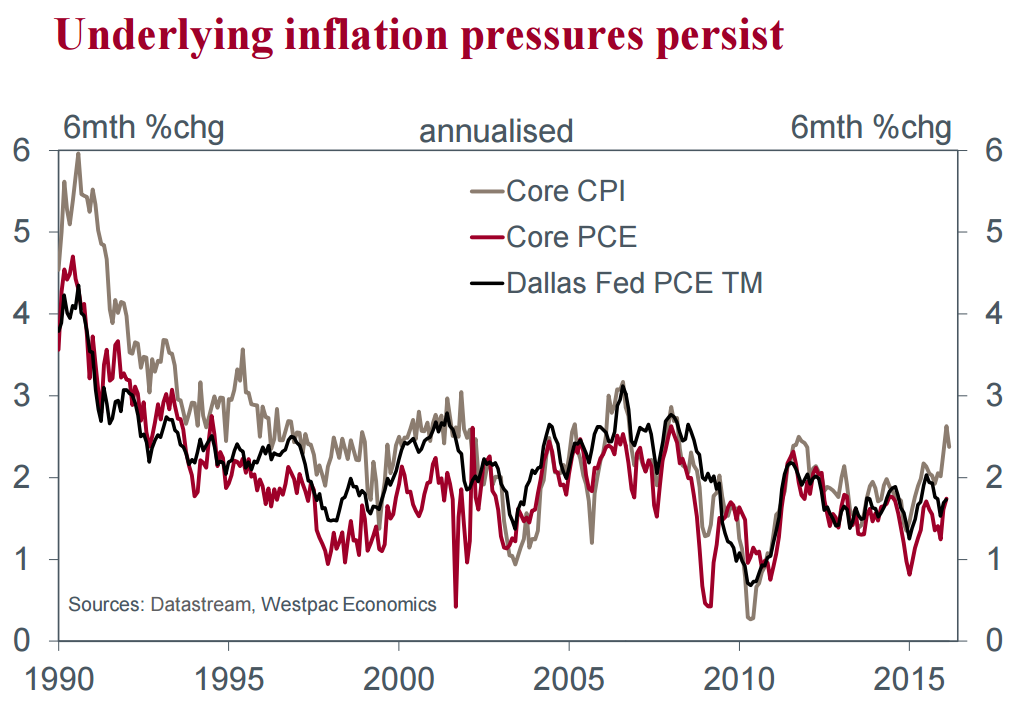

In recent months, core CPI inflation has shown renewed strength. Despite a softer than expected 0.1% headline outcome in March, core inflation remained above the FOMC’s medium-term target of 2%yr, coming in at 2.2%yr, or 2.4% in six-month annualised terms. Only available to February, the PCE measure is softer at 1.7%yr, but is still relatively near to target and is also in a clear uptrend.

Despite the ‘strength’ in these core measures, recent guidance on current and expected inflation dynamics from the FOMC has been decidedly noncommittal.

From the March meeting minutes: “Some participants saw the [recent] increase as consistent with a firming trend in inflation. Some others, however, expressed the view that the increase was unlikely to be sustained, in part because it appeared to reflect, to an appreciable degree, increases in prices that had been relatively volatile in the past.” Also, with respect to the risks, more members of the Committee continue to believe risks are more to the downside than upside.

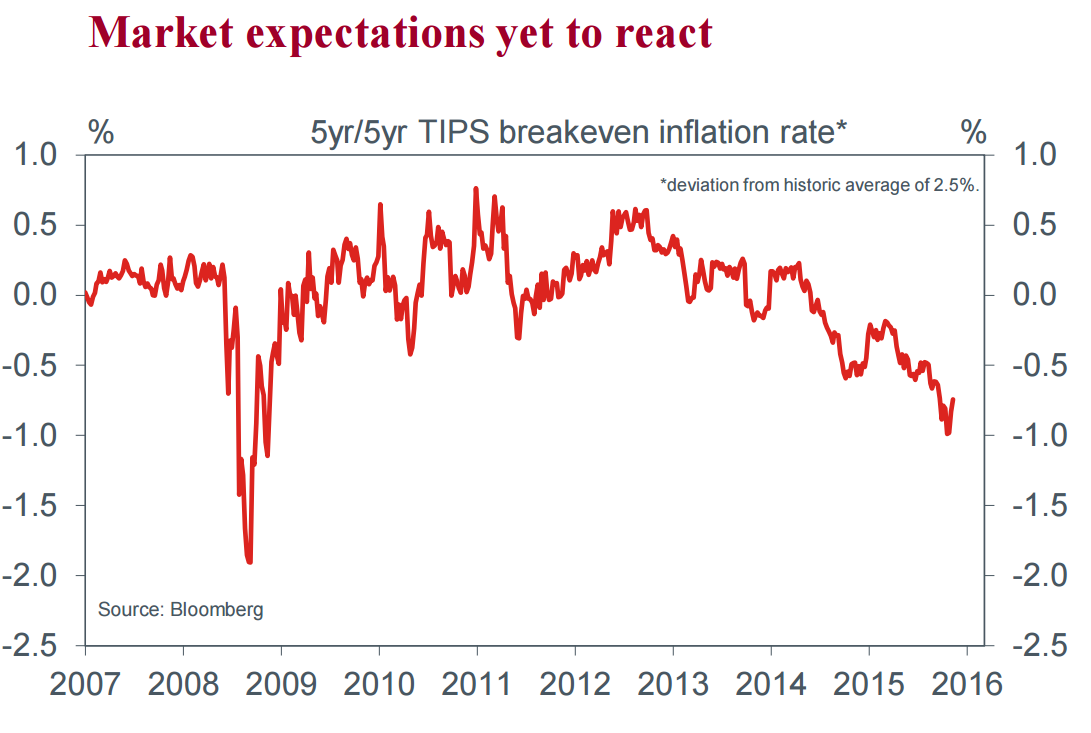

Given the near-constant disappointments in this recovery for inflation and the prolonged period of energy deflation and import price disinflation, doubts over inflation amongst FOMC members are understandable. This view also corresponds to the persistent, very low level of market inflation expectations which, unmoved by the core inflation gains above, continue to trend down.

For both the FOMC members’ expectations and those of the market, the persistence and breadth of underlying price pressures are important. To us, there is evidence on both fronts to support a constructive view of inflation for policy. (All subsequent inflation figures are six-month annualised rates).

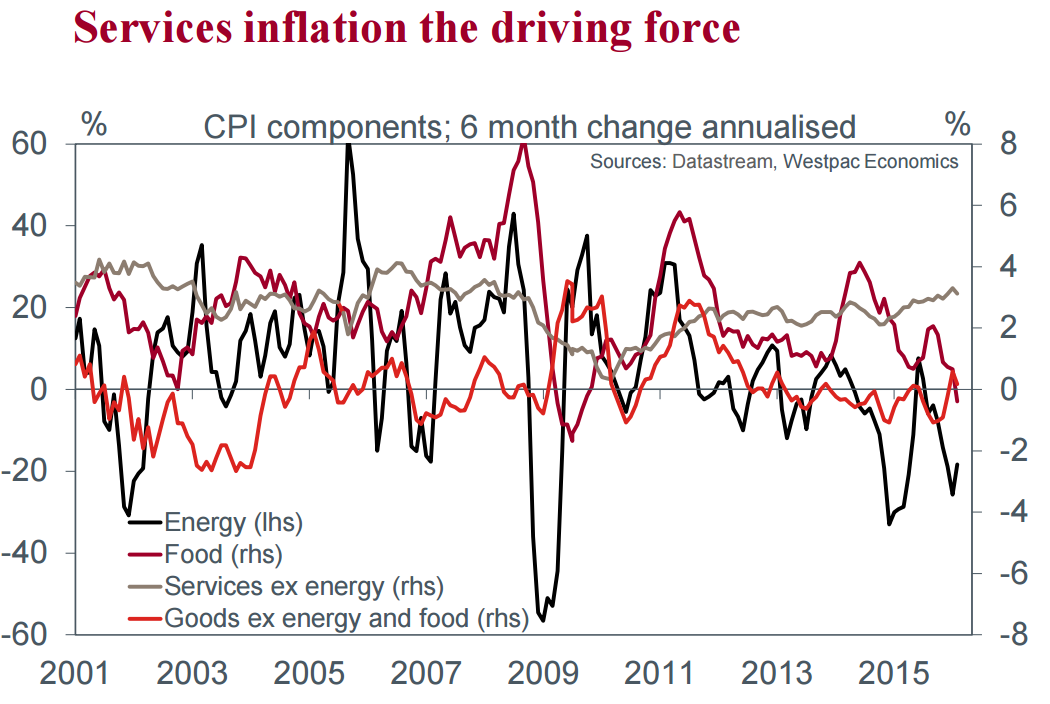

First, it is important to note that the underlying inflation trend has persisted for six months, if not longer. Services inflation has averaged above 3% over that period; and this follows a consistent uptrend from a prior low of 2.1% in November 2014.

Key to this trend has been the shelter component of the CPI, namely rents. Reduced home ownership; increased large investor development; and the (typically) higher price of new-build apartments (which are an increasing share of the rental stock) has seen the average rent paid by a tenant consistently rise by 3% or more since mid-2014. Bolstering the headline impact mechanically, this strength has also fed through into imputed rents for owner occupiers (note this is an economic assumption, not an actual measured cost for home owners).

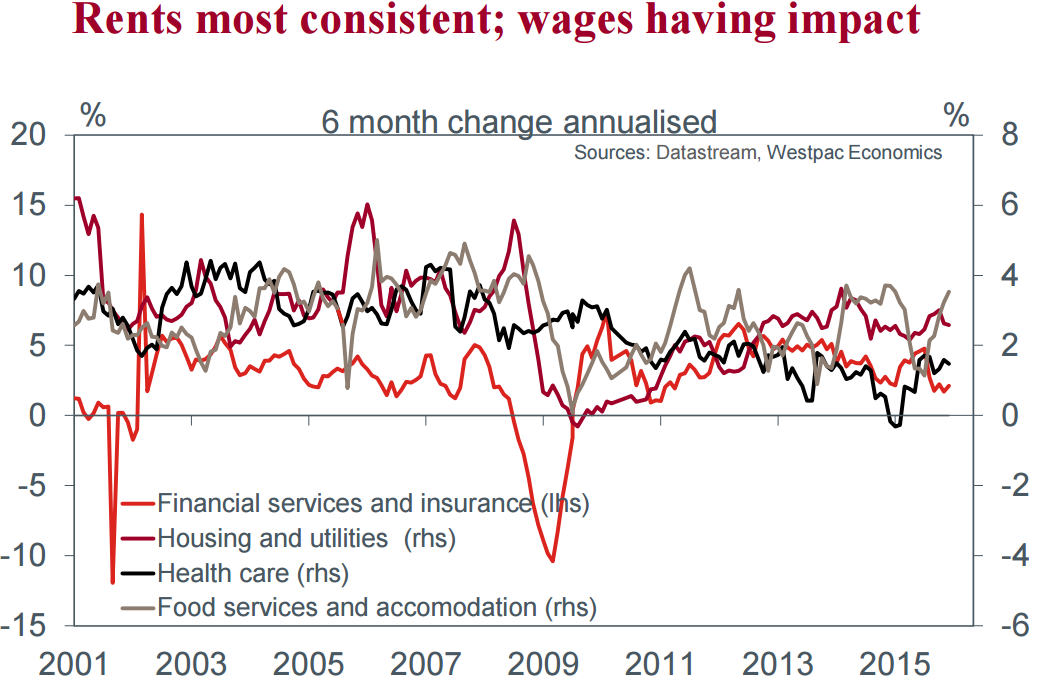

While rent inflation has ebbed a little of late, other sectors have experienced strengthening inflation, broadening the breadth of inflation pressures. Food services & accommodation has risen from a June 2015 low of 1.3% to 4.0% in February. And health care (which has a similar PCE weight to housing and is more than twice as large as food & accommodation) is up from 0.7% in mid-2015 to 1.2% in February. Both sectors have been impacted by minimum wage gains across the country and this will likely continue.

There is therefore evidence of solid price pressures in a number of key (typically stable) categories of inflation. Through 2016, to this will likely be added a basing in energy prices and the USD’s disinflationary impact. The inflation impulse should then remain strong enough to support further rate hikes during 2016; however, these decisions will continue to be triggered by available activity data and perceived risks, not inflation by itself.

Westpac has been too hawkish on the US for quite a while but I agree that there is enough going on here for the Fed to hike once more this year and twice if the first rise (second in the cycle) doesn’t destroy the global economy.

It’s odds on that a second hike this year (third in the cycle) will.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.