The front-runner to win this year’s Nobel Prize in economics, Yale professor Peter Phillips, has co-written a paper with Auckland University Economics Lecturer Ryan Greenaway-McGrevy, in which they identify Auckland housing as once again being in “bubble” territory. From Bernard Hickey at Interest.co.nz:

The paper applied econometric techniques used to identify asset bubbles in the United States and elsewhere to New Zealand house price data…

“Using recently developed statistical methods for testing and dating exuberant behaviour in asset prices we document evidence of episodic bubbles in the New Zealand property market over the past two decades,” they said in the paper.

“The results show clear evidence of a broad-based New Zealand housing bubble that began in 2003 and collapsed over mid-2007 to early 2008 with the onset of the worldwide recession and the financial crisis”…

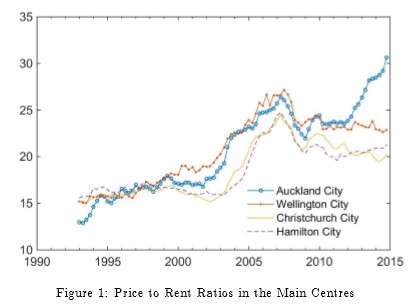

“Our findings suggest that the Auckland metropolitan area is currently experiencing a property bubble in terms of the house price-to-rent ratio that began in 2013″…

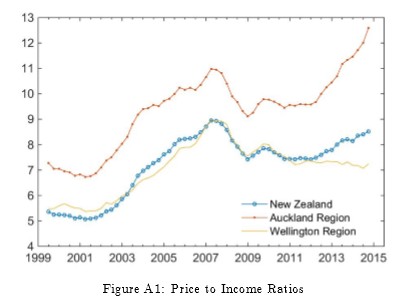

The paper also claims that Auckland housing is a “bubble” relative to incomes:

Advertisement

The authors believe that any correction will likely occur via a reduction in nominal prices driven by either a “demand or supply shock, or combination of the two”:

“The price-to-rent ratio can fall by house prices falling, by an increase in rents, or by some combination of these two channels. Household incomes ultimately place an upper bound on the amount of income that can be spent on housing costs (assuming that household incomes are exogenous to housing prices and rents)”…

“We show that rental expenditures as a proportion of income have remained remarkably constant over the past decade in the main centres of Auckland, Wellington and Canterbury. For example, in the Auckland region rents have remained consistently around 25% of expenditure since 2003″…

“Thus, if a market correction were to come through an increase in rents, this would involve an unprecedented increase in rental expenditure shares. In our view, therefore, any correction is more likely to come through an adjustment in prices driven by a demand or supply side shock, or combination of the two.”

The paper also points to the many deleterious impacts arising from the bubble, including “intergenerational wealth effects, reducing the relative wealth and welfare of younger generations, renters and first-time home buyers in relation to extant property owners”, exacerbating inequality, adverse “financial and macro-economic stability risks”, and inhibiting labour mobility and economic growth.

Advertisement

Can messrs Peter Phillips and Ryan Greenaway-McGrevy please conduct a similar analysis on Sydney and Melbourne, which are likely just as bubbly as Auckland?

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.