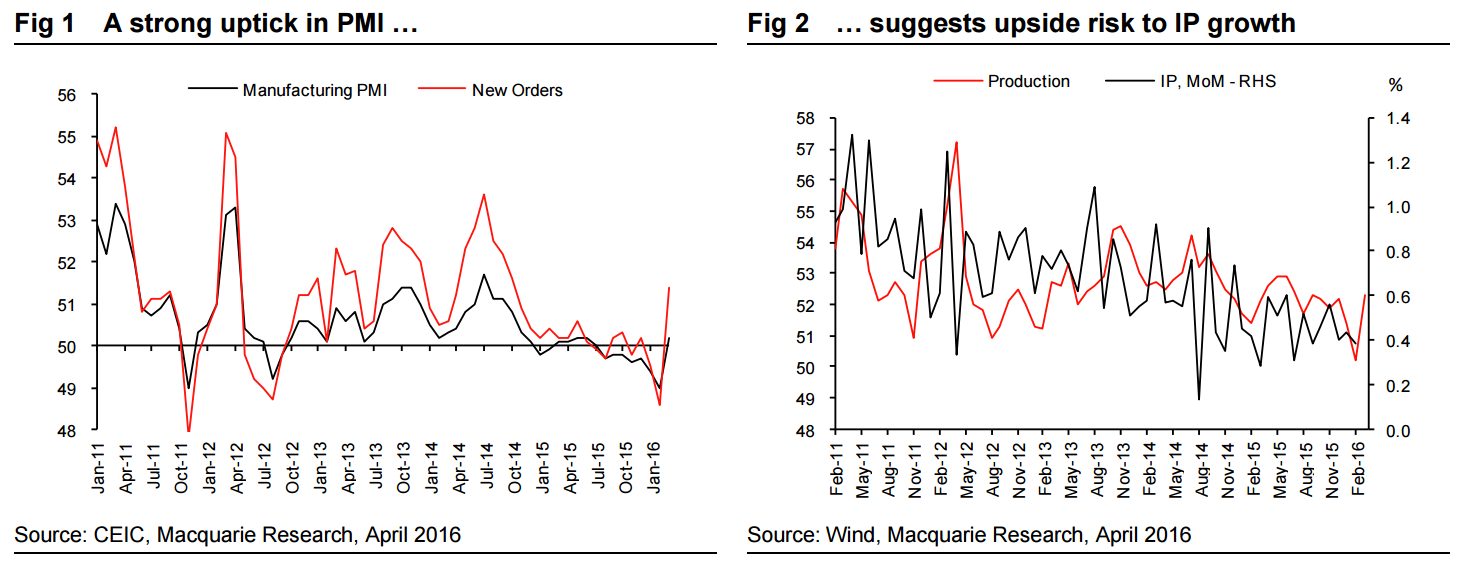

The official and Caixin Chinese PMIs announced last Friday both significantly beat consensus, and the former went back above 50 for the first time since last July. As the first data point for economic growth in March, the strong PMI readings reinforce the recent positive sentiment for metals, particularly bulk commodities, and reinforce the feedback we have been getting through our recent steel and copper surveys. Overall we continue to believe that Beijing’s efforts to support growth and, particularly, the property sector will result in reasonably strong sales of commodity containing goods. We still have doubts as to the sustainability of any underlying demand push, but for the ferrous value chain the sequential apparent demand gains continue to surprise many.

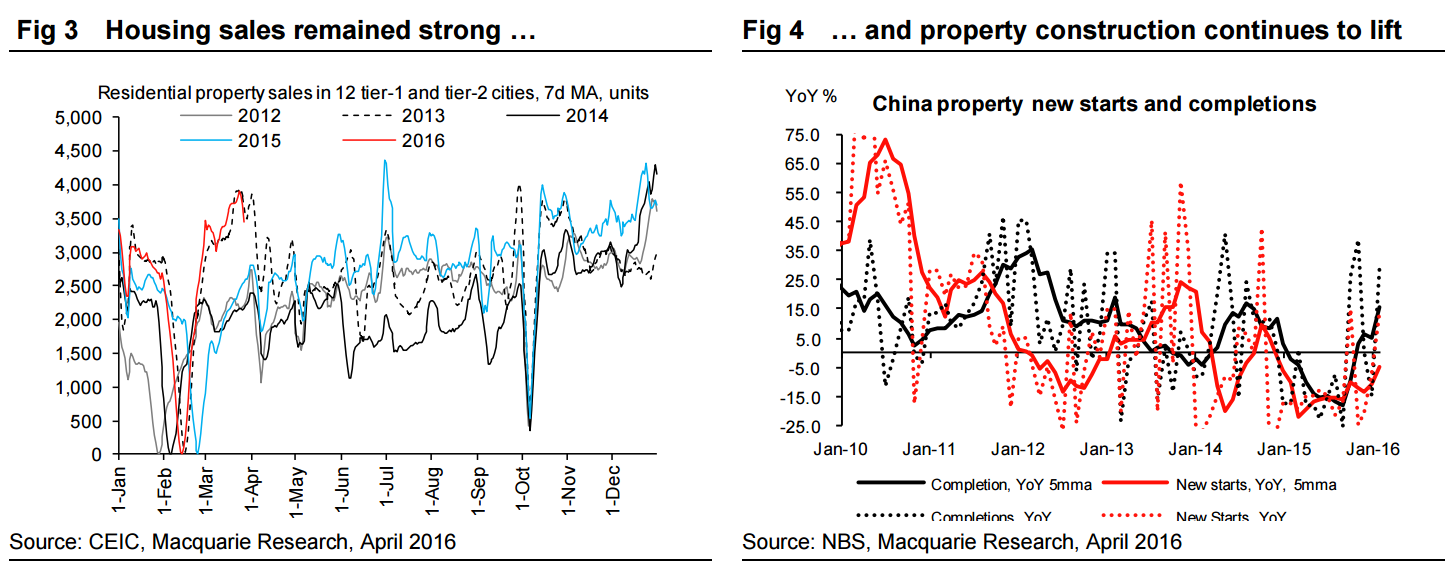

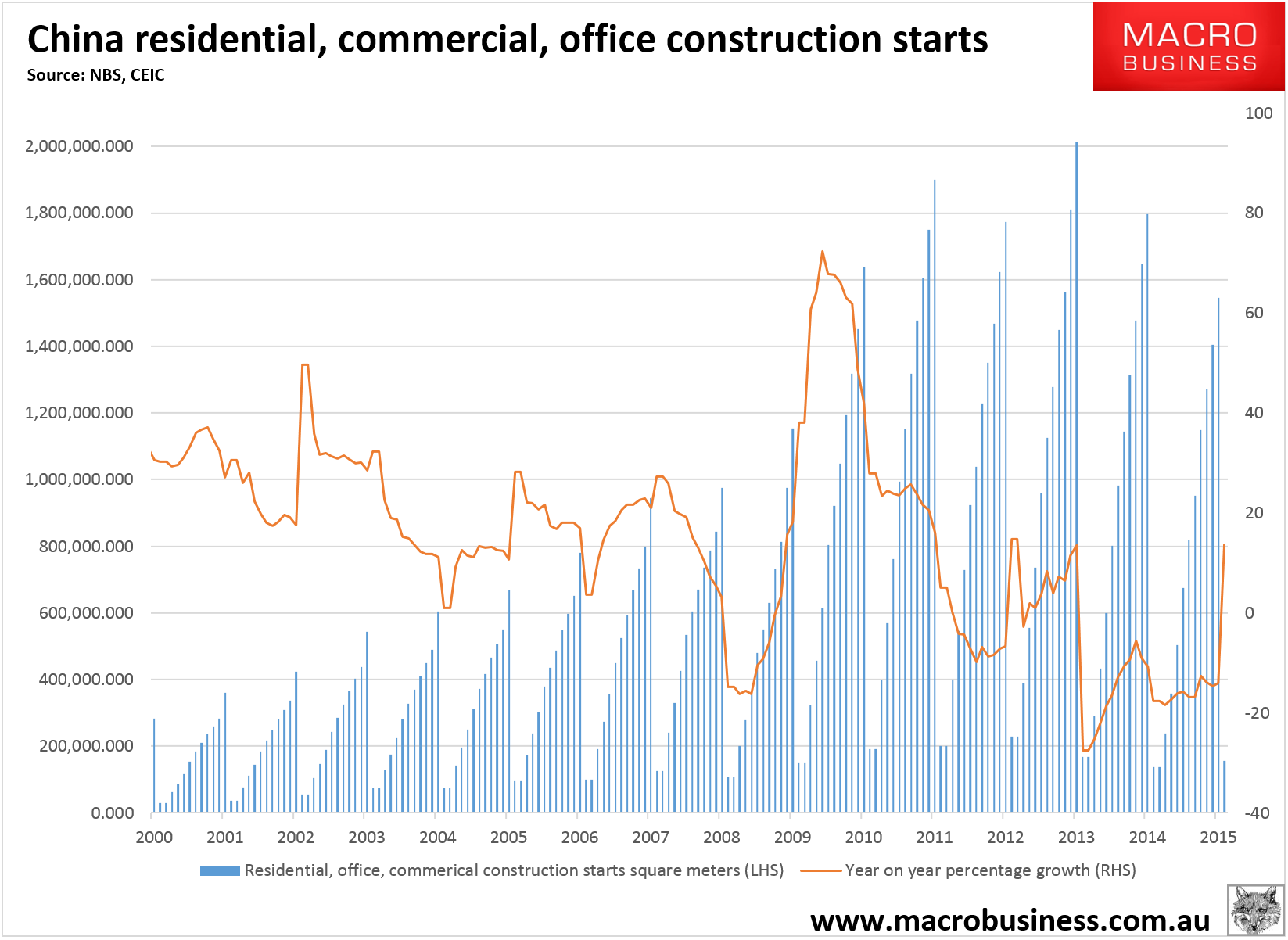

In the meantime, property sales remain buoyant. The daily sales in 12 tier-1 and tier-2 cities that we track were still in line with the peak level seen in 2013 and were 72% higher than the same period in March 2015 (the first 25 days). While Shanghai and Shenzhen have recently introduced measures to cool speculative price increases, we believe the turnaround of property investment in the past couple of months still looks to be on a solid footing. While monthly construction data in China has always been volatile, the five-month moving averages for both new starts and completions have both been showing a clear improvement (Fig 4). Upside risks are clearly increasing to our forecast for a -8% contraction in steel consumed in residential real estate construction for this year.

Looking back over history, the current cycle also looks increasingly like the upturn in mid-2012 to mid-2013, when the strength of heavy industrial sectors was evidenced by a pick-up of power generation growth from zero in June 2012 to 13.4% YoY in August 2013, and there has also been a surge in housing prices in both 1Q13 and 1Q16. Admittedly, the cyclical upturn in 2012/13 would probably prove stronger than seen this time, but if the duration of the last upturn is anything to go by then we will quite likely see growth momentum strengthen further over the next couple of months.

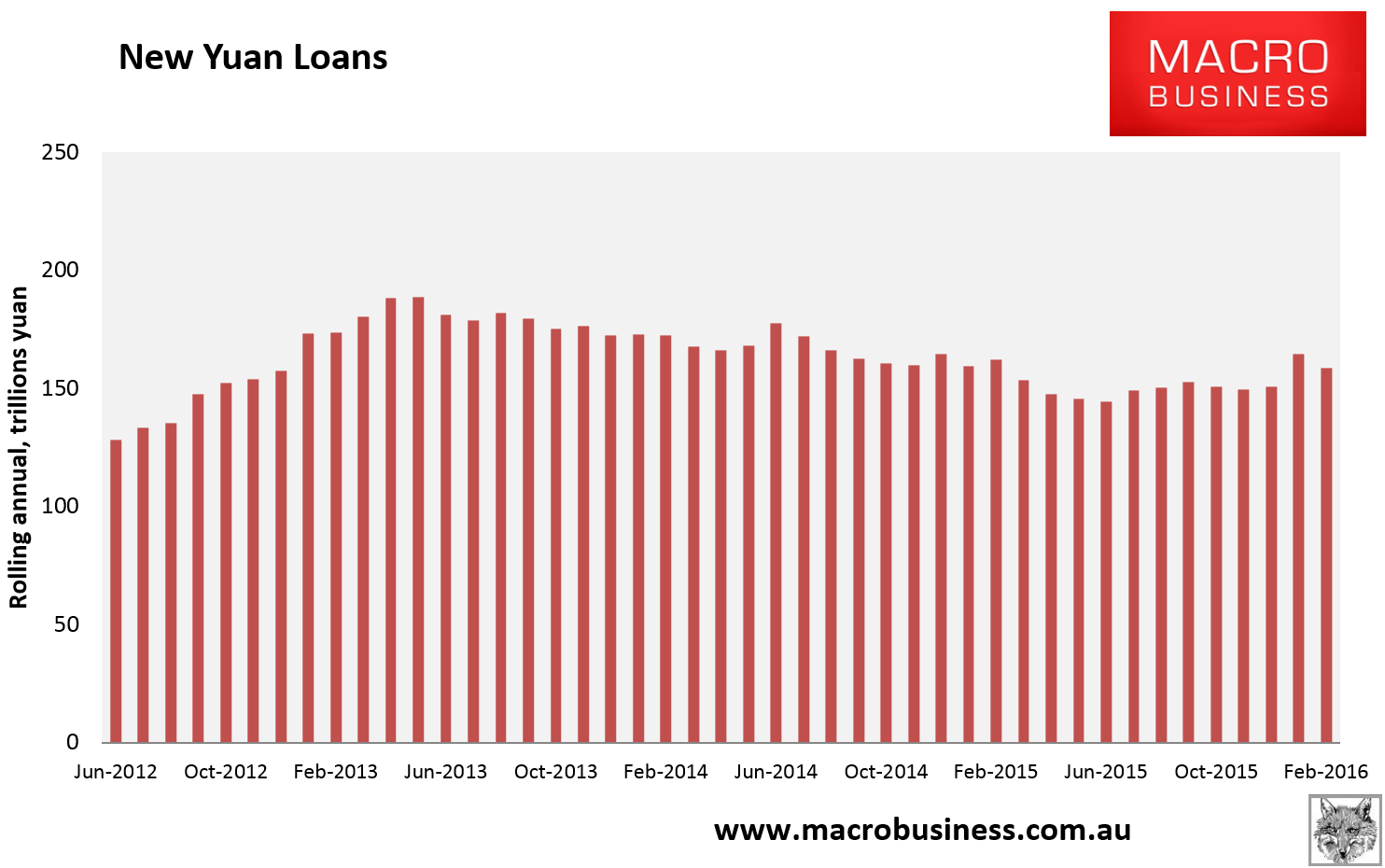

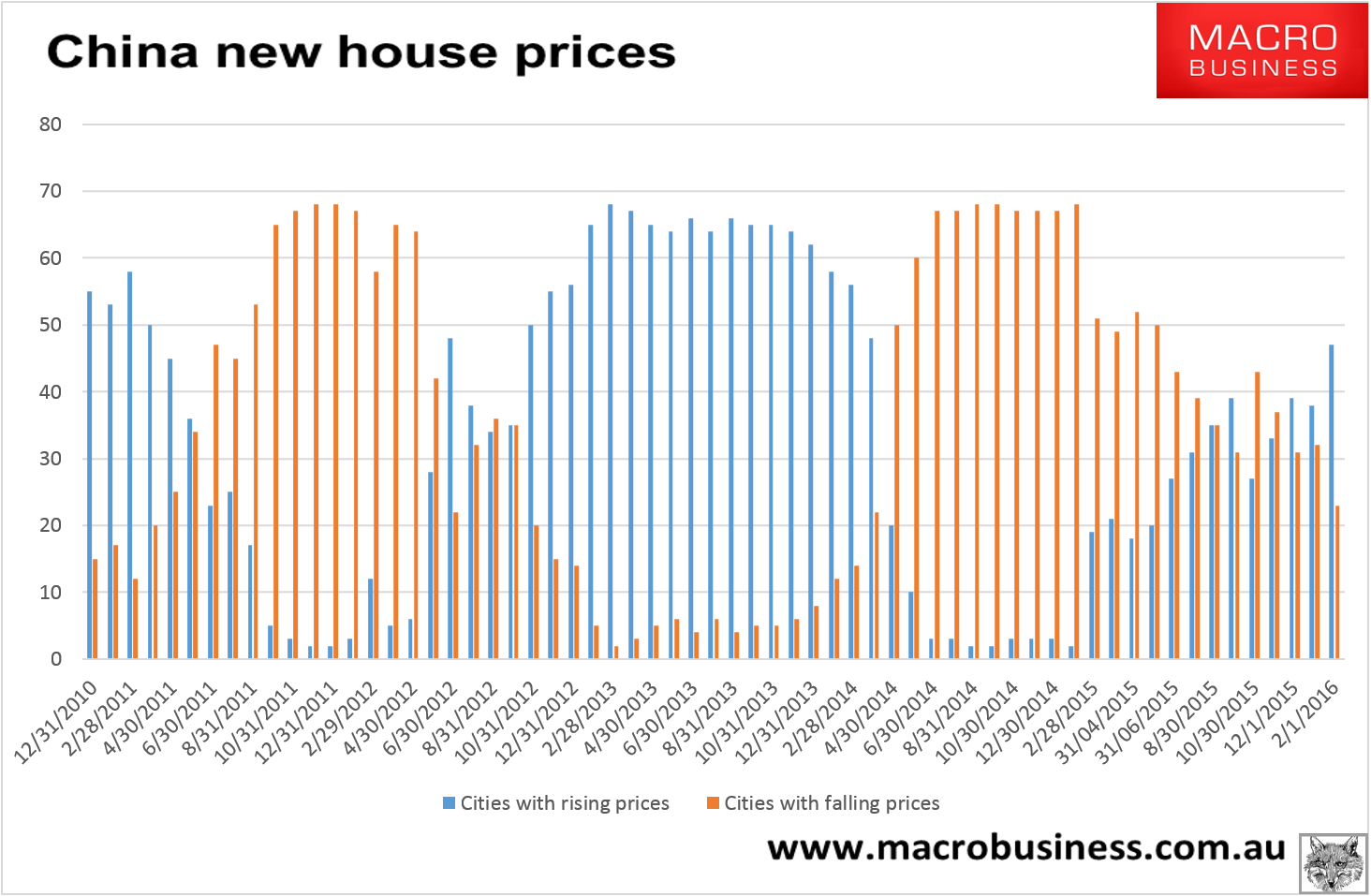

That’s a reasonable reading of events. We are not going to get as far as 2012/13. Back then we had full blown credit acceleration:

And house price recovery:

Advertisement

Versus flat lined credit today and a bifurcated price recovery. Moreover, 2012/13 was still enjoying the 2009 stimulus tailwind:

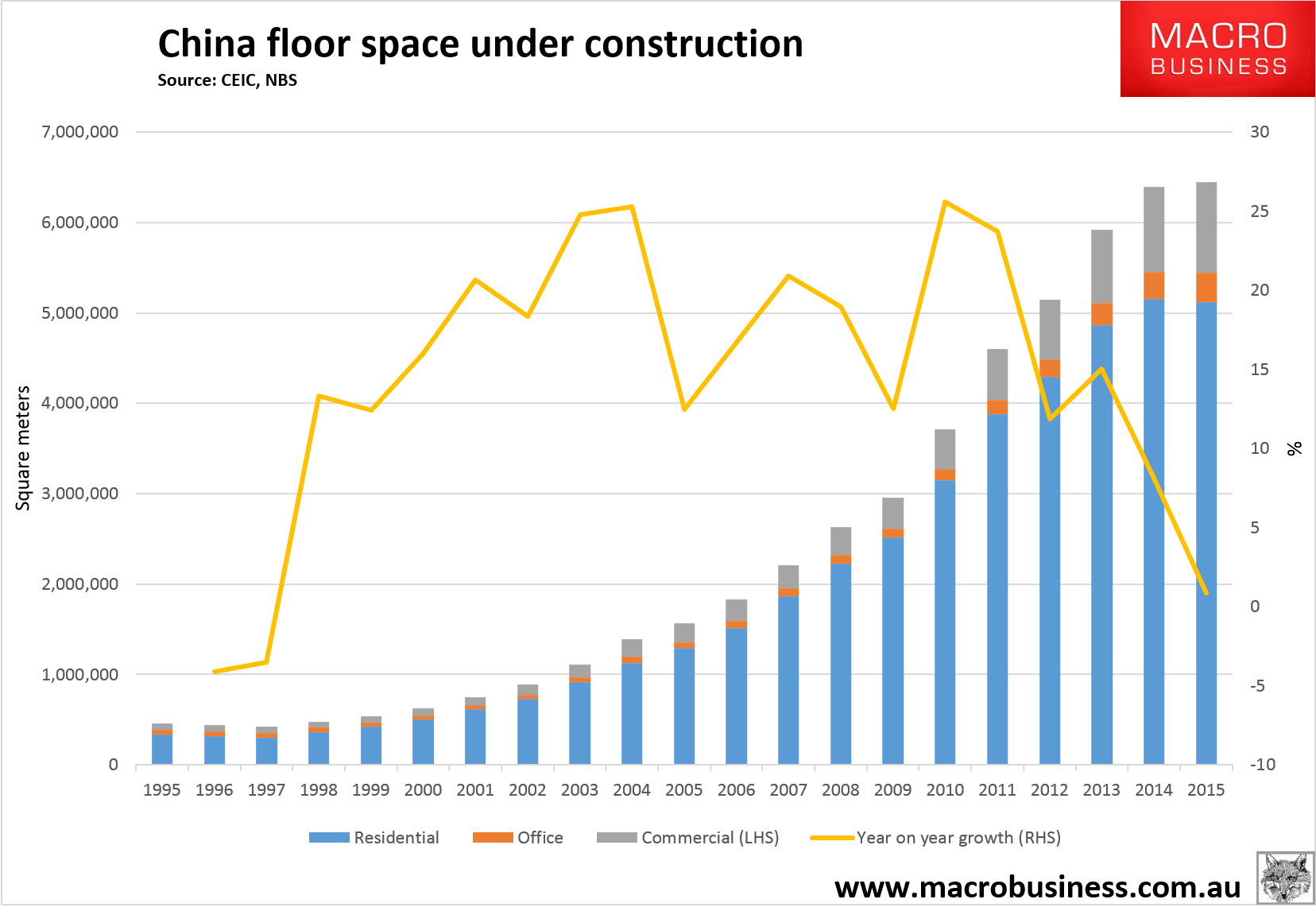

And even starts were yet to peak:

Advertisement

I expect we’ll see a couple of stable quarters in China then slide away again in H2, maybe even earlier if first tier city house prices hit the wall.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.