grandfathering) and — more importantly for low-income earners — the increases in rents.

Clearly, if rents are hiked, this will hit low-income households harder, as they spend proportionally more on rent…

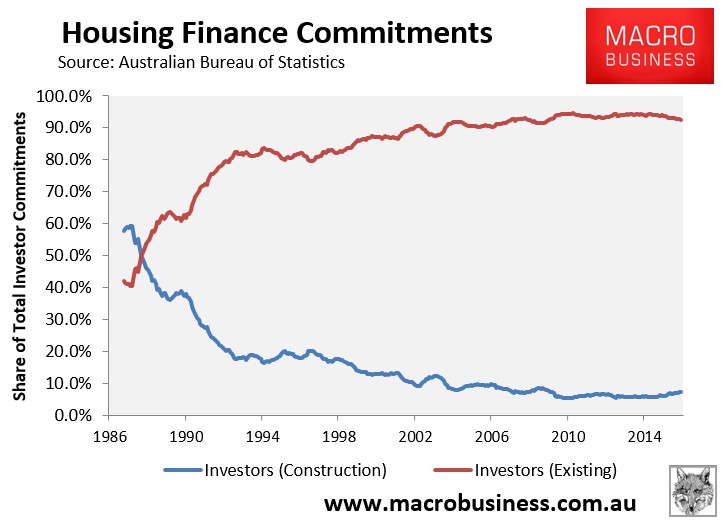

Nice straw man argument there. Tell me Michael, why would rents rise when the overwhelming majority (93%) of investors purchase existing dwellings?

Wouldn’t less “investment” mean that there are more homes available for sale rather than rent, and that more renters would become owner-occupiers, thus leaving the rental supply-demand equation unchanged?

You also conveniently failed to mention that Labor’s policy to direct negative gearing to new builds would boost supply, thus leading to more rental stock and placing downward pressure on rents.

Heck, Labor’s policy on negative gearing is virtually identical to the Coalition’s stance on foreign investment, whereby foreigners are restricted to buying newly constructed dwellings only. Here’s the chair of the foreign investment inquiry, Liberal MP Kelly O’Dwyer, explaining the benefits of this ‘new homes only’ policy:

“Currently the framework seeks to channel foreign investment in residential real estate into new dwellings in order to increase the housing stock for Australians to build, buy or rent. Foreign investment is encouraged in new dwellings whether they be apartments, units or homes because in addition to creating more supply, it also creates more jobs for the building and construction sector – all of which helps to grow our economy”.

So your suggestion that Labor’s policy would choke rental supply and force-up rents clearly does not pass scrutiny. If anything, the outcome would be the opposite: increased dwelling supply and lower rents.

Back to Potter:

…we can’t be confident that the ALP’s policy will result in a moderation of house prices, surely a goal of a policy to improve housing affordability.

For example, increased rents may encourage some renters to buy properties, increasing prices; similarly the ALP’s policy restricting negative gearing to new properties may increase the price of new dwellings.

It isn’t clear that these price increases will be offset by any reduction in the price of old properties.

Tying yourself in knots there Michael. We already have established that Labor’s policy would lower rents (other things equal). Second, given investors comprise roughly half of all mortgage demand (excluding refinancings), Blind Freddy can see that reducing demand from this cohort, while boosting supply, would reduce pressure on house prices and boost affordability.

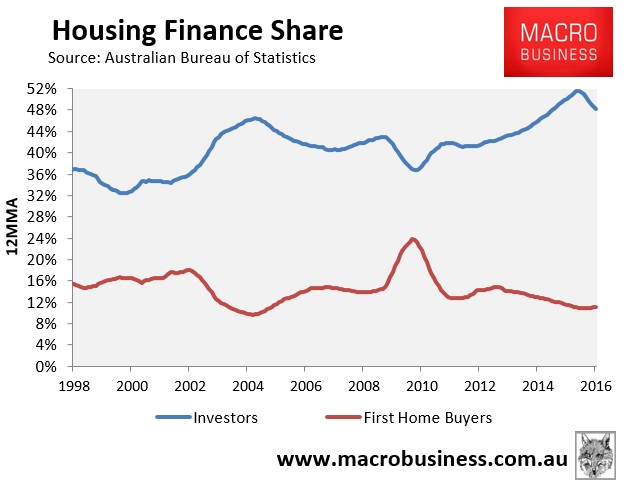

In turn, first home buyers – who have clearly been crowded-out by investors (see next chart) – would have more opportunities to enter the housing market. It’s not rocket science.

Back to Potter:

Playing with negative gearing would (further) interfere with a fundamental part of the tax system: costs should be deductible against income.

There are already some tweaks to this rule; and the more tweaks that are made, the more complex the system will become and the greater the incentives for tax avoidance.

If the tax system is so pure then why is it that workers cannot deduct their travel to/from work or child care from their tax?

And why is it that the current tax rules allow individuals to claim unlimited negative gearing deductions for property investments into perpetuity, but if they invest in a productive side business, they must meet all kinds of criteria before they can claim losses against their wage/salary earnings, including showing a profit in three out of five years?

Malcolm Turnbull knows this, which is why he noted in his 2005 tax policy paper that “Australia’s rules on negative gearing are very generous compared to many other countries” and that “the normal deductibility principles do not apply to negatively geared real estate such that the taxpayer is not obliged to demonstrate that the negatively geared property will generate positive cash flow at some point in the distant future”.

Back to Potter:

But more importantly, the tax system will become further biased against risk-taking. If you can’t deduct losses, then the incentives to invest in riskier assets and enterprises will be reduced — a poor result for what should be an innovative economy.

First, Labor Shadow Treasurer, Chris Bowen, has already explained that its negative gearing policy would only apply to “passive” investments – like property and shares – not genuine “active” business investments. Thus, there would be no changes to the tax rules for genuine productive investments.

Second, in his 2005 tax policy paper, Malcolm Turnbull described negative gearing and the CGT discount as a “sheltering tax haven” that is “skewing national investment away from wealth-creating pursuits, towards housing”.

Third, if there is one sector that is losing-out from the current taxation arrangements it is businesses.

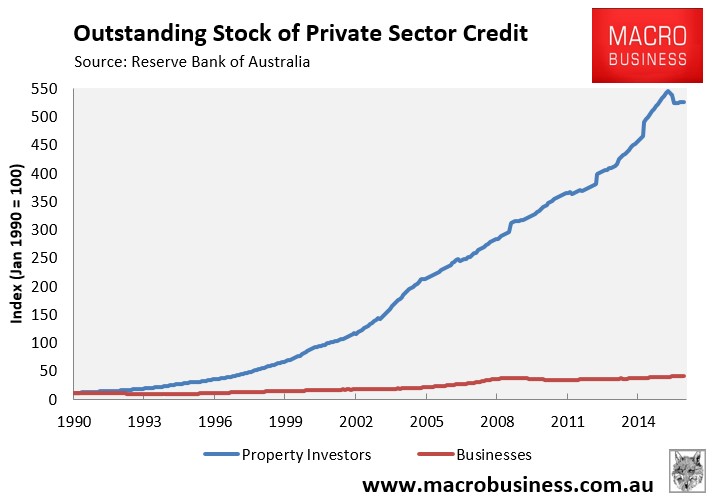

Since negative gearing was reinstated in 1987, lending to property investors has risen almost exponentially while business lending has flatlined (see next chart).

It is precisely productive business lending, particularly lending to small enterprises, that is being crowded-out by housing lending.

Policy discussion deserves better than an open tax dodge protected by a nominally “free market” think tank.