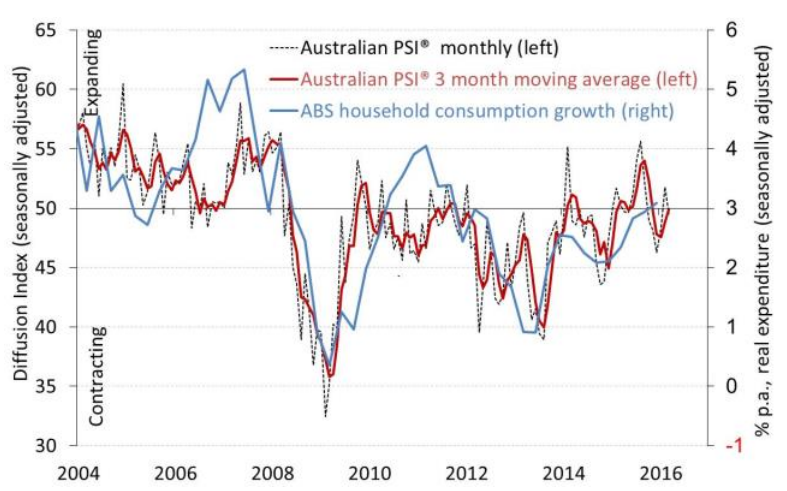

The Australian Industry Group Australian Performance of Services Index (Australian PSI® ) dropped by 2.3 points to 49.5 points in March indicating a broadly stable month for the services sector after expanding in February (results above 50 points indicate expansion with higher numbers indicating a stronger rate of expansion).

Of the five of activity sub-indexes in the Australian PSI® new orders expanded in March (51.9 points) but the other four indicators were below 50 points and indicating stable conditions or net contraction. Sales went from a strong result (55.7 points) in February to stable (49.4 points) in March, deliveries softened but remained broadly stable (49.3 points), while stocks (48.3 points) and employment contracted (47.8 points).

Six of the nine services sub-sectors in the Australian PSI® were stable or expanded in March (three month moving averages) improving from three sub-sectors in February. Finance & insurance (54.2 points), health & community services (58.4 points) and personal & recreation services (53.1 points) all continued their positive run. Wholesale trade (50.5), hospitality (50.9 points) and communications services (51.0 points) all went from contractionary conditions to stable. Retail trade (47.3 points), transport & storage (45.2 points) and property and business services (48.8 points) all remained in contraction in March.

The Australian PSI® results for March suggest continued strength in households services but weaker conditions in goods distribution sectors (retail, wholesale and transport services) and in business services.

The input costs (58.2 points) and wages (54.2 points) sub-indexes of the Australian PSI® remained in expansion in March but selling prices contracted (46.9 points) in March after a stable month in February. This indicates that services businesses are facing margin pressures. Respondents observe increasing competition in the services sector with businesses reluctant to pass on increased input costs (such as those being caused by a lower Australian dollar).

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.