The Pre-election Economic and Fiscal Outlook, or PEFO, will be released by Treasury which prepares the economic statement without any input from the government.

…”Once PEFO has been released there are no more excuses for Labor. They must show by how much the budget bottom line would deteriorate as a result of their unfunded spending promises so far in each year of the forward estimates,” Finance Minister Mathias Cormann said.

“Unfunded spending promises lead to higher taxes which hurt jobs and growth and Labor spending promises without explaining how they would pay for them make them meaningless and unable to be delivered.”

…In his reply to the budget at the National Press Club last week, shadow treasurer Chris Bowen pledged he would release before election day the full details of Labor’s costings based on the estimates in PEFO. He also promised that if elected, Labor would hand down a mini-budget within 100 days taking into account what it says would be more realistic forecasts for real and nominal economic growth and the iron ore price.

If I were you, Mr Cormann, I would be treading very carefully around allegations of unfunded promises given the outrageous forecasting lies that underpin your own outlook including:

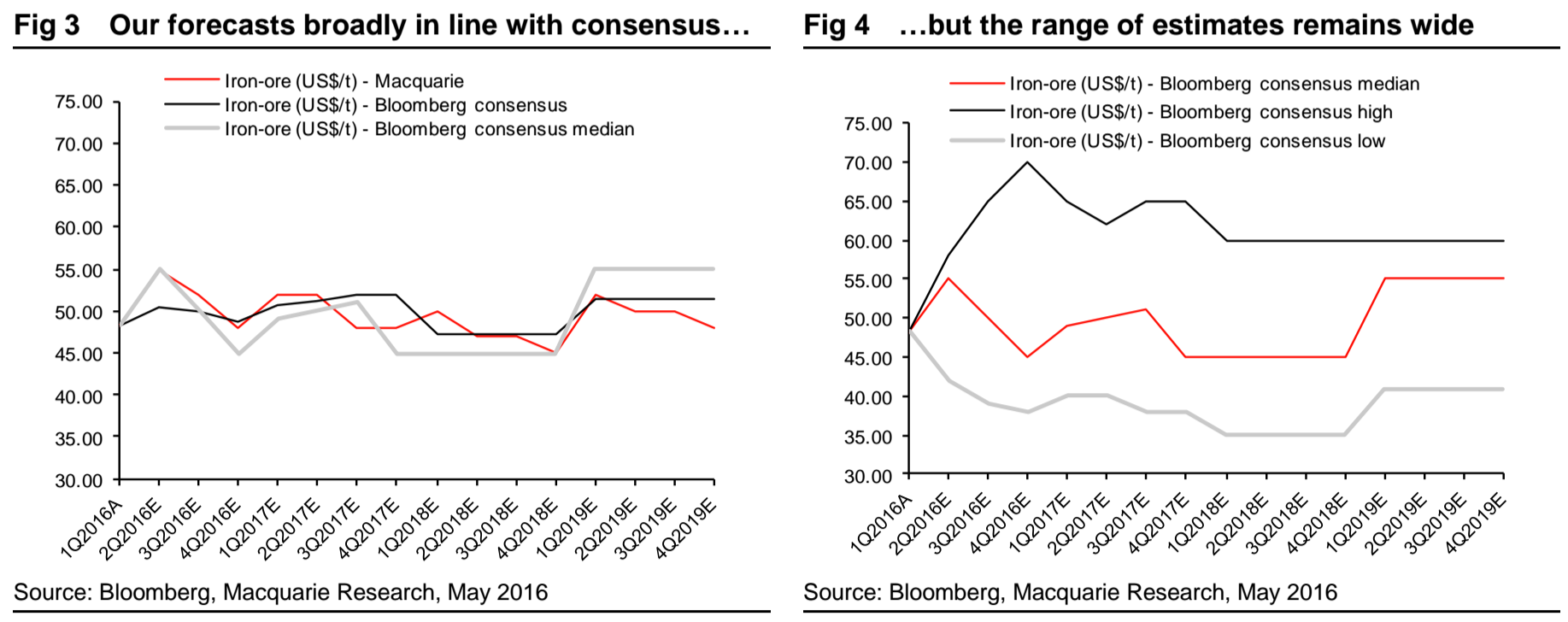

a ludicrously stable terms of trade and a farcical iron ore price of $60CFR versus $47.70 in the WA Budget, a market already at $55 and Singapore futures (the best forecaster by far) at $35 for 2016/17. Even heavily conflicted sells side research can’t bring itself to get above a sub-$45 consensus:

Advertisement

leading to $8 billion over-estimated revenue per annum, and

1-1.5% over-estimates for nominal growth killing just about every other parameter.

If I were Mr Bowen I would launch a full blown attack on these lies and the jeopardy in which they have placed the AAA rating. To wit, Moodys after the Budget of Lies:

Advertisement

“The projected increase in revenues as a share of GDP is based on a return to robust nominal GDP growth which generally comes with a higher revenue-intensity of growth. Our forecast for nominal GDP growth is somewhat more muted than the government’s. We estimate that the adjustment to an environment of lower commodity prices is still underway and will continue to weigh on corporate profitability and wage growth. As a result, improvements in the government’s revenues may be somewhat more muted than currently budgeted.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.