A small bounce in the February Labour Force, that is it is less than estimated population growth

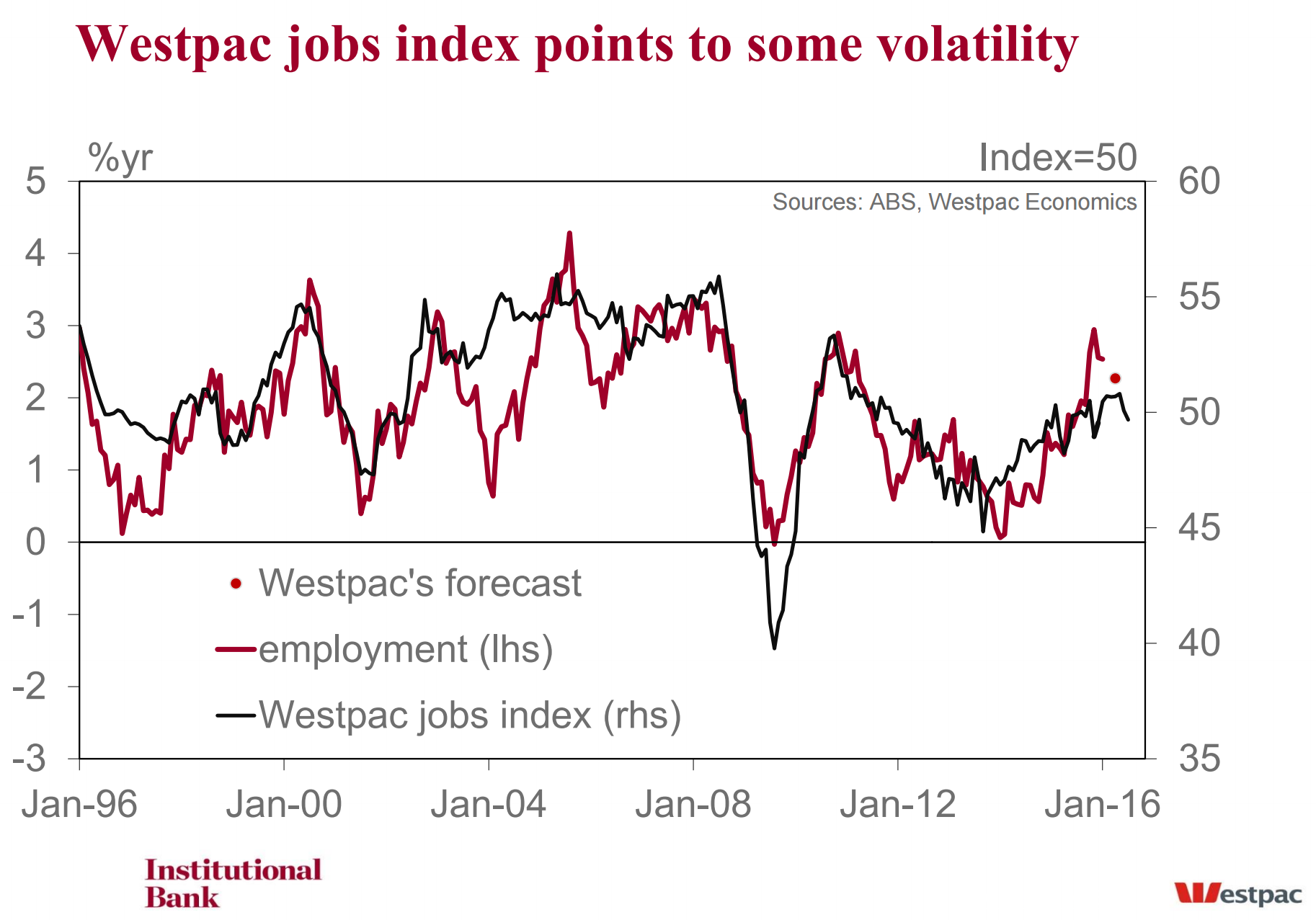

While we do think that the run up in employment in the second half of 2015 may have been overstated, the various other labour market indicators do suggest that Australia has a robust labour market outside WA. So any doubts we have about the survey are more about magnitude rather than direction.

In Jan, total employment fell 7.9k compared to a market median of +13k and a range of –30k to +40k. Westpac’s forecast was for +15k. The Jan survey was the second soft monthly update on employment. Recent statistical issues had made us question the magnitude of the recent strength; as such this soft patch was expected.

Following a strong burst in employment growth through Oct and Nov, employment levelled out through Dec and Jan. This burst took the annual pace well above what other labour market indicators were suggesting and in the past, employment growth has tended to ease back to the indicators.

Our 10k forecast will see the annual pace eased to 2.3%yr from 2.5%yr. The market median forecast is +12k while the range, given the volatility in this survey, is a respectable 3k to 25k. Why not go for a negative to speed the correction? Given the underlying growth in population and how it drives the level of employment in the survey it is hard to get negative prints in this environment.

In Jan the expected lift in participation did come through but it was very marginal (from 65.17% to 65.18%). Nevertheless, it was still enough to help lift the unemployment rate 0.2ppts to 6.0% (6.02% from 5.79% at two decimal places). Westpac had been looking for the unemployment rate to rise to 5.9% based on a slightly stronger employment number.

For Feb we are looking for another small gain in participation from 65.17% to 65.20% which, based on current population growth estimate, should lift the labour force by 26k in the month. With total employment forecast to grow by 10k, this will see the unemployment rate lift to 6.1%.

But we are cautious about just how much further the participation rate can rise. True this rise has been recently driven by rising female participation, particularly from the older groups either returning or staying in the workforce longer, but we not that the historical peak of 65.8% in not too far away from the current print.

We also note that since the Jan survey the ABS revised the population benchmarks from July 2014 to January 2015. However, the revisions to seasonally adjusted and trend estimates throughout the time series due to concurrent seasonal adjustment were minor. The revisions have been noted in the table on slide 2. (For more detail please refer to our review of the benchmarking here)

All our preferred indicators – the Westpac Jobs Index, Westpac-Melbourne Institute Unemployment Expectations, Job Vacancies and even, with questions about how it handles the structural changes in the employment process, the ANZ Job Ads – all suggest that employment should be growing around 1¾% to 2.0%yr not the current 2.5%yr.

So we are forecasting a soft path in employment through the 1st quarter of 2016 that could extend into the 2nd. So why not forecast another small negative in Feb? Remember, the survey collects information on the employment status of individuals from which the ABS estimate shares or ratios of the resident population of each employment condition. These shares or ratios are then applied to monthly estimates of resident population growth.

Why does this matter? Because if there is an underlying trend growth in the resident population then employment will grow by it estimate share of the growth in resident population with no other changes in the survey. So to generate a fall in employment you have to get a fall in the employment ratio that more than offsets the trend rise in population. We think it is unlikely this will happen three months in a row given the underlying fundamentals.

But, as always, there are no certainties with monthly labour force prints!

The last line is the most important. Labour Force is always a craps shoot but with the advent of Numberwang it’s become a pure random walk.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.