Another day, another battery of negative gearing lies from Prime Minister Malcolm Turnbull, this time from a speech to a business lunch in Adelaide yesterday. From The AFR:

Mr Turnbull went after Labor plans to halve the 50 per cent capital gains tax discount and to limit all new negative gearing after July 1, 2017, to new homes only, claiming they would “inevitably undermine property values, increase rents, discourage investment and obstruct entrepreneurship”.

“It’s not a housing affordability strategy, it’s an anti-investment strategy,” he said…

“So when Labor increases the tax on capital gains by fifty per cent it is acting clearly and with eyes wide open to discourage investment.”

Here we go again.

Are we seriously expected to believe that channeling negative gearing into newly constructed dwellings would magically “increase rents”?

Sure, there would be less “investment” (read transfer of ownership) in existing dwellings, but those homes would not magically disappear from the supply-demand equation. Rather, those homes would be purchased by an owner-occupier, thus reducing demand for rental properties by the same proportion as the fall in rental supply.

Moreover, because Labor’s policy would channel negative gearing towards new builds, dwelling construction would increase, as will the supply of rental accommodation. And this extra supply would obviously lower rents. It’s not rocket science.

If Turnbull truly believes this rubbish, then why does the Government champion foreign investment in newly constructed homes, but preclude it from established dwellings?

Here’s the chair of the foreign investment inquiry, Liberal MP Kelly O’Dwyer, explaining the benefits of this ‘new homes only’ policy:

Currently the framework seeks to channel foreign investment in residential real estate into new dwellings in order to increase the housing stock for Australians to build, buy or rent. Foreign investment is encouraged in new dwellings whether they be apartments, units or homes because in addition to creating more supply, it also creates more jobs for the building and construction sector – all of which helps to grow our economy.

Yet again, Turnbull’s opposition to Labor’s plan is full of contradictions and flies in the face of the Government’s stance on foreign investment.

Turnbull’s claim that Labor’s policy would choke investment is equally ridiculous.

Labor Shadow Treasurer, Chris Bowen, has already explained that its negative gearing policy would only apply to “passive” investments – like property and shares – not genuine “active” business investments.

Need I also remind readers once again that in his 2005 tax policy paper, Malcolm Turnbull described negative gearing and the CGT discount as a “sheltering tax haven” that is “skewing national investment away from wealth-creating pursuits, towards housing”, and has caused a “property bubble”.

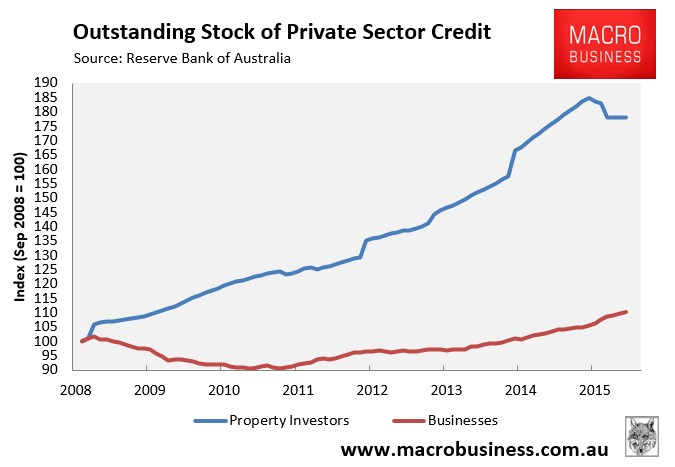

Therefore, it is highly contradictory for Turnbott to argue now that Labor’s reforms to negative gearing would suddenly crush productive business investment, when this is already happening under the current rules. If you want proof, check-out the below chart:

Since the GFC, outstanding business loans have increased by only 10% in nominal terms whereas outstanding property investment loans have ballooned by nearly 80%. If there is one segment that is losing from the current tax structure it is productive business lending, particularly lending to small enterprises, which is being crowded-out by housing lending.

Turnbull is also curiously silent on why the current rules allow individuals to claim unlimited negative gearing deductions for property investments into perpetuity, but if they invest in a productive side business, they must meet all kinds of criteria in order to claim losses against their wage/salary earnings, including showing a profit in three out of five years.

Further, why has the Government capped the ability of individuals to deduct education expenses from their income, and why is it now looking at capping work-related deductions as well, but is happy to leave negative gearing into property untouched? How is the tax code in any way consistent between how it treats genuine business/work-related deductions and investment property?

The answer is that the tax code is not consistent, which is why Turnbull in his 2005 tax paper also stated that “Australia’s rules on negative gearing are very generous compared to many other countries” and that “the normal deductibility principles do not apply to negatively geared real estate such that the taxpayer is not obliged to demonstrate that the negatively geared property will generate positive cash flow at some point in the distant future”.

Quit the scaremongering, Mr Turnbull.