From Macquarie comes some good news for savers (except the RBA will snuff it out):

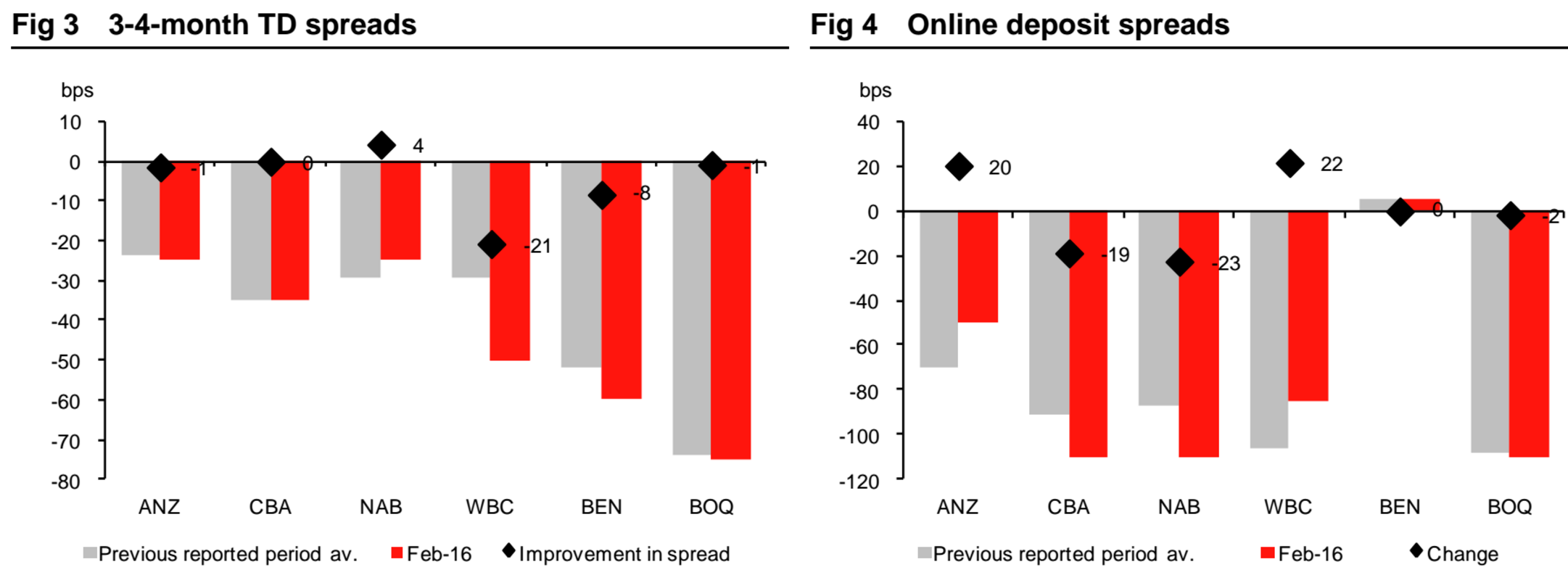

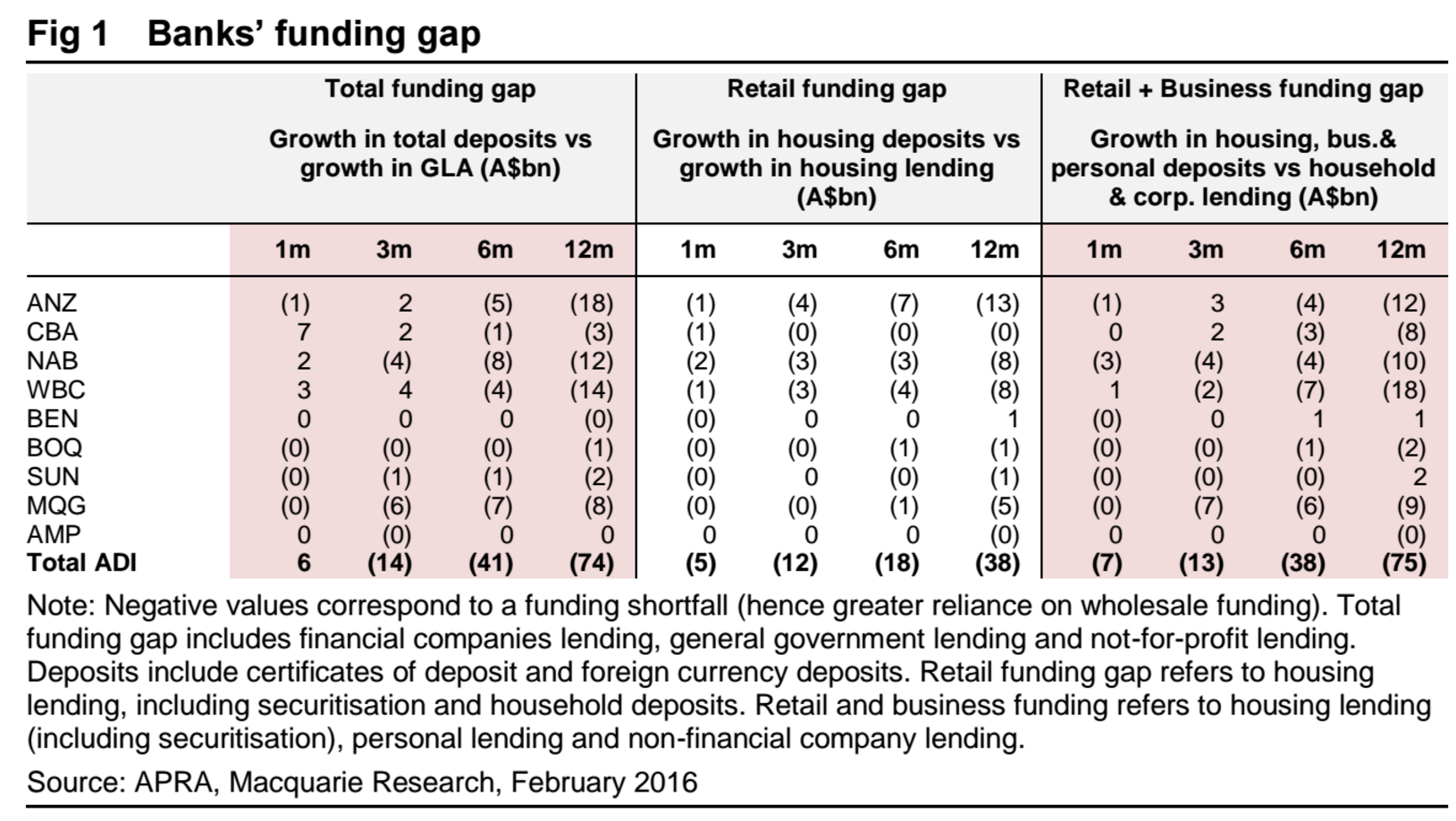

Given tightening in the wholesale funding markets we expected to see a step-up in deposit competition. While banks appear to be competing more aggressively for deposits, it appears that competition has remained contained. Our analysis on special deposit spreads suggests that ANZ’s deposit spreads continued to improve (potentially explained by ANZ’s funding position benefit following the Esanda sale), while peers have either increased their deposit rates in either the on-line space or on TDs. We estimate that over the past three months, all ADI’s funding gap stood at ~$13b. WBC and NAB appear to have a bigger funding gap than peers. In our view, given a deteriorating funding environment, the focus on deposit gathering is likely to intensify, which may put further pressure on deposit costs in the later part of FY16.

What’s a $74 billion funding hole between friends?

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.