The Australian Industry Group Australian Performance of Services Index (Australian PSI® ) lifted by 3.4 points to 51.8 in February, indicating expansion across the services sector (results above 50 points indicate expansion, with higher numbers indicating a stronger rate of expansion).

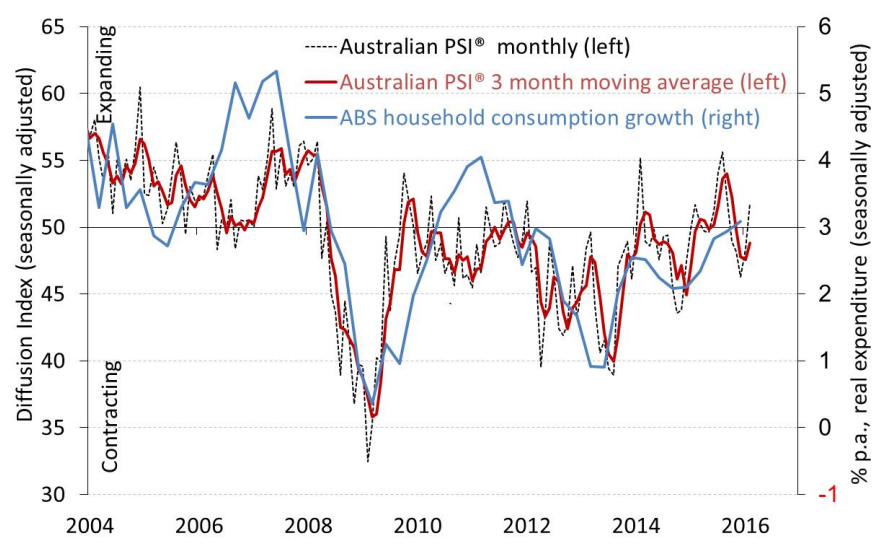

• The February result for the Australian PSI® revives the expansion evident in the middle of 2015. This suggests household consumption growth could strengthen further in Q1 2016.

• Of the five of activity sub-indexes in the Australian PSI® , all except supplier deliveries (47.7 points) were above 50 points in February. Sales and new orders went from stable or contraction to expansion (55.7 points and 53.6 points respectively in February). Stocks and deliveries both stabilised (both 50.1 points).

• Only three of the nine services sub-sectors in the Australian PSI® grew in February (in three month moving averages). These were finance & insurance services plus the large consumeroriented health & community services sector (which includes health, welfare and education) and personal & recreational services. Health & community services showed the strongest rate of growth in the Australian PSI® in February 2016, at 56.1 points. • The other six sub-sectors in the Australian PSI® all contracted in February. Business services and the goods distribution sectors (retail, wholesale and transport) continue to face difficult conditions. The worst performer was transport & storage services at 39.4 points, indicating a relatively strong rate of contraction in February.

• The wages sub-index in the Australian PSI® rebounded to 54.1 points, after contracting in January. Selling prices were stable (49.9 points). Input price rises remain relatively strong (60.5 points), possibly due to the continuing impact of the low dollar on imported inputs.

ACTIVITY SUB-INDEXES

• Sales picked up from stable conditions in January to expansion in February (55.7 points), after a disappointing period of contraction at the end to 2015.

• New orders recovered from a four month contraction, posting growth (53.6 points) in February. This promising reversal suggests that sales could pick up further, later in 2016.

• The supplier deliveries sub-index was stable in February (50.1 points), after expanding marginally in January (51.0 points). Deliveries have been relatively stable over the last twelve months, with this sub-index recording an average of 49.6 points.

• Stock levels (inventories) stabilised in February (50.1 points) after another contraction in January. After reducing for much of 2015, the stocks sub index looks to be stabilising.

• The Australian PSI® employment sub-index remained in negative territory at 47.7 points in February. This marks the sixth consecutive month of contraction for services employment, after expanding through much of 2015.

• Capacity utilisation across the services sector expanded to 76.1 per cent of available capacity being utilised in February, recovering most of the seasonal reduction in January.

PRICES SUB-INDEXES

• Input price rises remained relatively strong, at 60.5 points in February. This upward pricing pressure for inputs largely reflects the continuing impact of the low Australian dollar on imported input prices for retailers, wholesalers and others.

• The wages sub-index in the Australian PSI® recovered to 54.1 points in February, after contracting in January (the lowest result and only contraction since June 2009). Recent ABS Wage Price Index (WPI) data show private sector wages increased by only 2.0% p.a. in Q4 2015, but key service sectors showed stronger growth, with wages in finance +2.7% p.a., health +2.3% p.a., retail +2.5%, recreation +2.3% p.a., hospitality +2.3% p.a. and personal & other services +2.3% p.a.

• Selling prices were roughly stable in February (49.9 points), after falling in November and December. Reflecting the low inflation environment in 2015, selling prices in the Australian PSI® have been relatively stable over the past twelve months (50.3 points on average).

The big miss is in employment which is still falling. Otherwise an encouraging report.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.