After the Office of the Chief Economist’s disgraceful iron ore outlook released last week, David Uren takes up the debate over iron ore and the Budget today:

Last year’s budget described the fall in the iron market as “the largest single contributor to writedowns to government tax receipts”. The iron ore price was above $US120 a tonne at the time of the first Coalition budget in 2014.

Treasury provided an estimate that every $US10 move in the iron ore price translated into a $6.5 billion change to budget revenues over a two-year period.

That calculation suggests that the jump in the iron ore price since the mid-year budget update was prepared could add $14.3bn to budget revenue over the next two years if Treasury assumes the increase over the past three months will last.

…Treasury does not have an established method of treating the iron ore price. For the oil price and the Australian dollar, it simply makes a technical assumption that the level holding when it rules off the books in the days before the budget will prevail for the next two years.

If it takes that approach for iron ore, it would lead to a significant lift in revenue flowing from company taxes levied on the big mining companies. However, having been repeatedly caught out by the iron ore price falling by more than was expected, it may be more cautious and take an average analyst forecast.

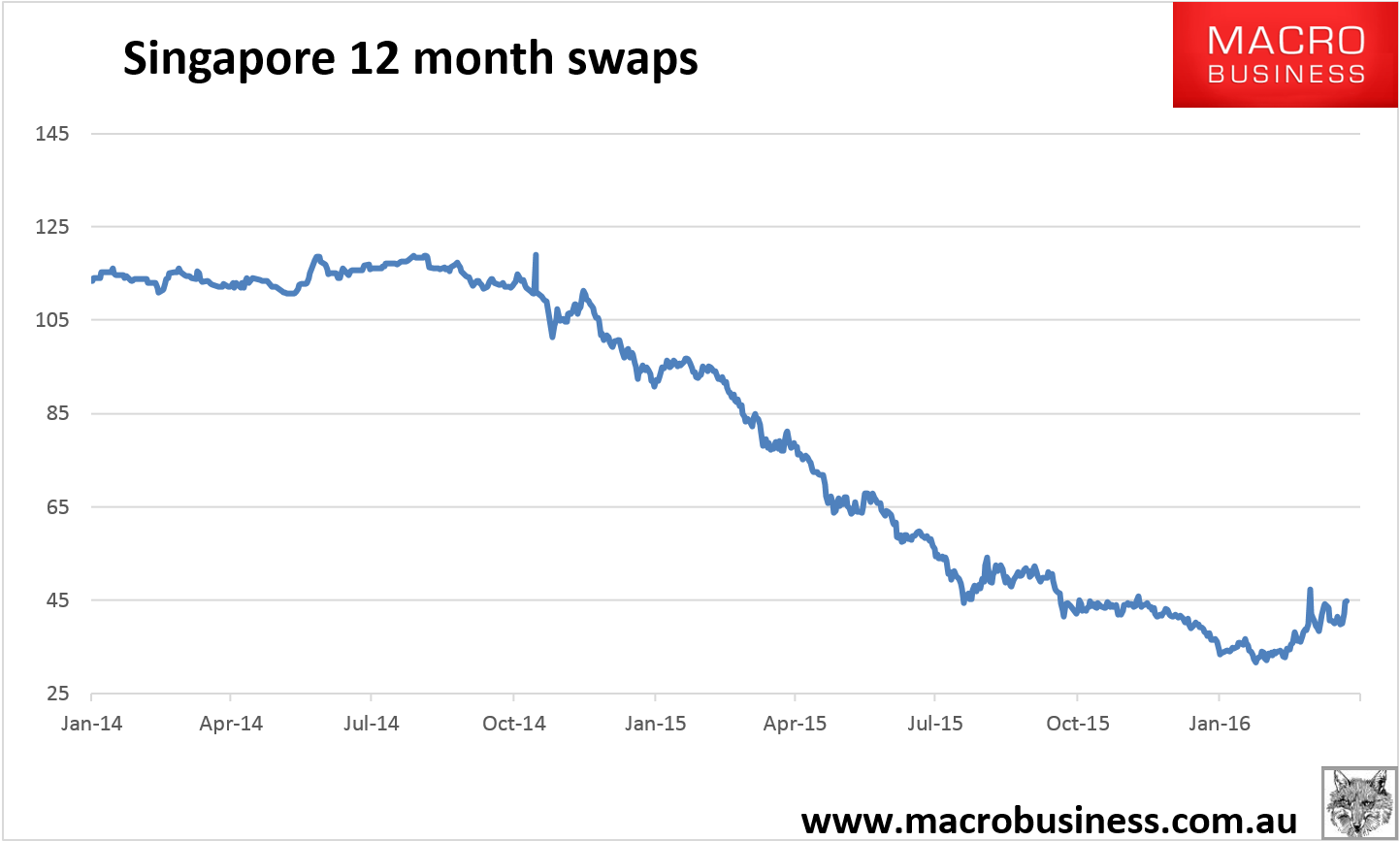

How about using the only sensible approach which is to use the futures market? The Singapore 12 month swap is priced today at $44.84:

It is a deep and liquid market, is not as volatile as the Chinese indexes, has a good record of forecasting prices within a reasonable range of accuracy and intrinsically brings together all available information in one price discovery. No, it’s not perfect but it’s as close you’ll get and, given we’re talking about the outlook for 2016/17 here, it is the perfect choice.

However, the $45 mark would not lift the Budget price of $39 once you add freight cost to bring it up to spot parity.

This is a very obvious choice so if the Budget does go ahead with iron ore price rises in the forecasts, it will be fair to conclude that there is tacit or explicit political interference at work in the outlook.

I mean, take the Office of the Chief Economist (formerly BREE) which managed the following perverse reasoning last week:

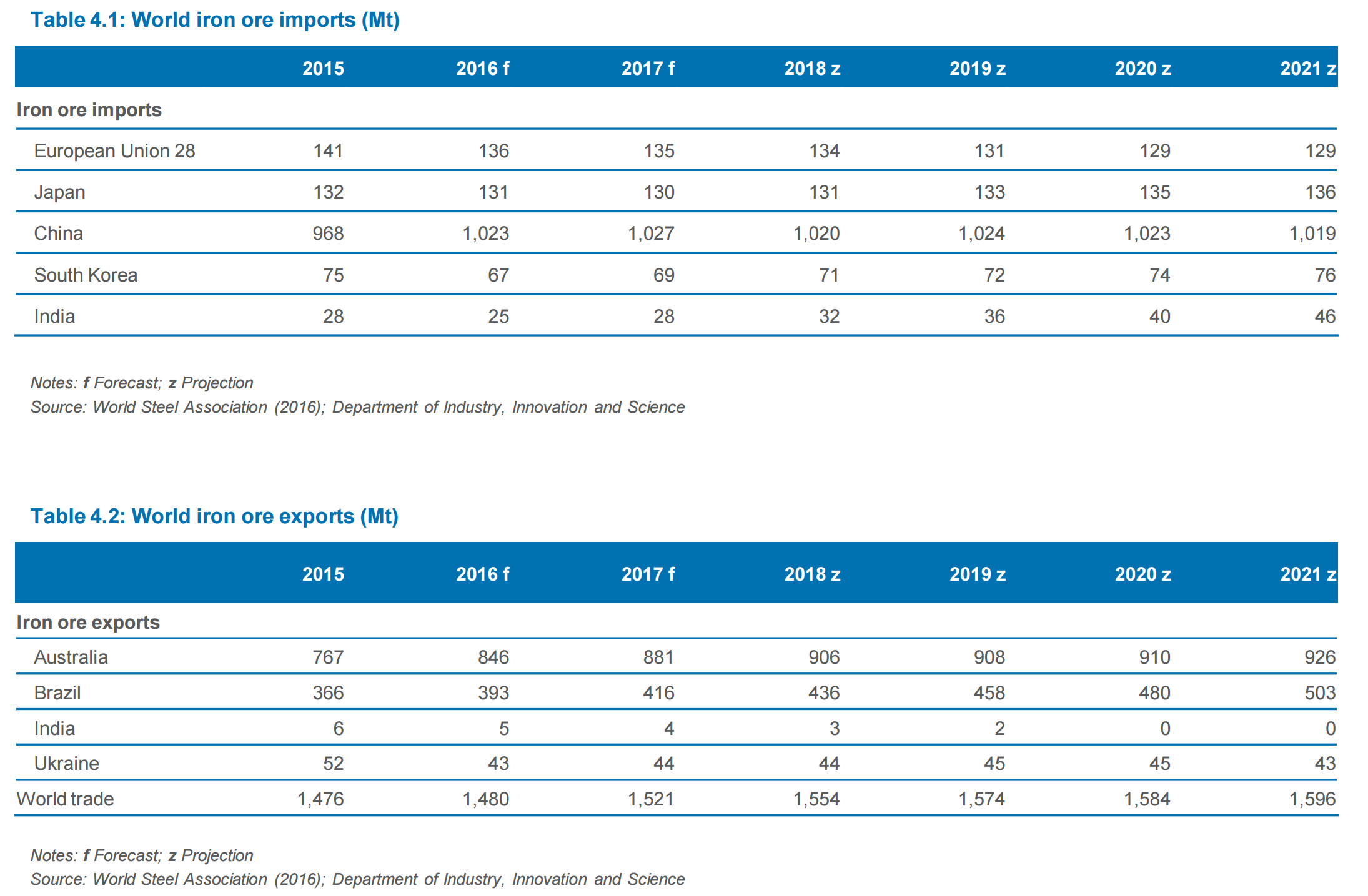

According to Son of BREE, Chinese iron ore imports are barely going to grow but Australia and Brazil exports are going to add between them another 296mt out to 2021 yet the price is going to rise to $70 over the same period. India is going to become a net importer even though it’s about to go completely the other way and stay there.

For this to work, Australia will need to displace all of China’s iron ore production and most of Brazil’s iron ore shipments to China as well while the price rises.

It’s such extravagant nonsense that one can only wonder if it is fraudulent.