The Aussie dollar remains on a tear hitting a new rebound high of $77.58 last night:

At 13.5% this is now easily the largest bear market rally of the great fall. Let’s take a look at the MB ‘five drivers’ model and see what it tells us.

The five drivers are:

- global and Australian growth (or, more recently, Chinese growth and Australia’s terms of trade);

- interest rate differentials;

- investor sentiment and technicals; and

- the US dollar.

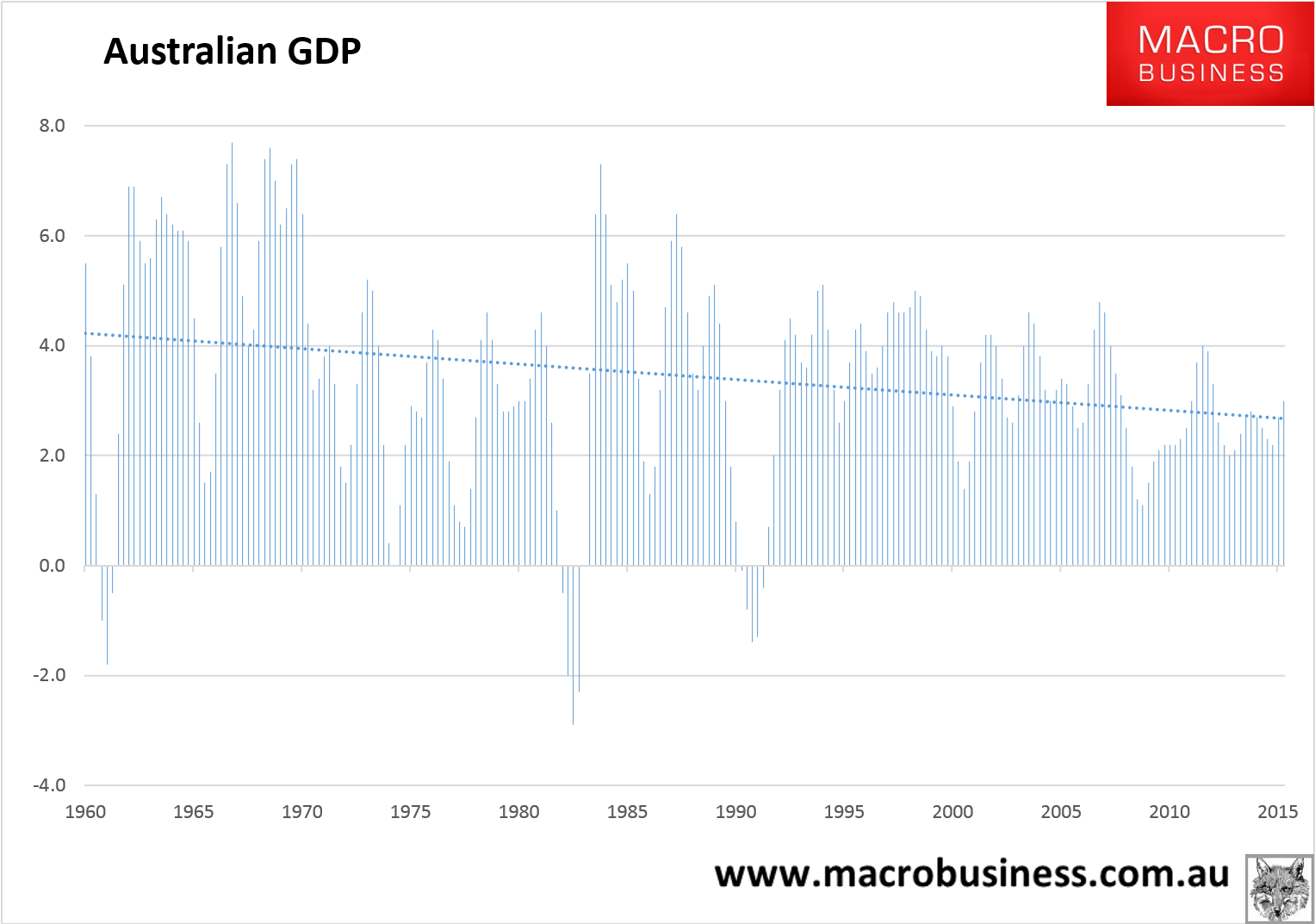

For the first, Australian growth has been relatively strong in GDP terms over the past year, certainly in terms of relative performance with other developed economies:

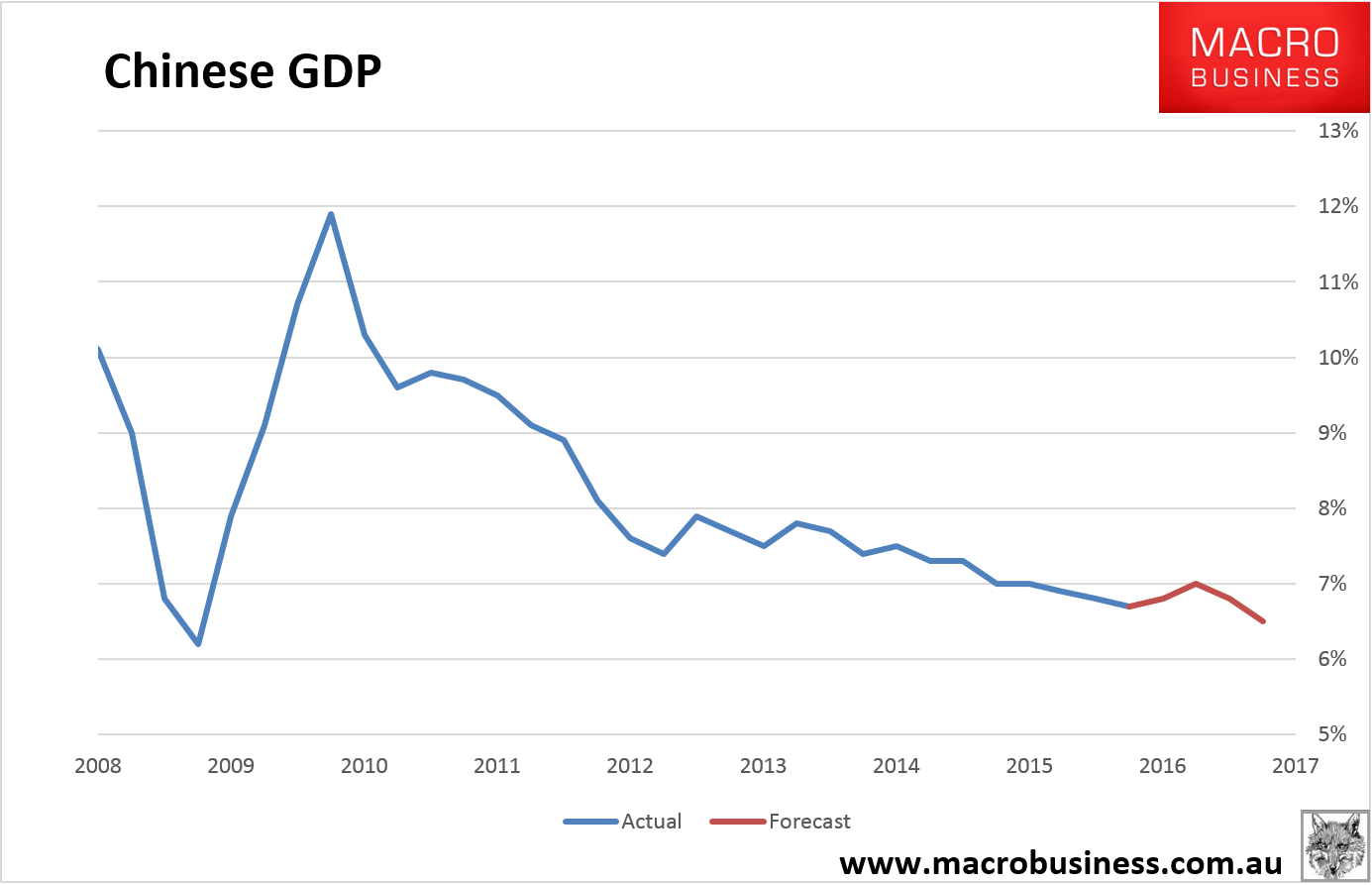

As well, Chinese growth is poised to rebound on stimulus over the next few quarters:

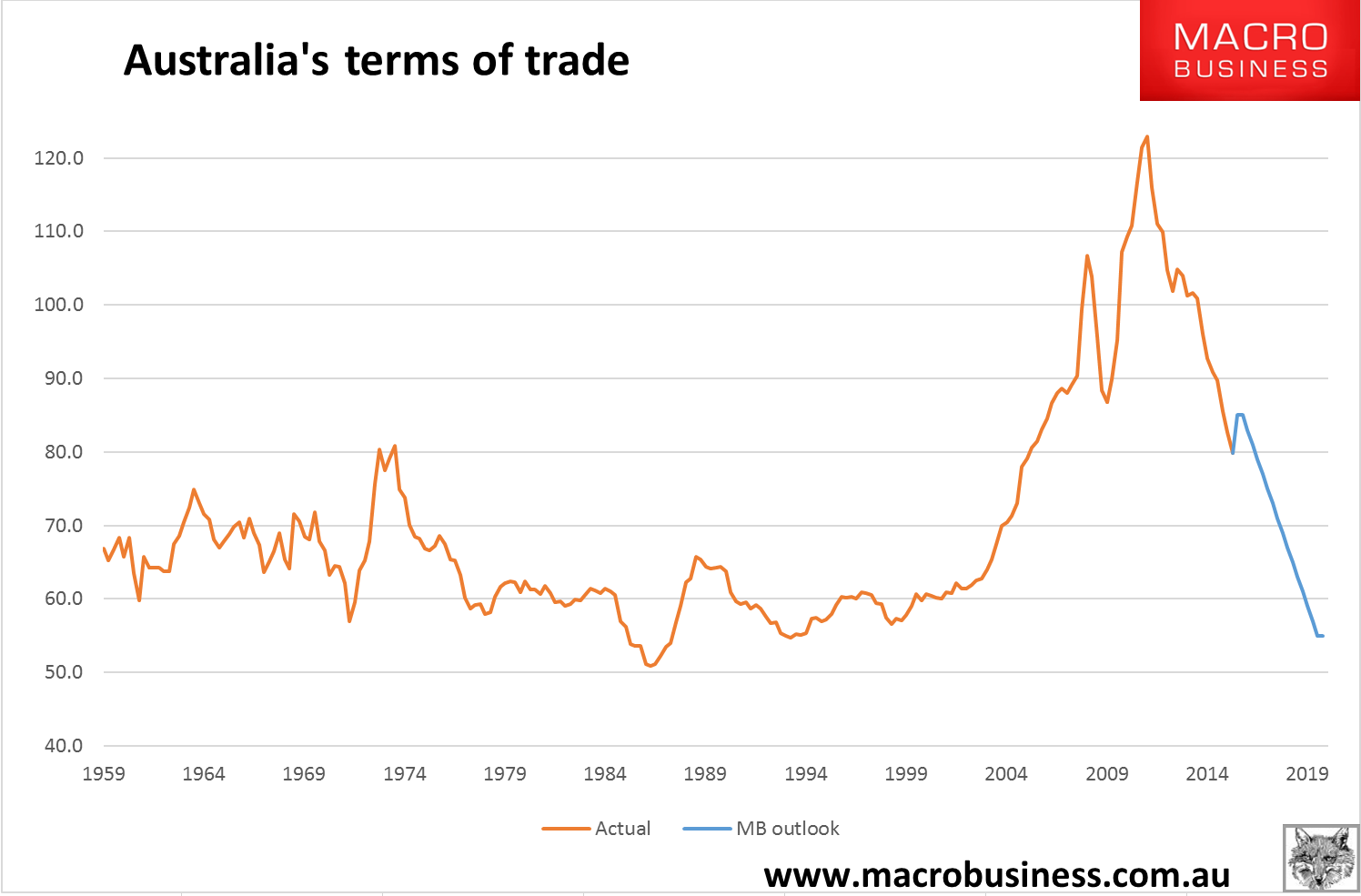

And this has temporarily lifted Australia’s terms of trade by a solid 6% or so from its December lows:

However, we do not expect this to last:

- Australia’s income shock will return in H2 as the Chinese growth pulse fades and with it Australia’s terms of trade as iron ore rolls;

- house prices are stalling and falling on macroprudential tightening also slowing cyclical sector activity;

- a mid-year election is exacerbating that;

- the triple-header capex cliff in mining, cars and residential construction begins in H2;

- a firmer dollar to date this year will stall the non-mining tradable recovery.

None of these is fatal in and of itself but together we see them pushing growth back towards ‘stall speed’ in H2, low enough to lift unemployment again and erase Australia’s growth advantage.

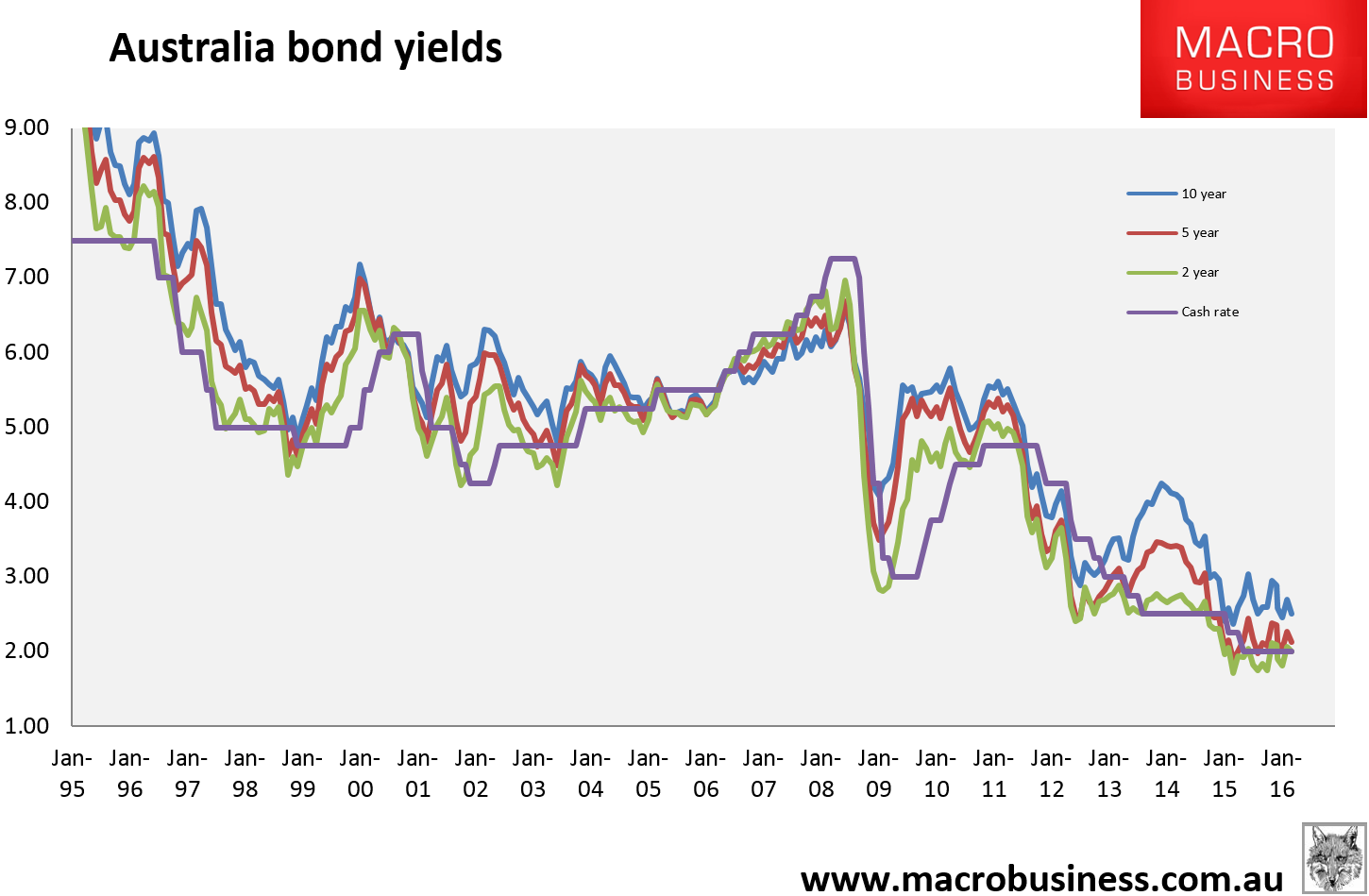

For driver two, local interest rates have now been paused for twelve months and many prognosticators see the cash rate at the bottom. We do not and expect further rate cuts in the cycle, likely this year as the above takes its course. For the time being local bond prices have stabilised around the cash rate of 2%:

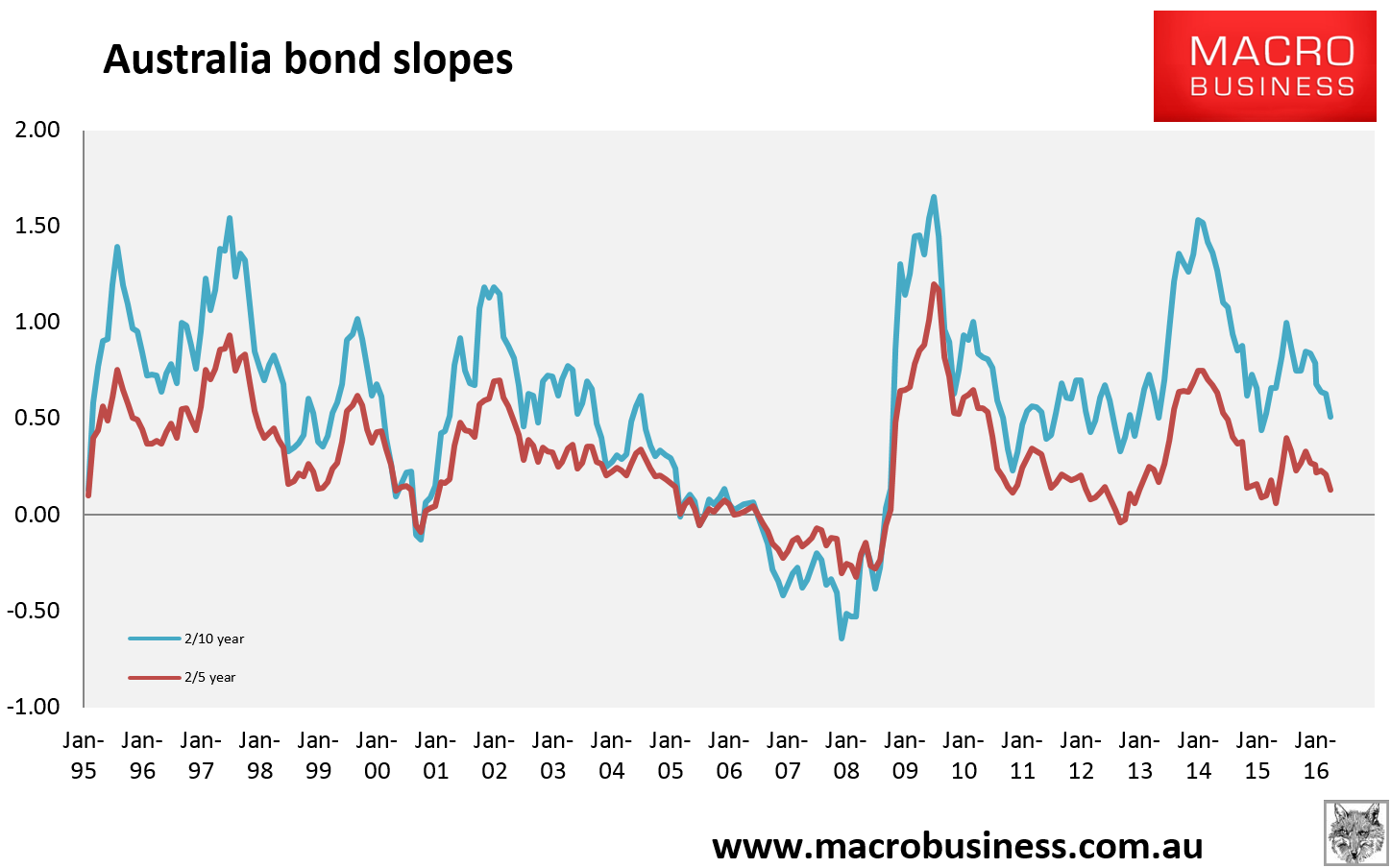

However, the yield curve or slope is clearly signaling a brewing problem with growth with the 2/10 yield flattening to its shallowest in a year and the 2/5 yield pressing towards inversion:

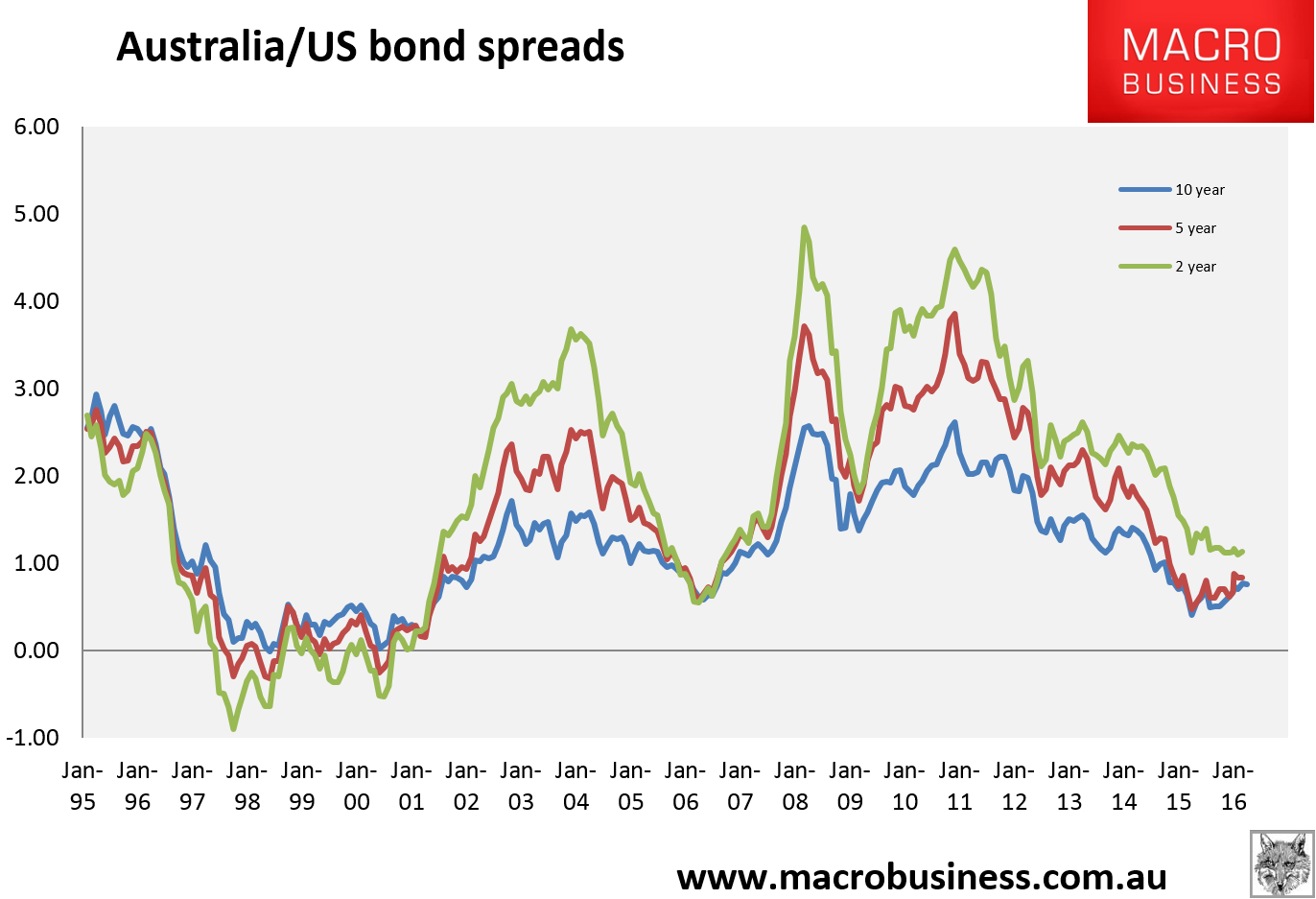

Both of these trends are signaling a resumption of the Australian easing cycle before long. Moreover, compared with the US where the Fed has slowed but not stopped its tightening, the spread has barely lifted at the short end of the curve despite Australia’s recent good run:

There has been a pretty decent widening at the long end of the curve, however, suggesting that markets still favour higher rates for Australia over the stretch.

Drivers three, technicals, still looks moderately bullish for the Aussie:

The declining channel in place since 2013 has room to the upside but 80 cents is the downtrend line and looms as very heavy resistance. If we can get that high and through it then it’s potentially a new bull market for the currency but I am doubtful to say the least.

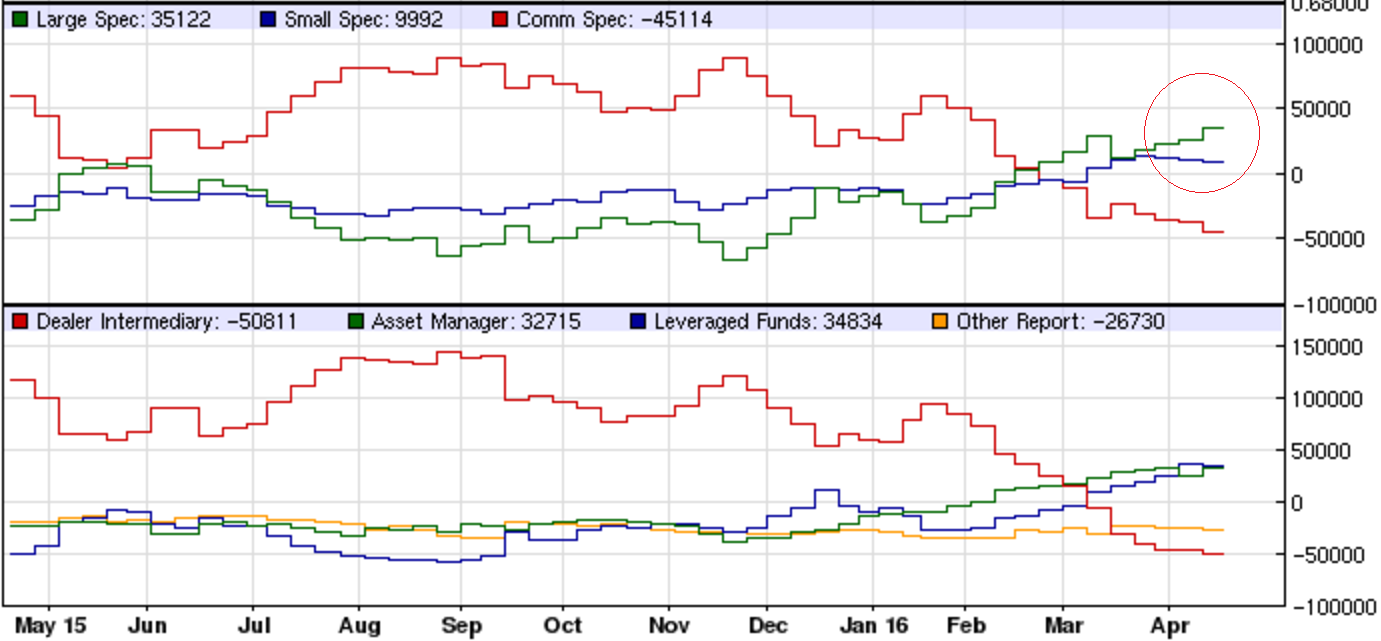

Driver four, sentiment, has the market positioned moderately long with the Commitment of Traders report at +36k contracts:

There is room for this go higher. In April 2013 when the Aussie was still riding high above parity it was common for the market to be long nearly 100k contracts. However that was exceptional and a better comparison is the bear market rally of H1 2014 which never saw contracts get above +30k, so we are already pretty long in context here which I would mark this down as modestly bearish.

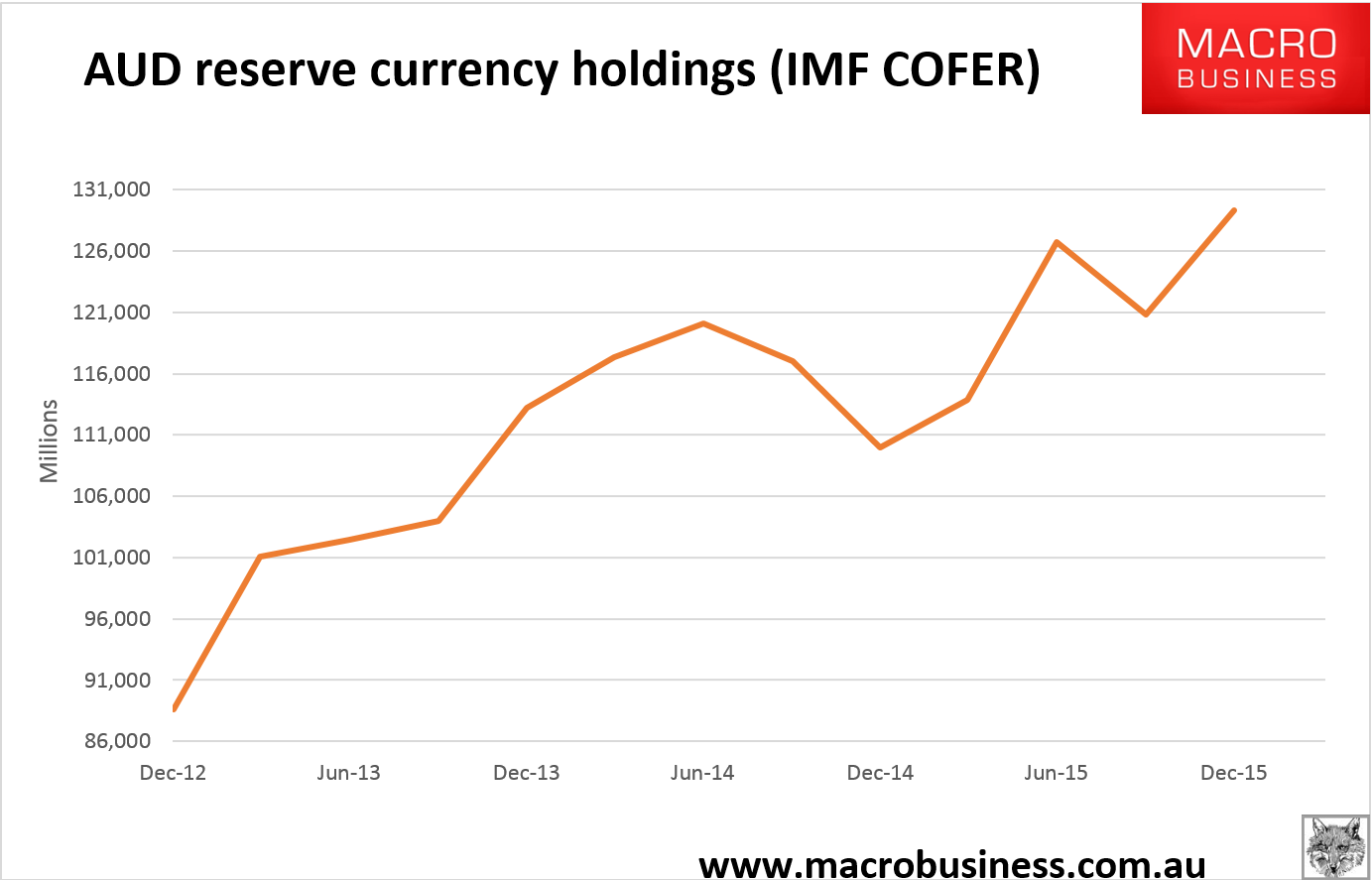

There is one other possible positive for sentiment. We know that central banks have been adding Aussie to their reserve portfolios for a few years. That has been a significant real support to higher valuations and general market sentiment around the currency. The IMF’s Currency Composition of Official Foreign Exchange Reserves (COFER) report is six months behind but up until Q4 2015 it showed official buying still trickling in:

I don’t know why they keep coming despite the large losses for much of it but hey!

The fifth driver, the valuation of the US dollar, has perhaps been the key change this year. Following the Mining GFC volatility of the first quarter, the Fed has roughly halved the pace of its intended tightening. That has taken a lot of pressure off the US dollar:

The chart pattern remains modestly bullish with a falling wedge within a large ascending triangle but for all of that the dollar also clearly wants to test the downside. I would not be surprised to see it break supports in 93 cent area and test lower resistance. Even so, the US economy is still plodding along with enough vigor for another rate hike this year, with an outside chance of two.

Further, when we compare the US outlook with the other large reserve currencies in Japan, Europe and Britain their weakness is very obvious with more easing likely. However, this simple pattern is complicated now by the specter of “quantitative failure” and the possibility that their extraordinary monetary tools are exhausted hence those currencies have been rising. This is premature. Japan especially has shown a willingness to innovate and its next steps will be “helicopter money” whether buying assets like stocks, giving away retail vouchers or to just fund government directly. While none of these is QE they most certainly are currency debasement!

In Europe, we have not only weak growth and the prospect of similar monetary innovation following Japan (though the Bundesbank will not be happy) but we also have severe political strains emerging around the guerrilla war with ISIS and its role in promoting anti-euro political parties in Britain, France and everywhere else to boot. This risk of a major country exit is real and any risk-adjusted valuation of the euro is much lower than its face value.

In short, even if the US dollar falls for while, I can’t see it getting far before reversing upwards given it is still the only major reserve currency worth owning. At least until the Fed embarks on another round of its own QE and that will take virtually a cycle-ending shock first.

The upshot of the five drivers is that the cyclical conditions for Australian dollar strength are obvious but already beginning to ebb while the structural factors remain weak.

80 cents could loom as a short term target given the downtrend line but even so most of the rally is probably already done. When it does roll over MB still sees the currency falling a long way from here. Our initial target of 60 cents for 2016 was wound up to 66 cents if the Fed slowed obviously and that has happened so we’ll stick with that. Next year we see it continuing to fall as Australia’s AAA is lost, it’s terms of trade continue to fall and, as monetary easing steadily loses traction in the housing market. Our cycle low outlook of 45 cents is still in place when the next global shock arrives.