Advertisement

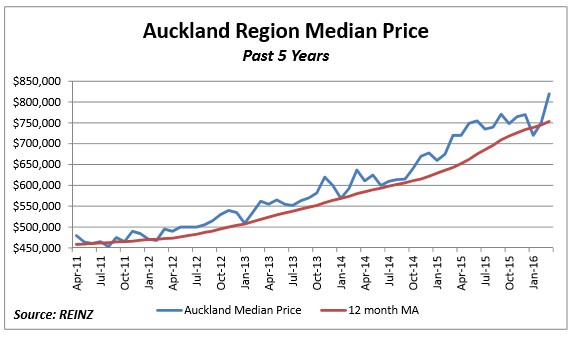

After declining sharply in the last few months of 2015 and in January 2016, Auckland’s housing bubble has re-ignited, with the Real Estate Institute of New Zealand’s (REINZ) latest housing report revealing that Auckland’s median house price hit a record high $820,000 in March:

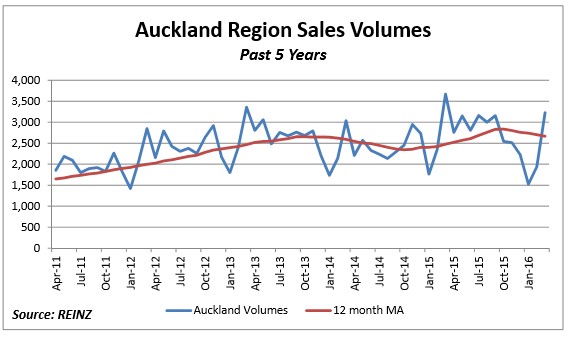

Auckland’s sales volumes, too, rebounded, jumping by a seasonally adjusted 12.9% in March, although they were down 14.1% year-on-year:

Advertisement

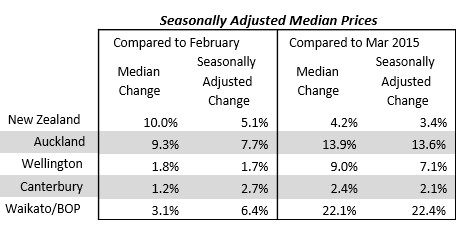

Looking at the broader New Zealand market, the national median price rose by 10% (+$45,000) in March to $495,000, and was also up 4.2% (+$20,000) year-on-year:

Advertisement

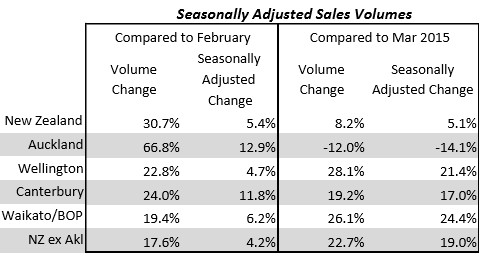

Sales volumes nationally also jumped by a seasonally adjusted 5.4% in March to be up 5.1% year-on-year:

Advertisement

About the author

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.