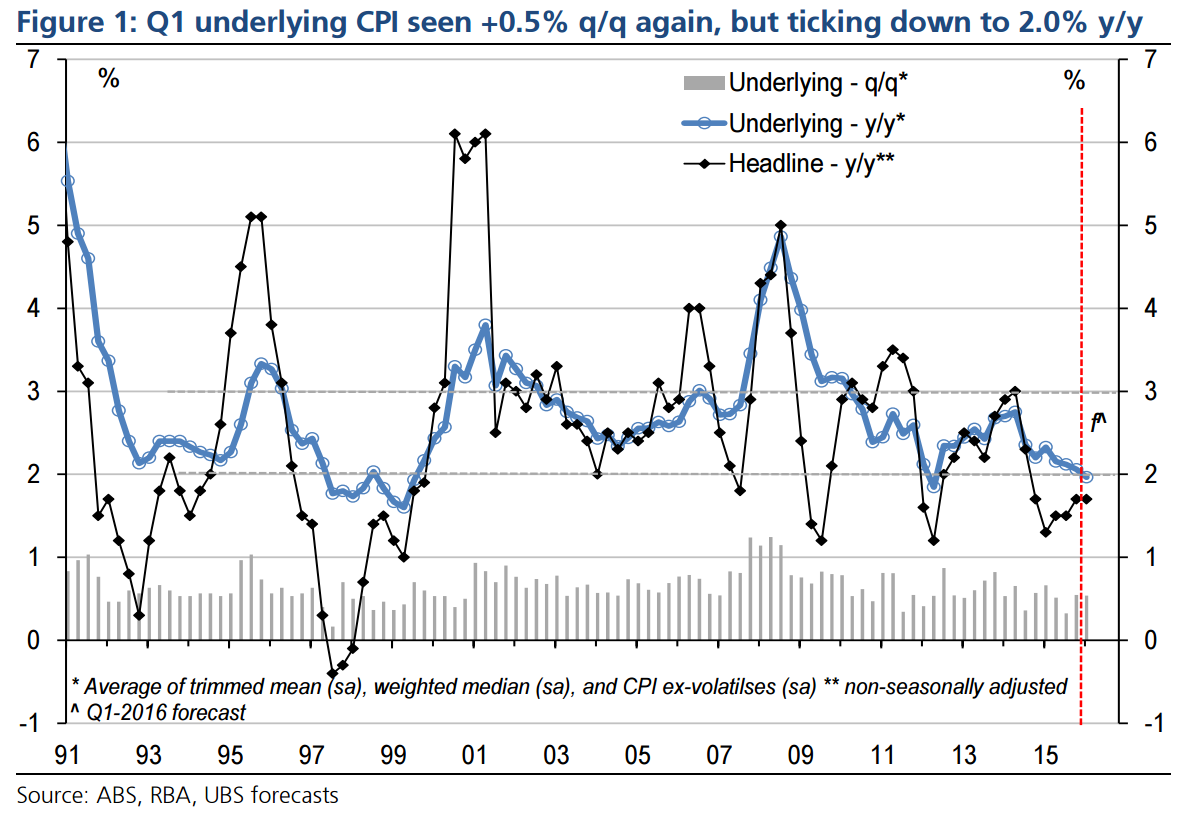

Based on our proprietary inflation survey, we cut our Q1 headline CPI forecast (due 27th April) by 0.2% pts to 0.2% q/q. This holds the y/y at 1.7%, staying ‘below target’ for a 6th consecutive quarter. Given the RBA’s mid-year target of 1½% y/y implies quarterly gains of 0.35%, a 0.2% q/q print would present the RBA some downside risk.

Of course, the low headline print is driven by a 10% q/q slump in petrol that alone subtracts ¼%pt. Elsewhere, global disinflationary pressures are still dragging, the boost to imported prices from the typically lagged pass-through of AUD deprecation is likely less dominant in Q1 given the AUD TWI’s recent bounce, while competitive pressures remain in play in food. Record low wage growth & weak business selling prices also imply low CPI, but the pick-up of consumption in 2H-15 suggests some price pressure.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.