So Macquarie Bank says after the APRA Net Stable Funding Ratio (NSFR) paper:

While APRA expects banks to meet a 100% NSFR target by January 2018, it is not clear what buffers banks will be required to achieve. Given the structure of our funding market, we expect the regulator to give banks time to grow into a reasonable NSFR position (ie. ~105% by 2020). The improved funding position should also help banks to achieve “unquestionably strong” status.

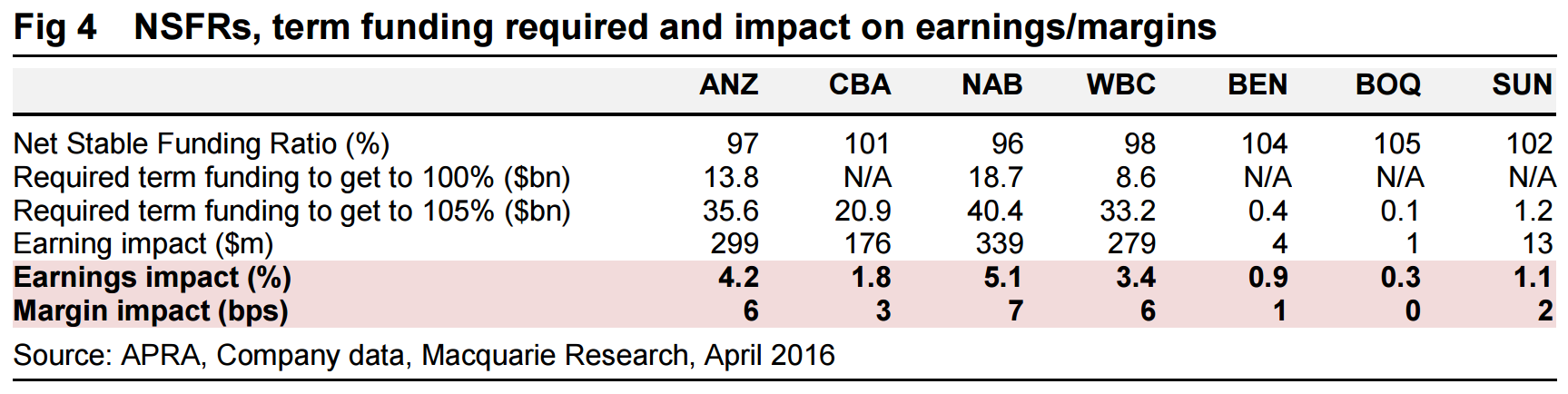

As per the figure below, our analysis highlights that CBA is the only major bank with a NSFR over 100%. NAB appears to have the lowest NSFR. We estimate that the regional banks have NSFRs of over 100% given their balance sheets are skewed to mortgages.

Based on our estimates and assuming no changes in deposit market shares, we estimate that ANZ, NAB and WBC will need to raise an additional $14bn, $19bn and $9bn of term debt, respectively, by 2018. Should all banks target a 105% NSFR by 2020, we estimate $21-40bn of additional term funding required over the next four years, which will take 2-5% off banks’ earnings and 3-7bps of banks’ margins. We note that the regionals are generally better placed to meet the NSFR requirements.

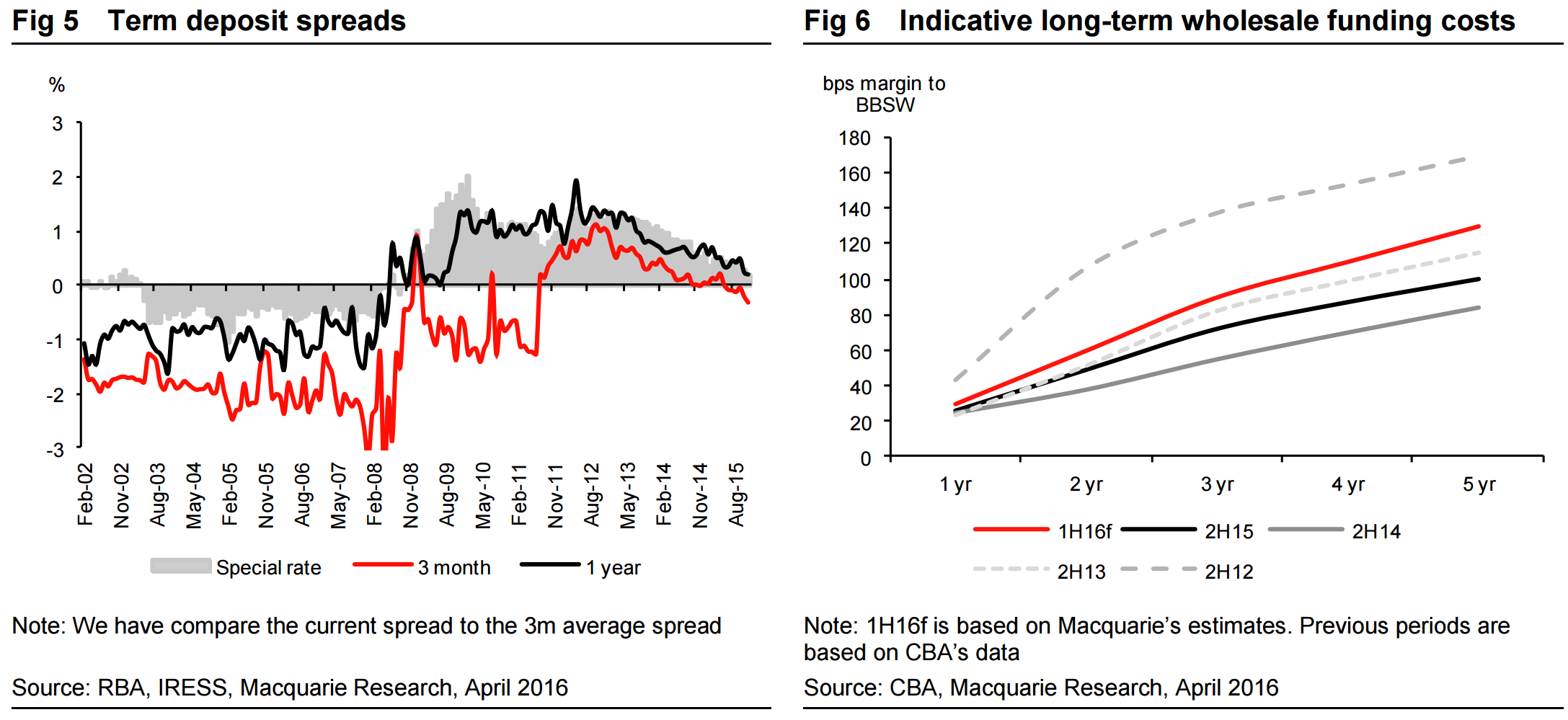

Outlook for deposits. We continue to expect competition for deposits to intensify. While we accept that irrational competition is not going to materially increase the supply of deposits and raise the cost for the industry, we believe pockets of deposit completion will again resurface. As banks need to close their funding gaps, they are likely to be constrained by both the cost and availability of additional term funding. These conditions are likely to lead to higher deposit costs as we experienced from 2008-2010.

Outlook on wholesale funding. We expect Australian banks to lengthen the duration of their wholesale funding. This is likely to put pressure on their margins. We note that as banks increase the quality of their funding, their LCR requirements are likely to fall, providing a small offset.

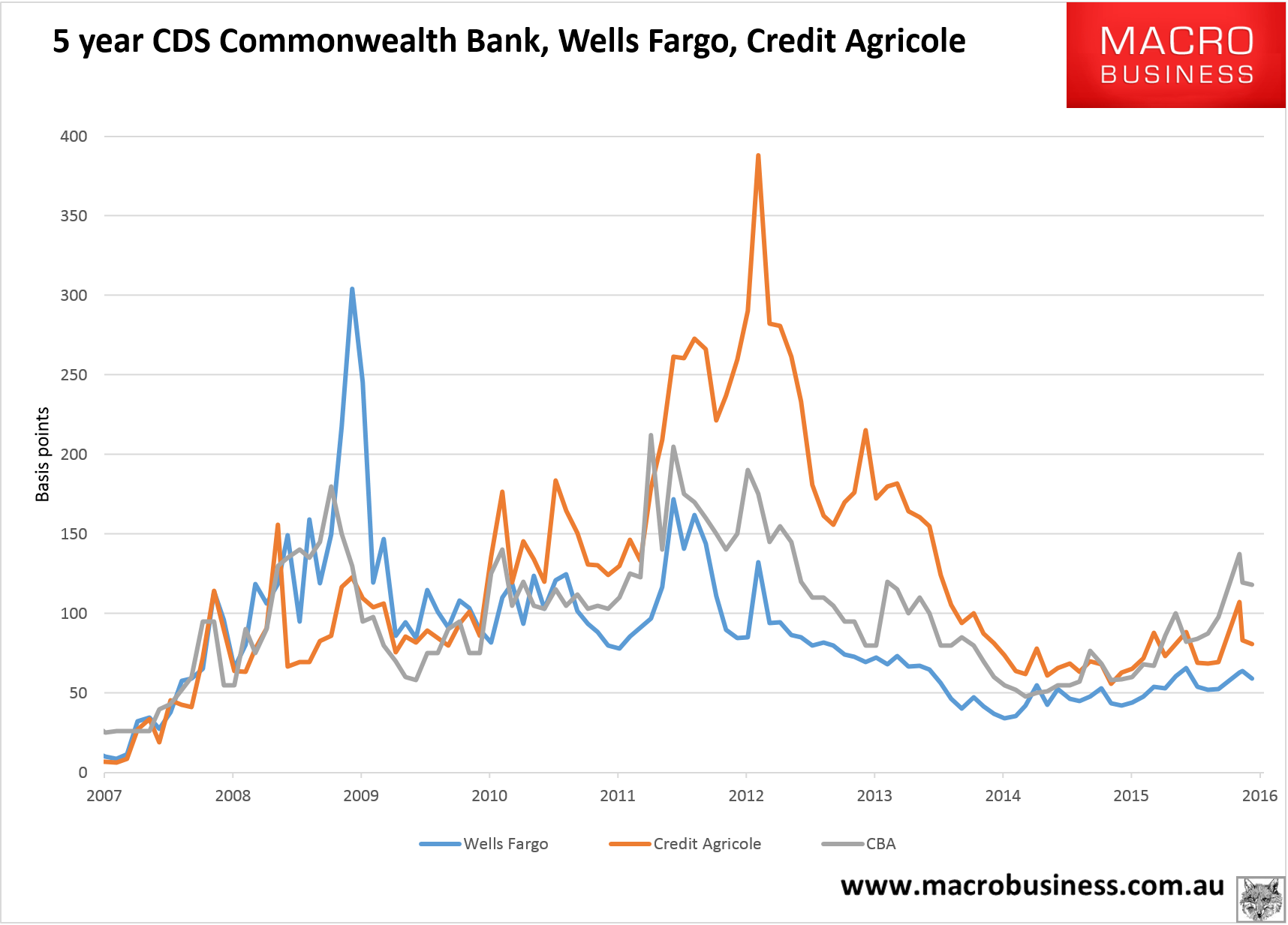

The pressures are internal and external. Yesterday’s CBA CDS price was 118bps:

Advertisement

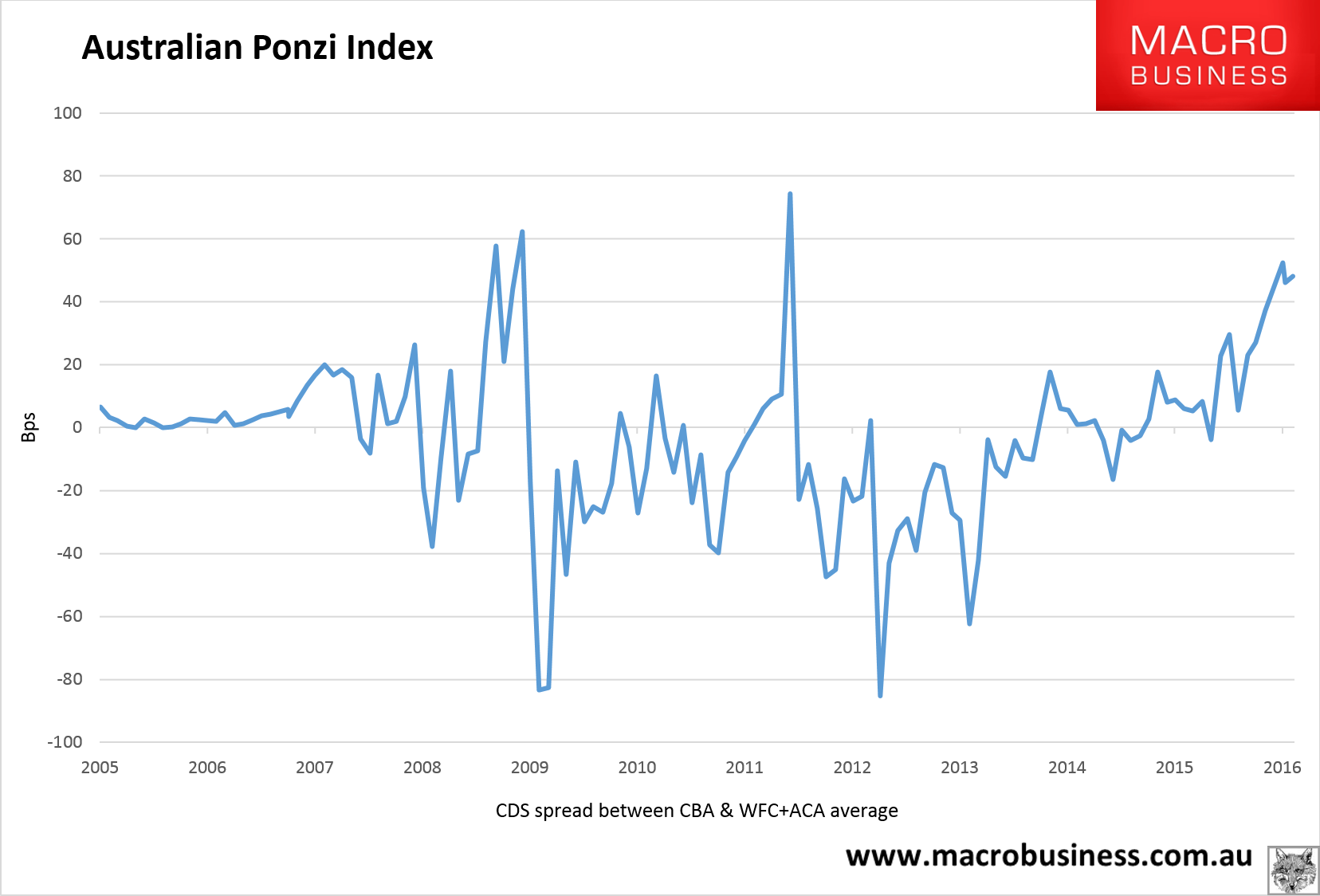

European and US spreads contracted so the Australian Ponzi Index widened:

ANZ has issued new five year paper and the spreads are getting worse as expected, from Banking Day:

Advertisement

The highlight in the domestic credit market last week was the A$2.57 billion, five-year note issue by ANZ (rated AA-). The issue is the largest seen this year and only the second with a five year term to maturity from a major bank.

With the introduction of the net stable funding ratio looming there will no doubt have to be more issuance of this tenor. But as everyone knows, it will be expensive and this issue provides ample confirmation of this.

The only other five-year issue undertaken by a major bank this year was from the Commonwealth in early January, when it was able to raise funds at 115 basis points overbank bill swap rate.

On Thursday ANZ paid 118 bps over, showing that credit spreads are still widening.

But we are yet to get back to the February 2012 peak of 185 bps for five-year funds.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.