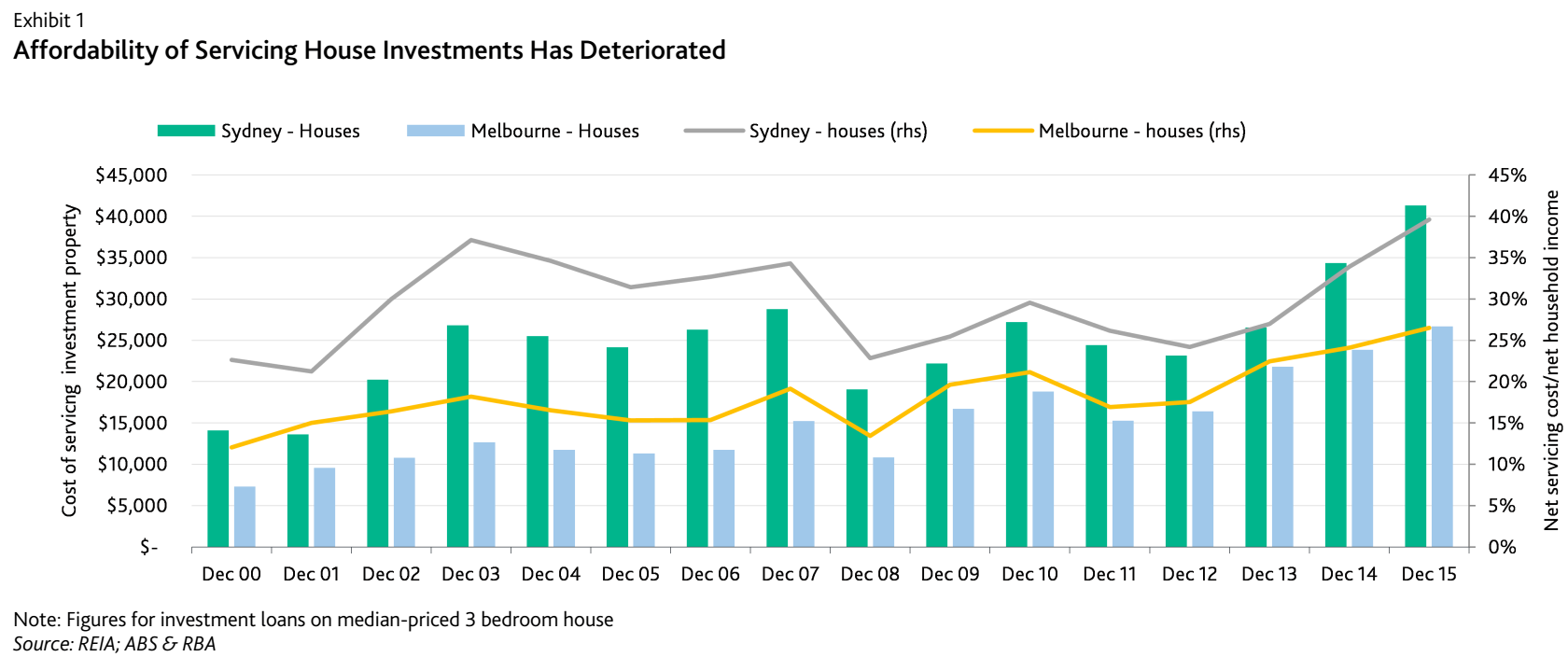

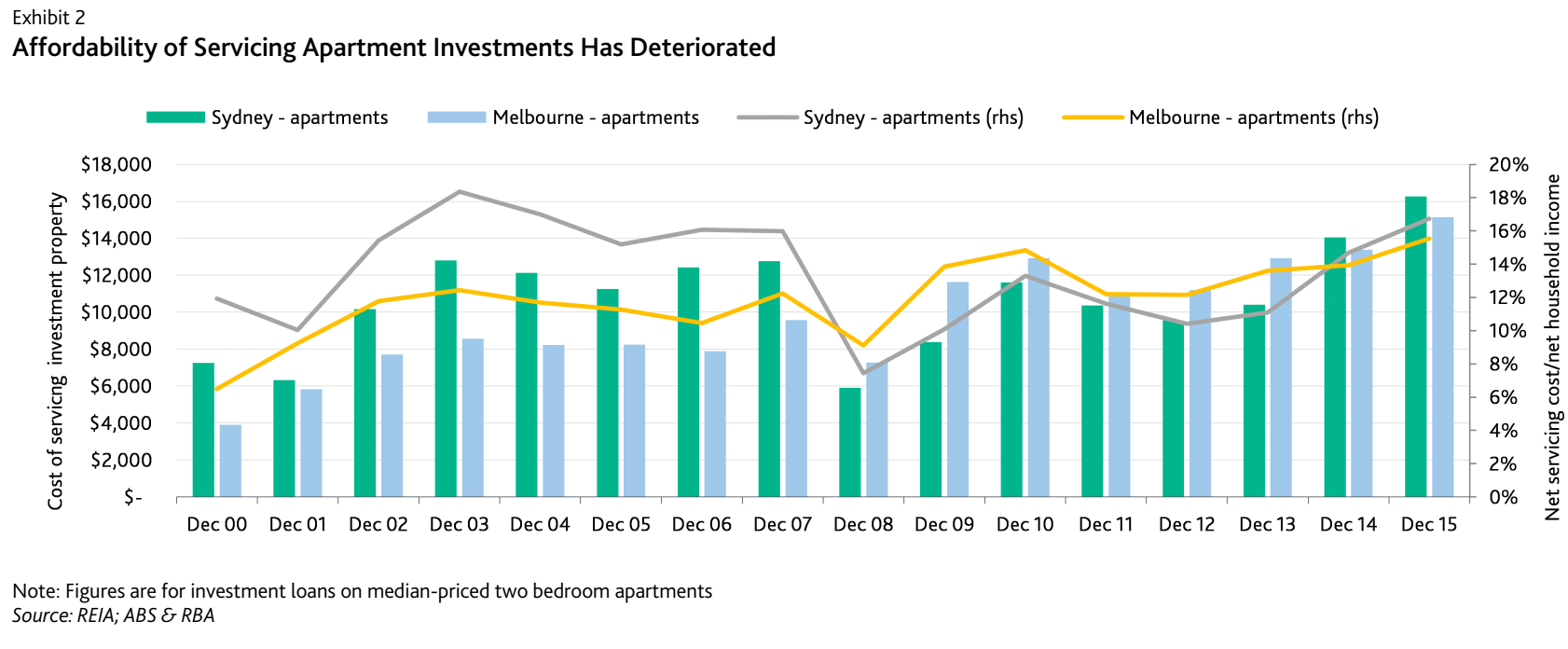

Moody’s Investors Service says rental yields on houses in Australia’s two biggest cities, Sydney and Melbourne, have declined to record low levels, increasing the risks for residential property investors and ultimately, residential mortgage-backed securities (RMBS).

Moody’s says the low rental yields have resulted in increased net costs in servicing a housing investment relative to household incomes, making investment properties less affordable. Net costs refer to investment loans costs less rental income.

“Deteriorating affordability increases the risks for Australian residential property investors and therefore for residential mortgage-backed securities backed by loans on investment properties,” says JP Truijens, a Moody’s Assistant Vice President.

“The deteriorating affordability of servicing investment properties makes residential property investors more vulnerable to risks such as loss of income, interest rate increases, vacancies or rent reductions, and therefore increases their probability of default,” adds Truijens.

Truijens was speaking on Moody’s just released sector-in-depth report on Australian RMBS entitled, “Record Low Rental Yields Increase Risks for Residential Property Investors.”

According to the report, deteriorating affordability also reduces investors’ flexibility around refinancing or restructuring their mortgage loan terms, giving them less options should they experience hardship.

The decline in rental yields has increased the level of ‘cashflow’ losses suffered by residential property investors over the past three years and made investors dependent on greater levels of house price appreciation to cover their losses.

And a greater dependency on house price appreciation makes residential property investing, and in turn, investment loans more risky.

In Moody’s view, the performance of residential property investment loans will deteriorate through 2016 and 2017.

Investment loans originated in 2014 and 2015 – at the peak of the recent house price cycle – will be behind this deterioration.

Furthermore, Moody’s does not expect to see any major improvement in the cost of servicing residential property investment loans in the near term.

The negative impact of low rental yields and the deteriorating affordability of servicing property investments will be most evident in RMBS issued in 2016 and 2017.

Australian RMBS portfolios are typically made up of loans that are one to two years seasoned and so the bulk of the 2014 and 2015 investor loans to be securitised will be found in 2016 and 2017 vintage RMBS.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.