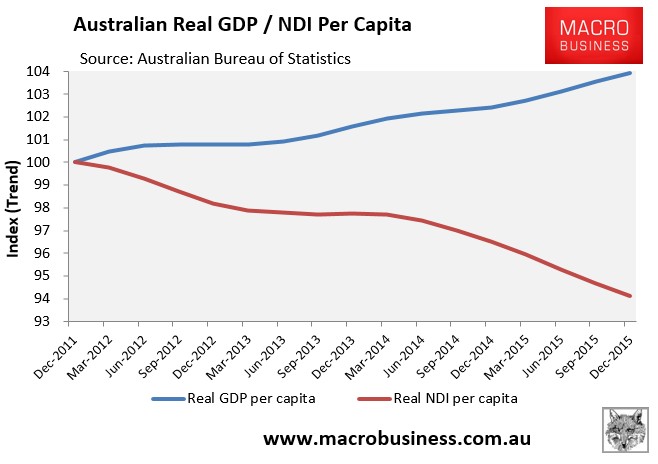

Australian GDP is proving to be spectacularly resilient despite the nation’s standards of living falling at an equally marvelous rate:

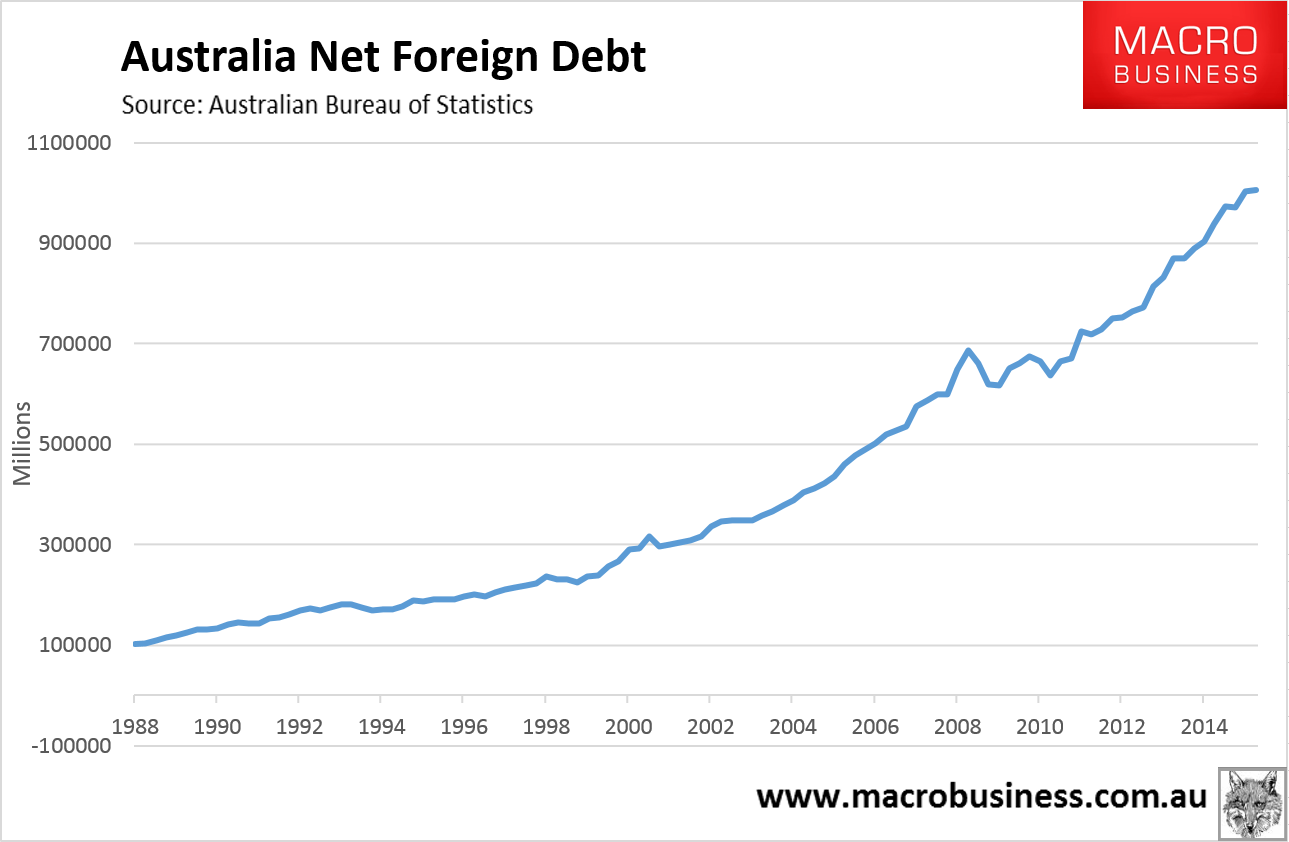

This has consequences and the main one is this: so long as Australia can continue to print solid GDP there is little reason for markets to turn off the credit tap even if we’re borrowing as a nation at the fastest rate of growth ever:

This is the key to everything in Australia. We can grow GDP more or less forever so long as markets don’t mind letting us leverage public and private balance sheets up even as our incomes decline. So, is it time to position for Australian success?

First, let’s ask what that “success” will look like:

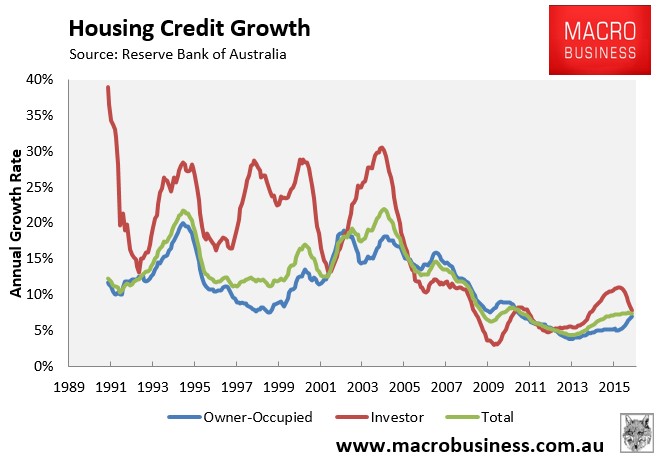

- private sector credit has already slowed and will keep doing so as macroprudential and other housing measures take effect:

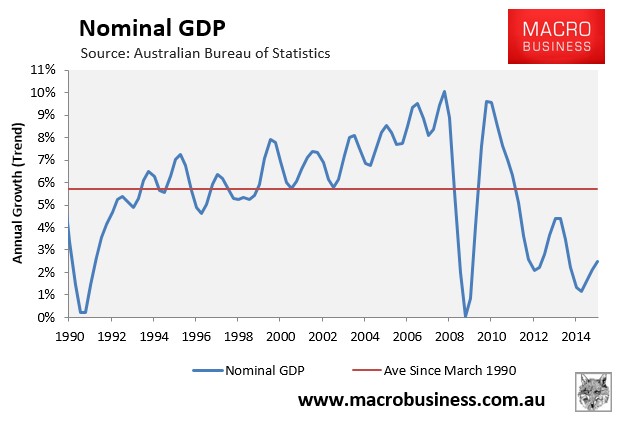

- there is little to cheer about for the Budget given nominal growth is still poor so government will have to keep borrowing heavily:

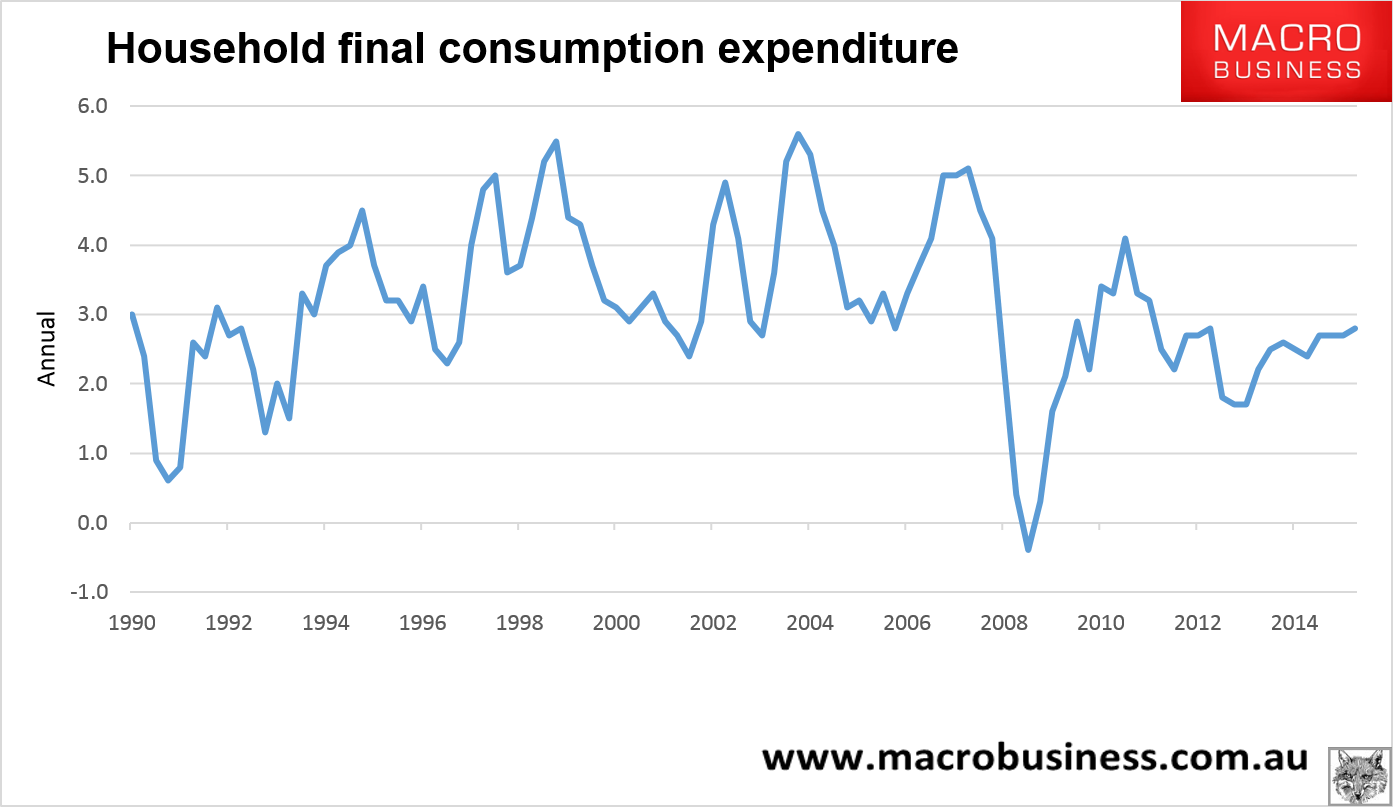

- household consumption will wax and wane with confidence as the headwinds mount and fade but on the whole it remains weak:

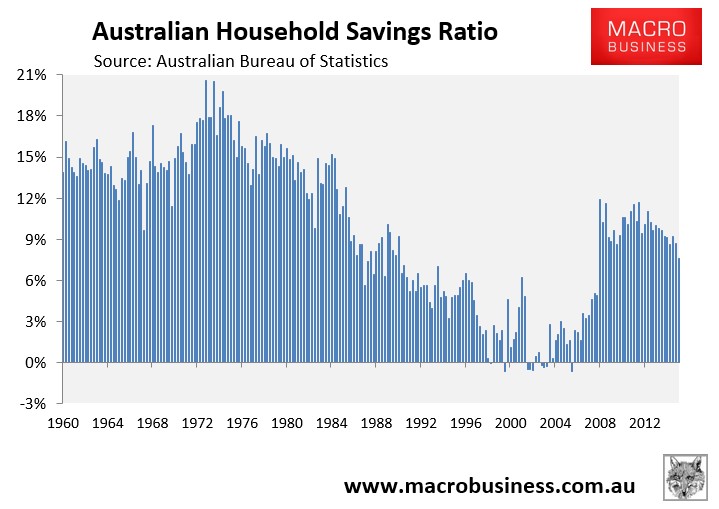

- more rate cuts are still coming to ensure that the property bubble is supported and that households keep spending their savings for the good of GDP:

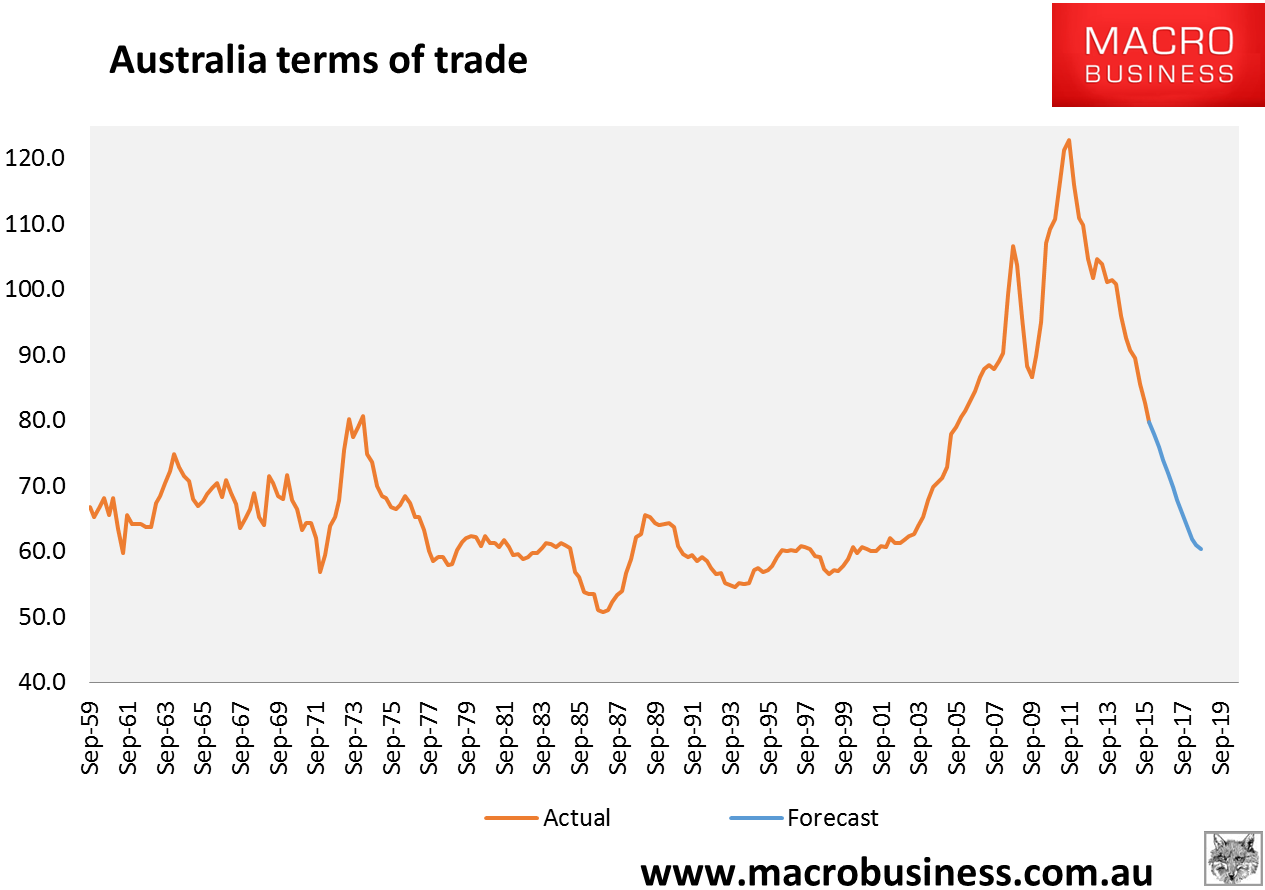

- the terms of trade will keep falling as iron and coal revert to mean:

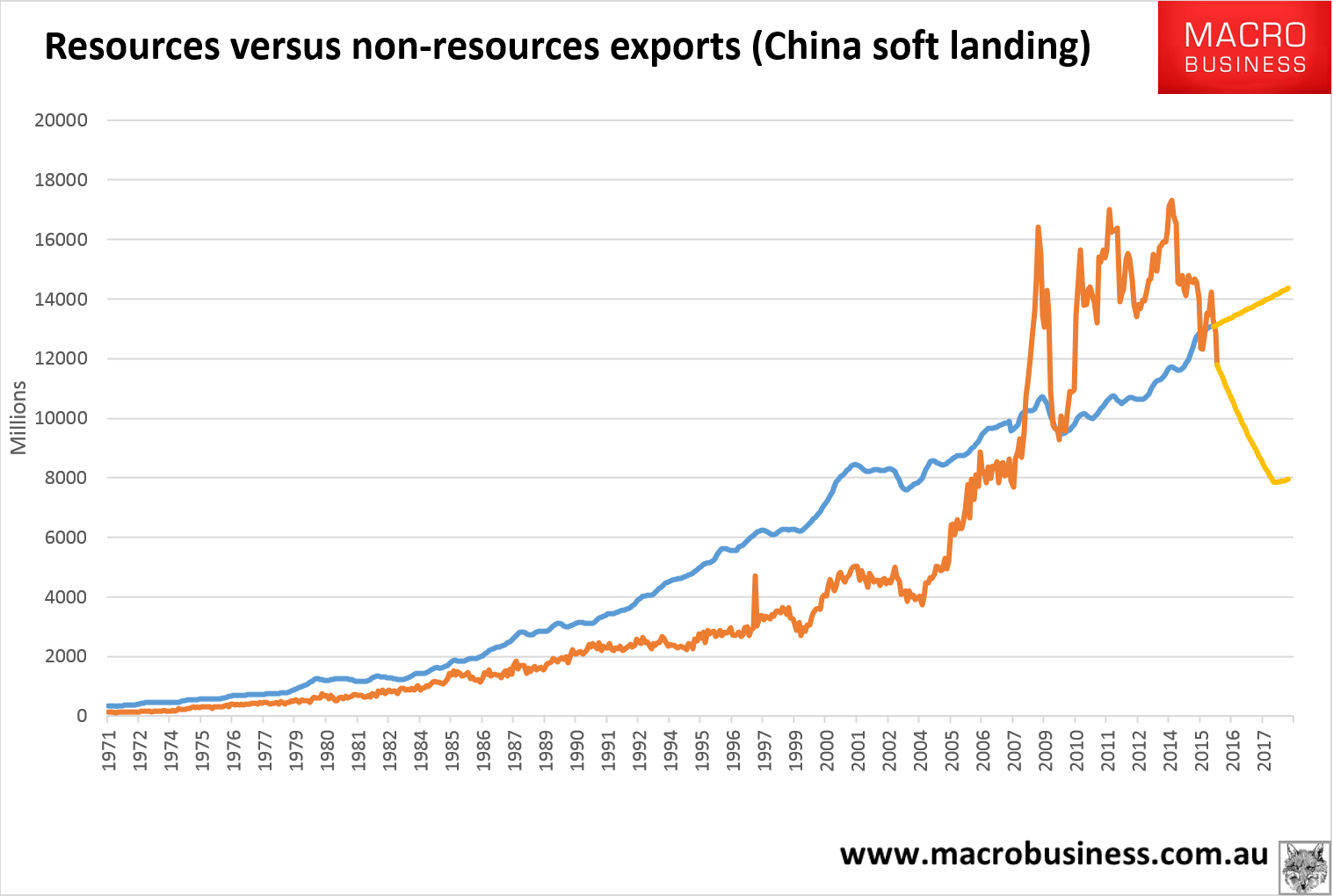

- export income will continue to rebalance from mining to non-mining with a net result of falling income which will have to be made up for by borrowing:

- the dollar will also to keep falling but more slowly than it should as it fights the rest of the world’s low and negative interest rates, guaranteeing another headwind;

- LNG volumes will continue to drive net exports growth, though it will diminish given imports are up on consumption as we saw yesterday;

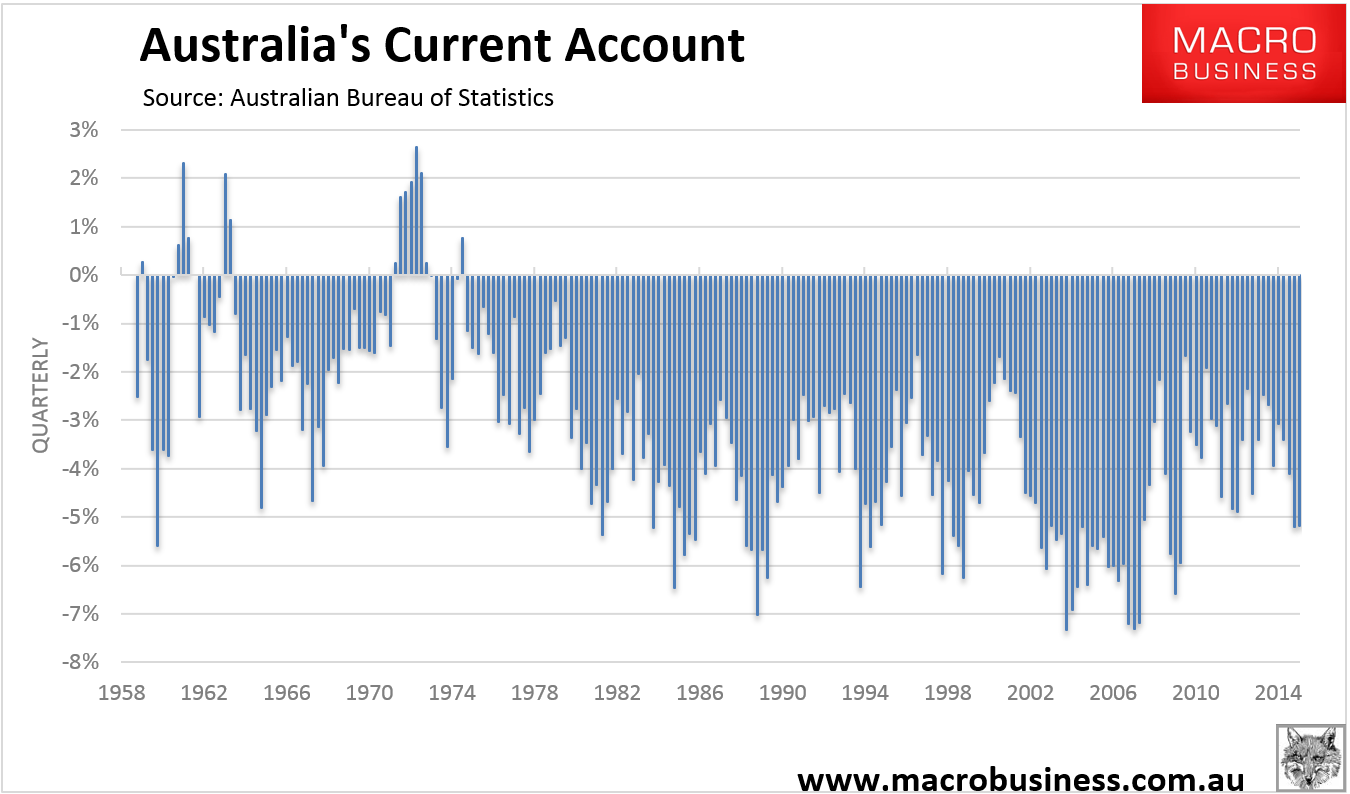

- the current account deficit that has been on a tear should stabilise at risky but manageable levels as growth pulls back towards 2%. If bubble growth persists at 3% then we’ll risk a very risky blow out:

So, even the Australian success scenario is not a great picture for another three years but it is manageable so long as there is no external shock that makes markets question the viability of the model. If you want to back that success then going long banks (which are under-priced for a successful post-mining boom rebalancing) and dollar-exposed industrials are the plays. The two together hedge nicely as well. Judging by yesterday’s stock market action there’s quite few out there buying this thesis. It is still much too early to buy miners and domestic demand will remain lumpy and lousy causing earnings dyspepsia for locally-exposed stocks.

My own view is that little has changed following the GDP data, except to register just how hard it is for Australia to have an ‘official recession’ with the current mix of growth drivers. We’ve just passed through a convergence of serendipitous events – huge house price rises, tumbling petrol prices, ABS Numberwang and the ascendancy of Malcolm Turnbull – generating a moderate impact upon confidence and spending. But those drivers are already fading as:

- house price growth stalls and falls;

- combined capex cliffs in residential construction, cars and mining hit the labour market along with ABS Numberwang give back;

- the Turnbull bubble pops on a caustic negative gearing election, and

- global volatility persists around the Mining GFC.

Most importantly, I do not see the global economy getting through the forthcoming period of Australia’s major post-mining boom headwinds without another cycle-ending shock. The commodities bust is not over. China is still slowing and changing fast, pressuring the yuan. The US is still tightening while others all ease, pushing up the US dollar. Emerging market business models are still broken. Australian bank funding costs are already at nosebleed levels well before we’ve gotten to any crisis from the above so that bodes poorly for local credit costs as the economic headwinds persist, let alone when the end-of-cycle shock actually arrives, and when the sovereign rating is downgraded.

If you share that view then you ought to be in cash, calmly waiting.