From Westpac:

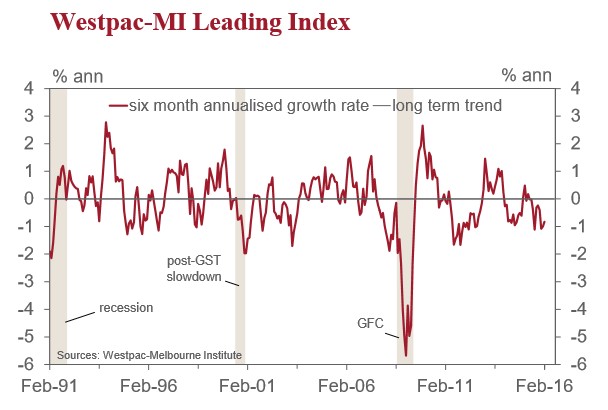

The six month annualised deviation from trend growth rate in the Westpac-Melbourne Institute Leading Index, which indicates the likely pace of economic activity three to nine months into the future, rose from –0.99% in January to –0.82% in February.

Despite some improvement over the last two months, the Leading Index continues to point to below trend growth through much of 2016, implying a slowdown from 2015’s slightly above trend pace.

The December quarter national accounts released earlier this month showed GDP growth of 3% for 2015 as a whole, with growth running at a 3½% annual pace over the second half of the year – ‘trend’ is considered to be around 2¾%yr. That solid finish was foreshadowed by the Leading Index which had run 0.10% above trend on average over the first half of the 2015.

The Index has since weakened significantly, with the six monthly annualised growth rate averaging 0.67% below trend since mid2015. That is a clear signal that growth is set to return to the more sluggish 2-2½% GDP growth rates seen in 2014.

Between September and February the six month annualised growth rate of the Index has slowed from 0.32% below trend to 0.82% below trend. The main components driving the slowdown have been: more negative reads from the yield spread (–0.37ppts); the AUD value of commodity prices (–0.23ppts); dwelling approvals (–0.16ppts); and US industrial production (–0.14ppts). The contribution from the Westpac MI Unemployment Expectations Index has also become less supportive, effectively taking –0.17ppts off the growth pace. These impacts were offset by a reduced drag from the ASX (+0.30ppts) and improved positive contributions from both hours worked (+0.19ppts) and the Westpac–MI Consumer Sentiment Expectations Index (+0.07ppts).

As the component breakdown suggests, the Leading Index is reflecting a shifting mix of both positive and negative developments.

The Index declined 0.15pts in the February month, from 97.22 to 97.07. Amongst the components, the Westpac-Melbourne Institute Consumer Sentiment expectations index rose 1.7%, the commodity price index rose 0.64% and aggregate monthly hours worked rose 0.13%. These positives were more than offset by heavy falls in the S&P/ASX 200 (–2.5%) and dwelling approvals (–7.5%), a narrowing in the yield spread (–0.23ppts) and a slight deterioration in the Westpac-Melbourne Institute Unemployment Expectations Index (+1.34%, indicating a poorer outlook for the labour market).

The Reserve Bank Board next meets on April 5. We continue to expect the Bank to leave rates on hold throughout 2016. Although the Bank is clearly watching developments abroad closely for potential threats, the solid growth figures for 2015 and continued resilience of the labour market are major positives domestically. Recent strength in the Australian dollar has been associated with a more positive outlook for commodity prices and as such would not be grounds for a policy adjustment