Monetary policy is all about risk management. With downside risks to the global growth outlook persisting, question marks over the trajectory of domestic growth in the second half of 2016 due to the peak in housing activity and a 10 per cent appreciation in the Aussie dollar trade-weighted index since late last year, it is getting harder for the RBA to withstand downside surprises on inflation.

The burden on activity data to deliver growth which is consistent with above trend (or even trend) growth is now larger in order to return inflation to target, and presumably requires a more accommodative setting of monetary policy to achieve this. With core inflation now at 1.55 per cent, the real cash rate in Australia is closer to +0.50 per cent. This is a departure from recent years, where the RBA has delivered monetary conditions consistent with a real cash rate of 0.0%.

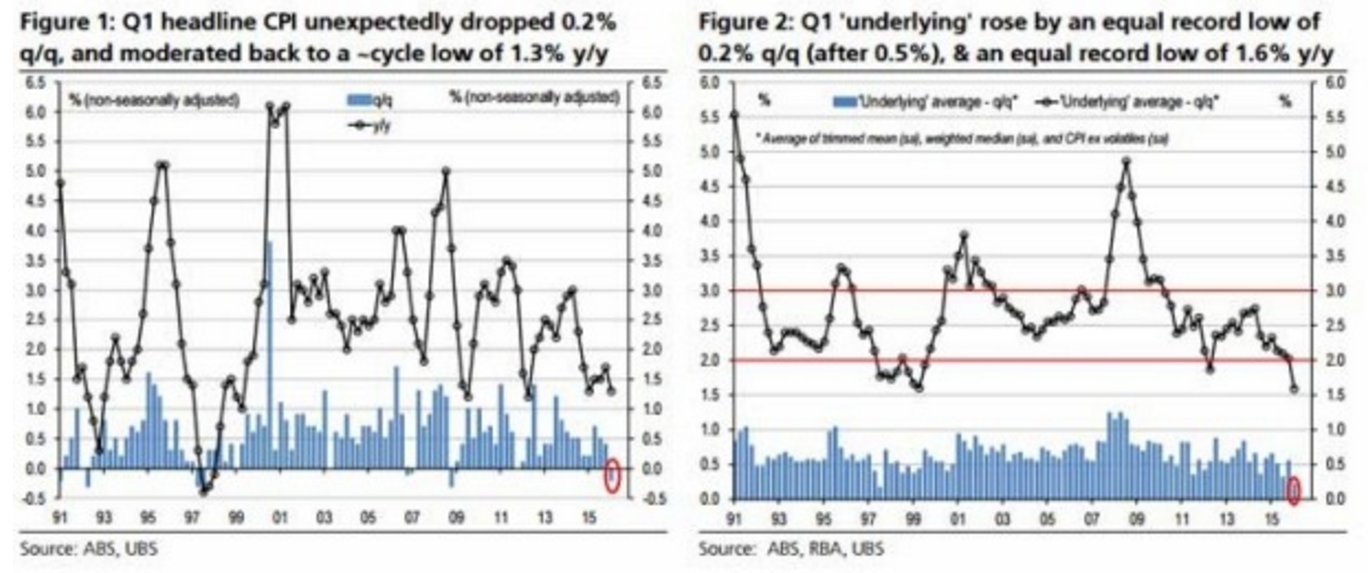

There is enough “signal” (rather than noise) in the last couple of inflation prints to convince the RBA that the disinflationary trend is genuine, and moreover, has not stabilised. The trend in core inflation is clearly lower – and while this is no different to that seen in most developed economies – the RBA has already observed that the soft 3Q15 core result was more signal than noise.

Of course, like all decisions, this one is not clear cut, Auld concedes.

“It is possible that the RBA points to GDP growth at 3 per cent-plus annualised in 2H15, an unemployment rate of 5.7 per cent and stability in the price components of business surveys as factors which perhaps permits it to look through the downward surprise.”

The RBA could also argue that today’s inflation print represents the “capitulation” of domestic inflation in the face of strong disinflationary global forces, and with commodity prices looking like they have troughed and the currency looking like it will struggle to breach 80 US cents, the inflation story should improve from here, she says.

“But even taking these arguments into account, we still come back to the point that the shift in the balance of risks to both growth and inflation now demands lower rates.”

Westpac says no:

The key observation in the March quarter is the across the board weakness in Australia retail prices highlighted by the first disinflationary CPI headline print in seven years and the lowest six month annualised pace of core inflation in seventeen years. All together this highlights downside risks for our medium term inflation forecasts.

But low inflation, on its own, is not a trigger for a rate cut. Sure, it unlocks the interest rate door for the RBA should it decide it needs to walk through that door as the Bank would not have to wait for another CPI update before doing so. However, it does not mean that the RBA will cut rates! A rate cut is dependent on local economic conditions demanding a rate cut. With unemployment on a new downtrend this is not so at the moment and we suggest that the RBA is waiting to see a new weaker trend in domestic activity and employment before it would embark on such a strategy.

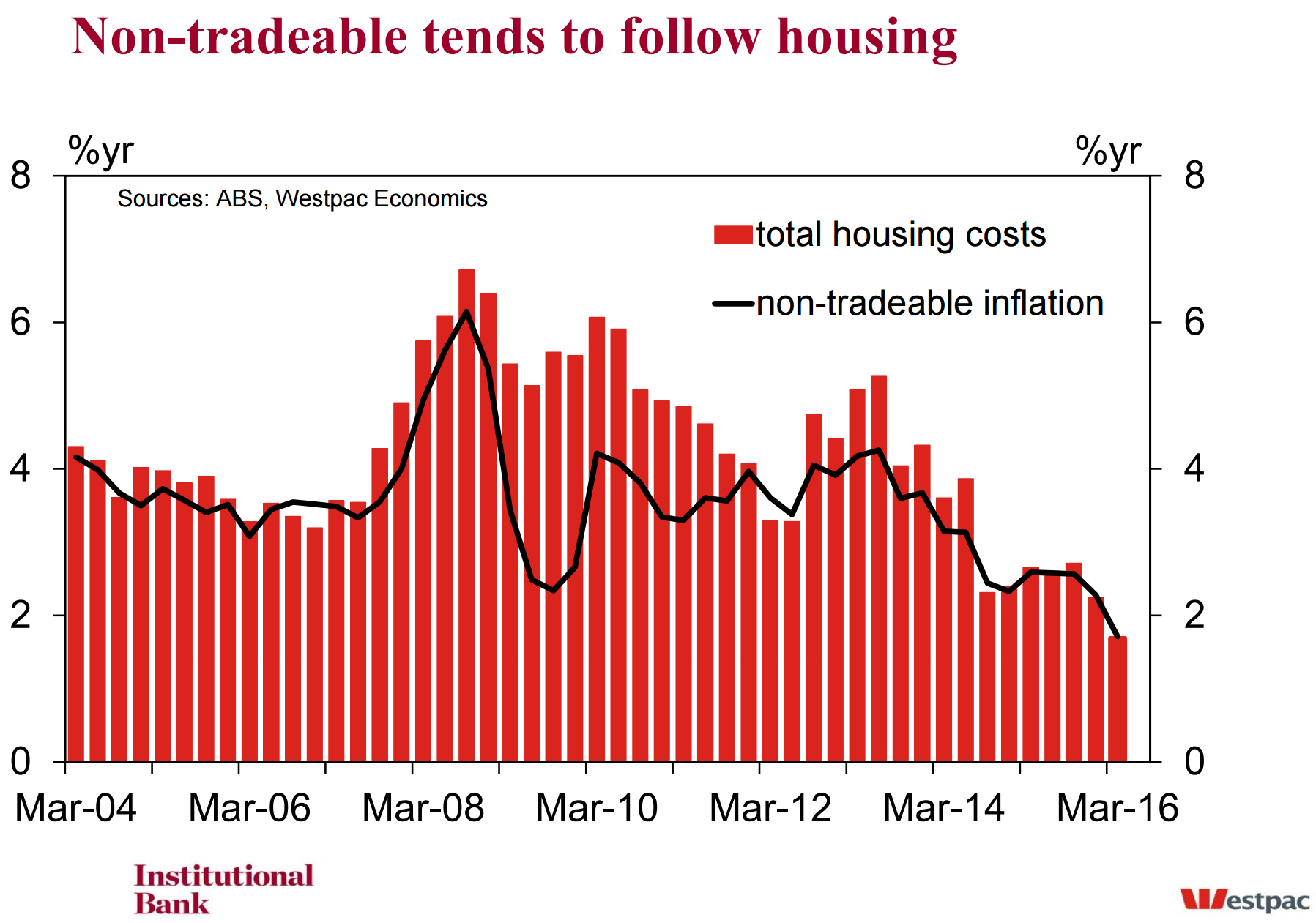

I agree with Westpac that May is out. But that non-tradable inflation downtrend linked to housing is a leading indicator for the weakness that will trigger the RBA. June or July is on.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.