Reality appears to be setting in that Australia’s labour market, whose deteriorating fundamentals have been on display for several months already, is not as strong as previously thought.

Here’s Jacob Greber at The AFR:

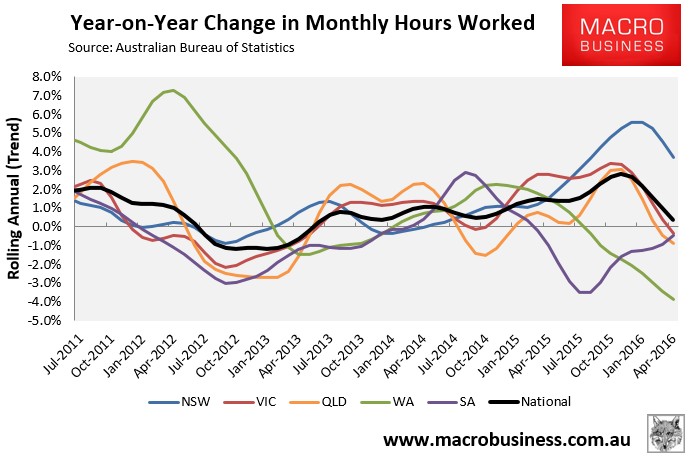

Hours worked by Australians have fallen over the last 12 months in every state other than NSW, raising fears a year-long resurgence in the labour market may be running out of steam.

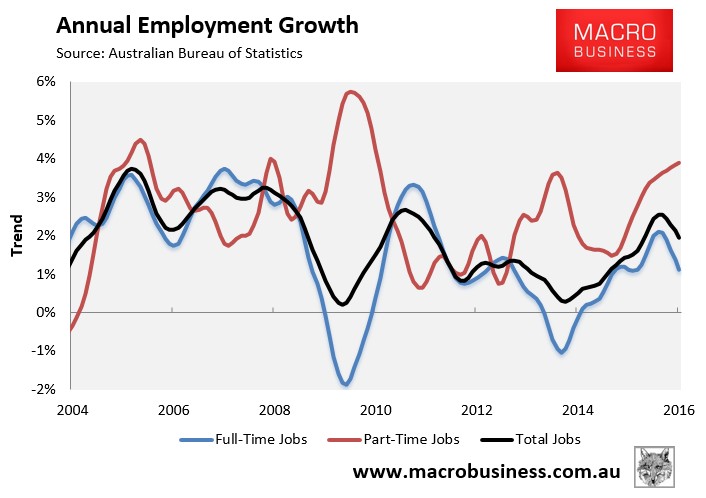

…economists warn the decline in hours worked is being driven by a huge surge in more volatile part-time jobs, which have risen over the last year by 161,000, or double the gain in full-time work.

More broadly, total jobs growth over the first four months of 2016 has averaged just 6500 per month, which is less than half the number of jobs normally required to bring down the jobless rate…

Paul Dales, an economist at Capital Economics, warned that the figures confirm growing concerns about the “quality” of many of the more than 300,000 jobs that were generated in 2015.

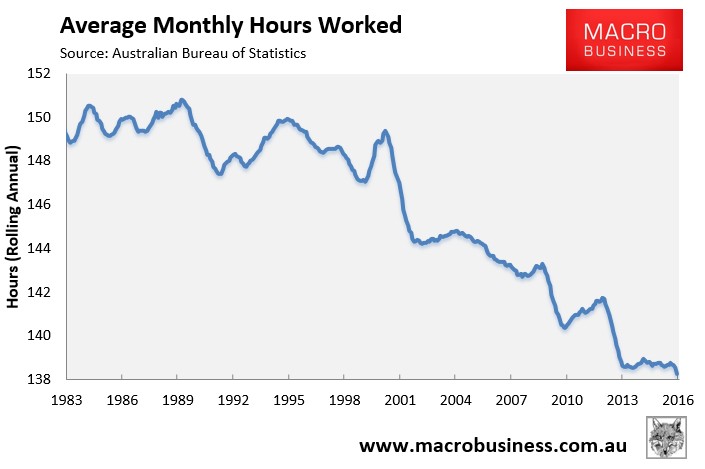

He estimates that average hours worked per employee per month has fallen to a record low of 135, a sign that companies are paring back wage costs in an attempt to avoid firing staff.

The figures also reflect sliding wages growth, which has fallen to a record low.

And more via The ABC:

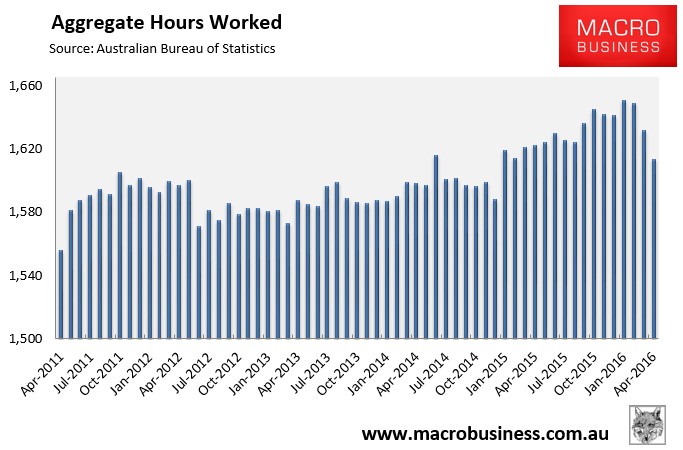

It is the first time in three years that annual total hours worked has fallen, down 0.5 per cent over the 12 months to April…

Commonwealth Bank economist Gareth Aird said, while the fall in hours worked appears inconsistent with jobs growth, there is a logical explanation.

“The disparity is explained by the big lift in part‑time jobs over the past year,” he observed in a note on the data.

“There have been twice as many part-time jobs (161,000) created as full-time jobs (83,800).”

Indeed. The ABS jobs numberwang in October and November, was always too good to be true. And the truth was revealed yesterday when hours worked plummeted, down 0.5% year-on-year in seasonally adjusted terms:

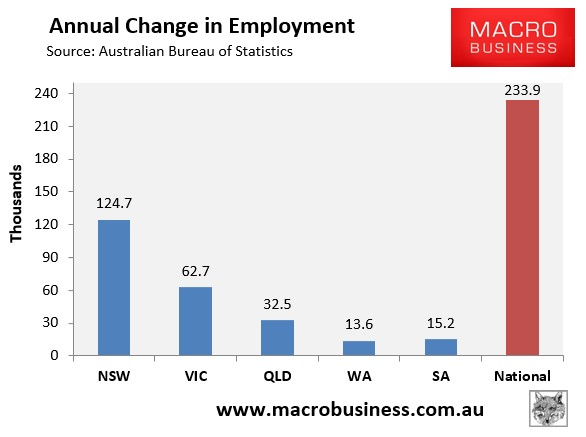

With the trend weakening everywhere and negative in all major states except NSW:

Moreover, average hours worked also hit another record low:

The reason for the above weakness is, of course, because most of the jobs being created have been part-time, presumably low paying jobs in the services sector, with full-time jobs growth piss weak:

And because of this, average wages growth has fallen to just 1.99% in trend terms – the lowest rate on record:

And while it won’t be revealed for another quarter, average weekly earning growth is likely weaker still given the ongoing rotation out of highly paid mining jobs into low paying services jobs.

The question is, is this a turning point in the cycle or just a pre-election blip? From Westpac:

Westpac has for some time argued that observed lift in part-time employment is likely to be more about which sectors are now expanding and which sector are now contracting, such as the growth in service industries as mining and manufacturing restructure, rather than any significant change to the employment arrangements within the sectors. This continued into April with female employment rising 164.4k in the year (3.1%yr) compared to the 80.3k (1.3%yr) rise in male employment.

The fact that the participation rate was flat this month at 64.9 was somewhat surprising. We now observe a trend decline in participation, from an average of 65.09 in Q4 to 64.95 in Q1. With a 64.84 print in April the average is set to dip again in Q2.

This decline in participation is likely to hold the unemployment rate convincingly under 6% even if we see a soft patch in employment through the next few months.

One cautionary sign may be the recent sudden decline in hours worked (–0.5%yr). Given this dip in hours worked was driven by a collapse in hours worked per full-time employee, it may pointing to some near terms risks to the outlook for employment.

When the observation on hours worked is combined with our analysis of the gross flows data, which suggests that we may be in midst of a ‘hiring freeze’, then we may be entering a classic pre-election pause in employment. While this would correct post the election it may mean we see softer employment prints for the next few months. However, in this case softer participation is likely to prevent any spike up in the unemployment rate.

That’s no doubt true but we should remember that the majority of jobs growth has come via NSW and VIC, which are experiencing monumental housing price/construction bubbles:

And at some time in the second half of this year these construction booms will peak and begin to decline. Add the ongoing mining capex cliff and car industry closure and the headwinds for employment growth will strengthen post-election even if wider conditions improve a little.

This labour market cycle has been luke warm at best and is very likely past its best. We do not see a precipitous decline ahead in the second half but add any kind of shock to what will now be chronically under-performing jobs market and and we soon will.