The Grattan Institute has released a new report entitled HELP for the future: Fairer Repayment of Student Debt, in which author Andrew Norton calls for the repayment threshold on HELP student loans to be lowered in a bid to reduce costs to taxpayers and forestall the need to slash university funding.

Below is the overview along with some key charts from the report.

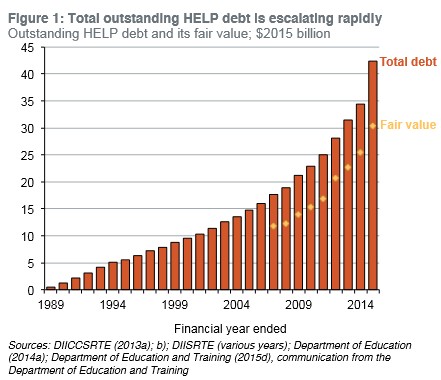

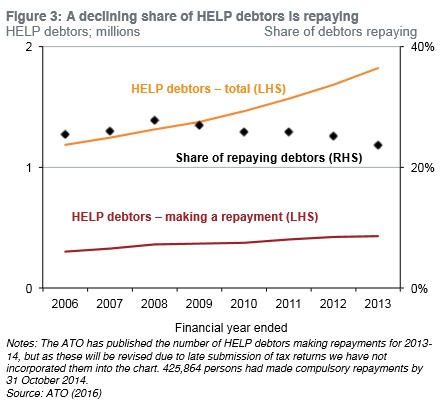

Since 1989 nearly four million Australians have taken out HELP student loans, greatly expanding access to tertiary education. But too many HELP borrowers either do not repay what they owe, or take too long to clear their debts. Without change, HELP’s costs will escalate, putting other education programs at risk of cuts.

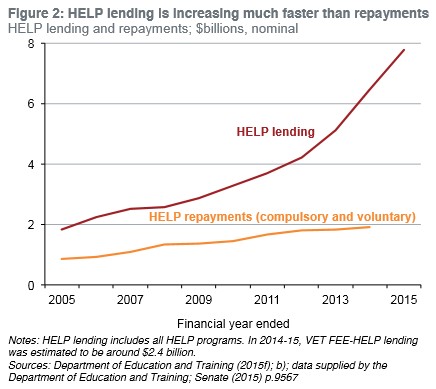

In 2014-15, the government lent students $7.8 billion. An estimated 20 per cent, or $1.6 billion, won’t be repaid. Interest subsidies on outstanding HELP debt add $200 million to HELP’s costs, but would be five times higher if interest rates return to previous levels.

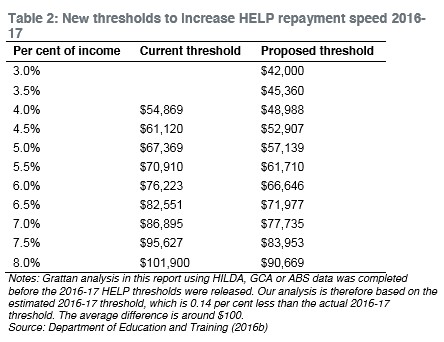

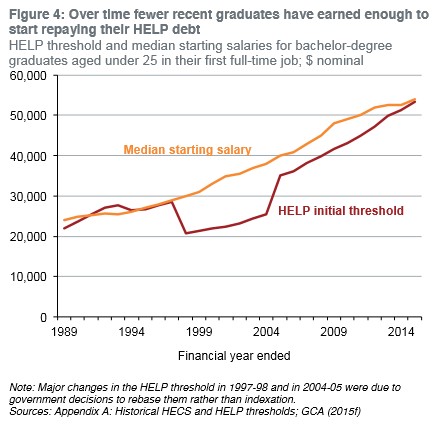

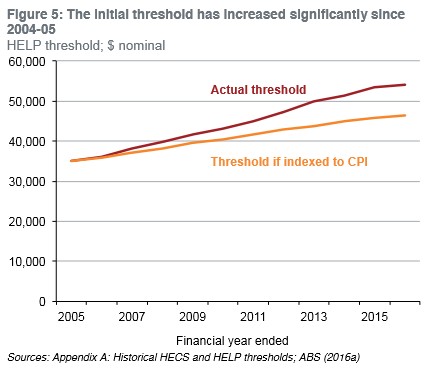

A major cause of HELP’s problems is that debtors who earn less than its initial threshold – currently $54,126 – do not repay. A lower $42,000 threshold in 2016-17 would be a more realistic way to address major trends in the earnings of those with HELP debts.

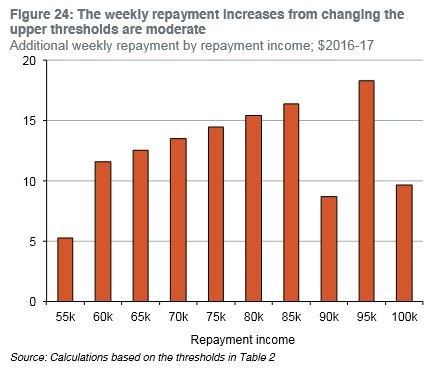

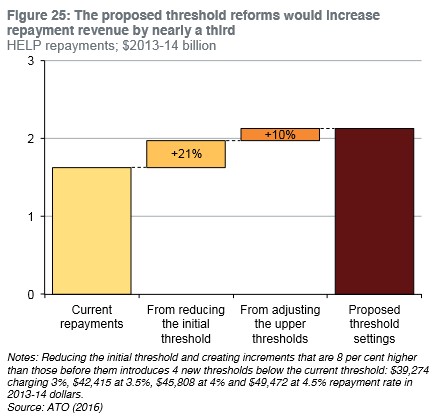

Lower thresholds would increase total HELP repayments by at least $500 million a year, reducing interest costs and doubtful debt. Fewer well-off people would receive HELP subsidies, which would be more targeted toward people facing genuine financial hardship. The savings would reduce pressure to cut teaching and research grants.

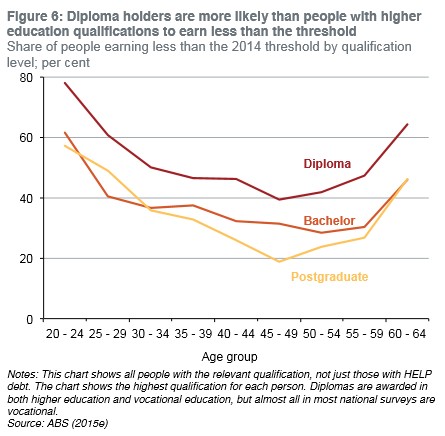

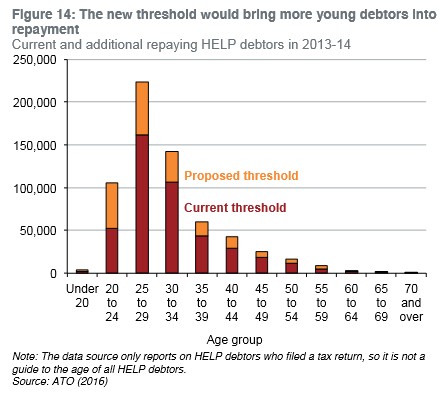

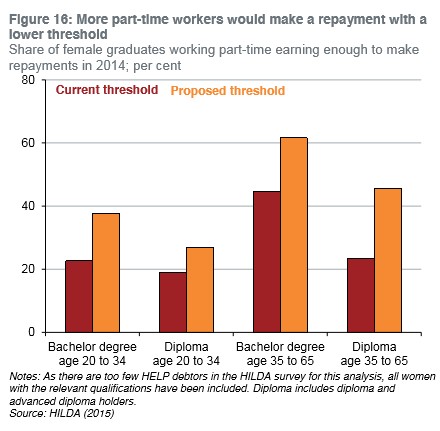

A growing proportion of all graduates work part-time, but most part-time jobs earn less than the current threshold. Vocational education diploma students now get HELP, and are less likely than higher education graduates to earn $54,126 or more. With the new threshold, almost 50 per cent more debtors would repay.

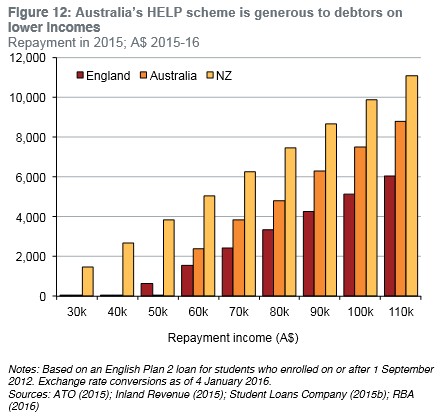

International experience suggests that even with a lower threshold, students are still attracted to tertiary education. The English student loan repayment threshold is set at a level similar to A$42,000, while in New Zealand the threshold is much lower.

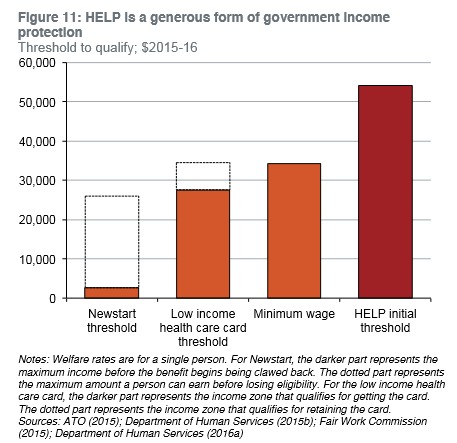

Although a $42,000 threshold would affect debtors who are not well-off, overall it is a fair level that still protects against financial hardship. The initial threshold for repaying HELP is $20,000 more than the Newstart and low income health care card thresholds. Graduates do not have special needs compared to non-graduates who receive government financial assistance.

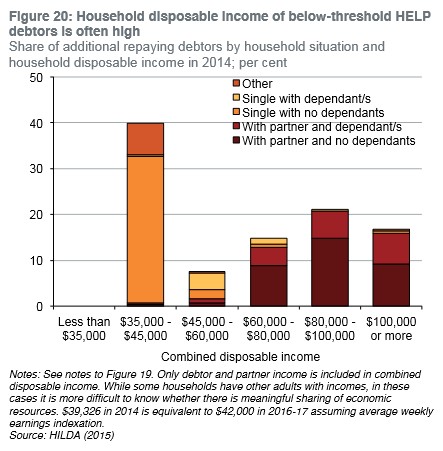

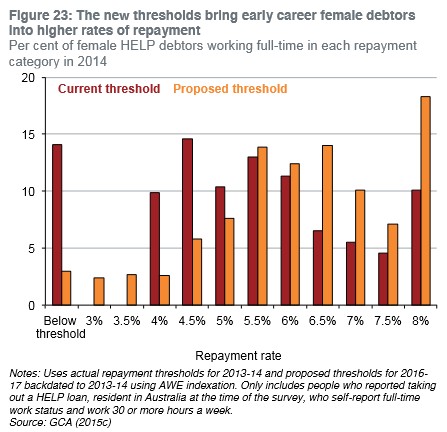

Threshold reform affects more women than men, due to high rates of part-time work, but most debtors who would be affected are not the only income earner in their household. Half live with a partner, and the combined disposable income of 70 per cent of these couples exceeds $80,000 a year.

At $54,126, HELP debtors repay 4 per cent of their income each year. At $42,000, a rate of 3 per cent of their income should apply. As they do now, repayment rates should increase with income, up to a maximum of 8 per cent. Each threshold would be lower than current one, so that more debt is repaid each year.

Lower thresholds are both efficient and fair. Unlike other possible cuts to education spending, expenditure on HELP can be reduced without damaging its vital education and social policy goals.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.